Source: Pixabay

Canada GDP rises

EURUSD climbs as data shows Eurozone recovery gaining momentum

Surging crude prices undermine USDCAD

RBA leaves monetary policy unchanged

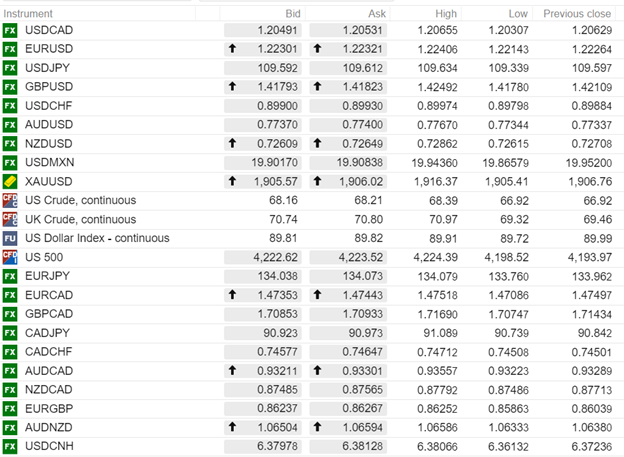

USDCAD open 1.2049-53, Overnight range 1.2028-1.2066, Previous close 1.2063

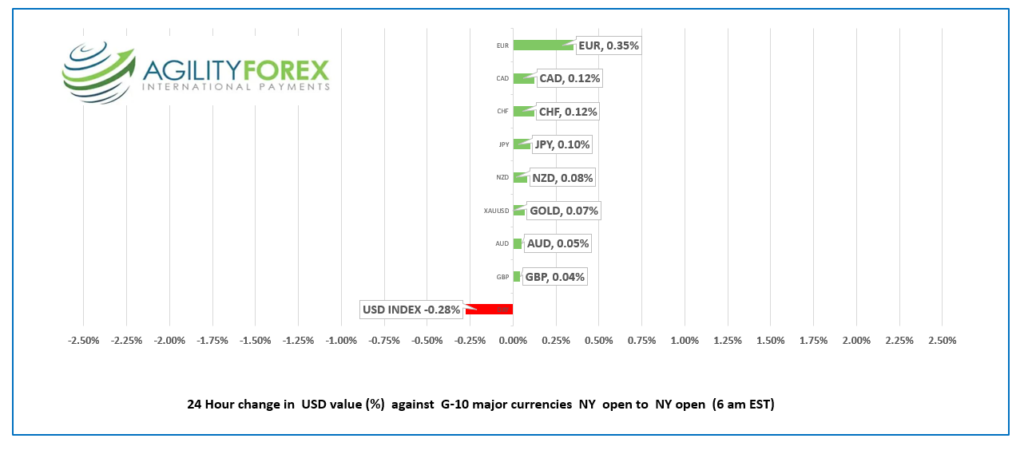

FX at a Glance-24 hours

FX Recap and outlook

Canada GDP grew 1.1% m/m in March, easily beating February’s 0.4% gain, while winning streak extends to 11 consecutive months. The result was a tick better than the 1.0% predicted. However, Q1 GDP fell to 5.6% q/q, which was well-below the consensus of for a 6.7% gain.

All in all, the results are positive for the Canadian dollar, and economists, and the Bank of Canada expect robust growth beginning in the second half of the year.

Overnight, FX markets were steady in Asia, but somewhat choppy in Europe after a series of Eurozone economic reports suggested the Eurozone economic recovery was gaining steam. China equity indexes closed with gains, while Japan’s Nikkei 225 and Australia’s ASX 200 were modestly lower. Better than expected Eurozone data powered European bourses higher, led by a 1.45% rise in the German DAX index.

Oil prices are higher. WTI oil climbed to $68.39/barrel from $66.92/b ahead of today’s Opec meeting. Analysts expect the cartel to maintain the current plan to phase out production cuts through July, while new production from Iran is not likely to disrupt the market.

US 10-year Treasury yields climbed from 1.581% to 1.622% overnight. Yields are well within the current range but are underpinned by concerns ahead of Friday’s nonfarm payrolls report. The consensus forecast for NFP is 650,000, although many forecasters are suggesting a much higher result.

EURUSD traded with a bid tone in a narrow 1.2214-1.2241 range. Prices were supported by news Eurozone inflation reached the ECB target level, rising to 2.0% from 1.6% y/y in May. ING economists suggest CPI will stay at 2.0% for the rest of the year, but the pressures are temporary, and CPI will drop in 2022. Eurozone and German unemployment data were better than expected. The EURUSD uptrend is intact above 1.2130, a level guarded by support at 1.2205.

GBPUSD rallied in Asia, then dropped in Europe, falling from 1.4249 to 1.4157 after the UK Final May Manufacturing PMI was lower than previous (actual 65.6 vs previous 66.1). Even so, the CIPS statement noted, “Conditions in the manufacturing sector improved at an unprecedented rate in May, as output growth strengthened and new orders rose at the quickest pace in the near three-decade survey history. The intraday GBPUSD technicals are bullish above 1.4150.

USDJPY rallied from 109.40 to 109.67, supported by the rise in US 10-year treasury yields. USDJPY gains are facing headwinds due to inflation differences between Japan and the US. There is no inflation in Japan, meaning that Japan offers a higher real yield than the US.

The Reserve Bank of Australia left monetary policy unchanged. The OCR rate is unchanged at 0.10% and reiterated that rates will remain unchanged until 2024. AUDUSD danced between 0.7732 and 0.7767 and is trading at the overnight low. NZDUSD tracked AUDUSD lower.

USDCAD traded around 1.2027 before and after the GDP data was released. USDCAD tracked broad US dollar sentiment against the EUR while domestic economic recovery hopes, and rising crude oil prices weighed limited upside moves.

USDCAD may struggle to break below support in the 1.2000-1.2010 area ahead of Friday’s Canadian and US employment reports.

The US ISM Manufacturing PMI data (forecast 60.7, unchanged from April) is the focus today.

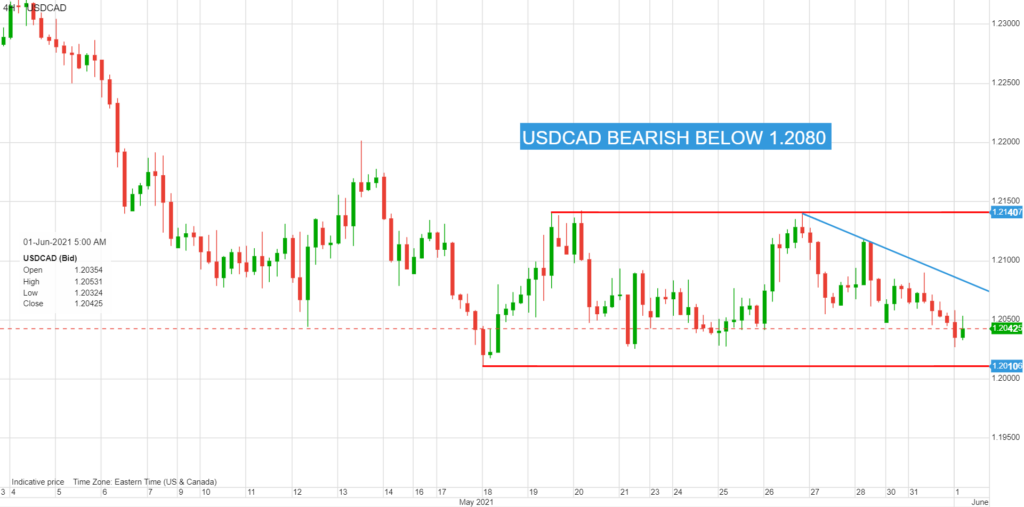

USDCAD technical outlook

The intraday USDCAD technicals are bearish below 1.2080, looking for a break below 1.2000 to extend losses to 1.1935. For today, USDCAD support is at 1.2030 and 1.1990. Resistance is at 1.2080 and 1.2120. Today’s range 1.2000-1.2080

Chart USDCAD 4 hour

Source: Saxo Bank

FX open, high, low, previous close

Source: Saxo Bank