Source: IFXA Ltd

- FOMC minutes from Dec. 15 due this afternoon

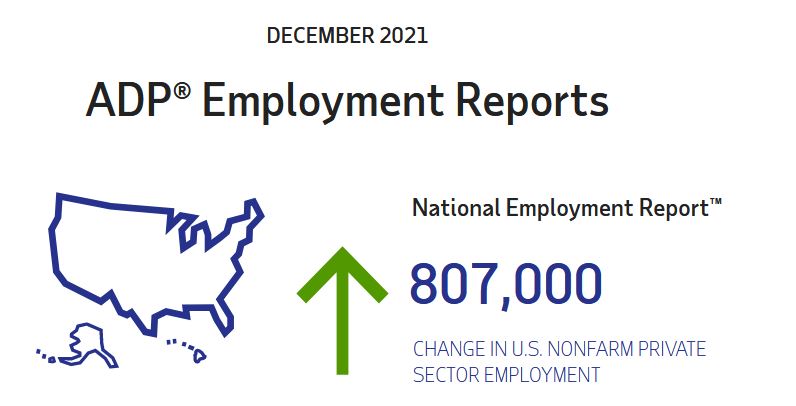

- Upside surprise to ADP employment number

- US dollar opens defensively

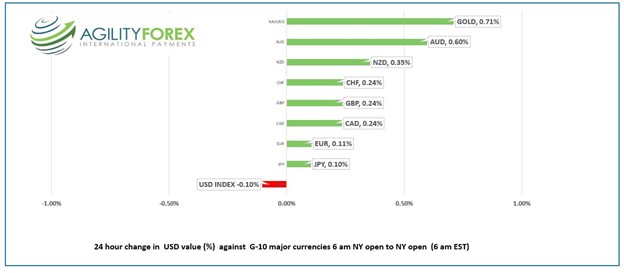

FX at a Glance

Source: IFXA Ltd/RP

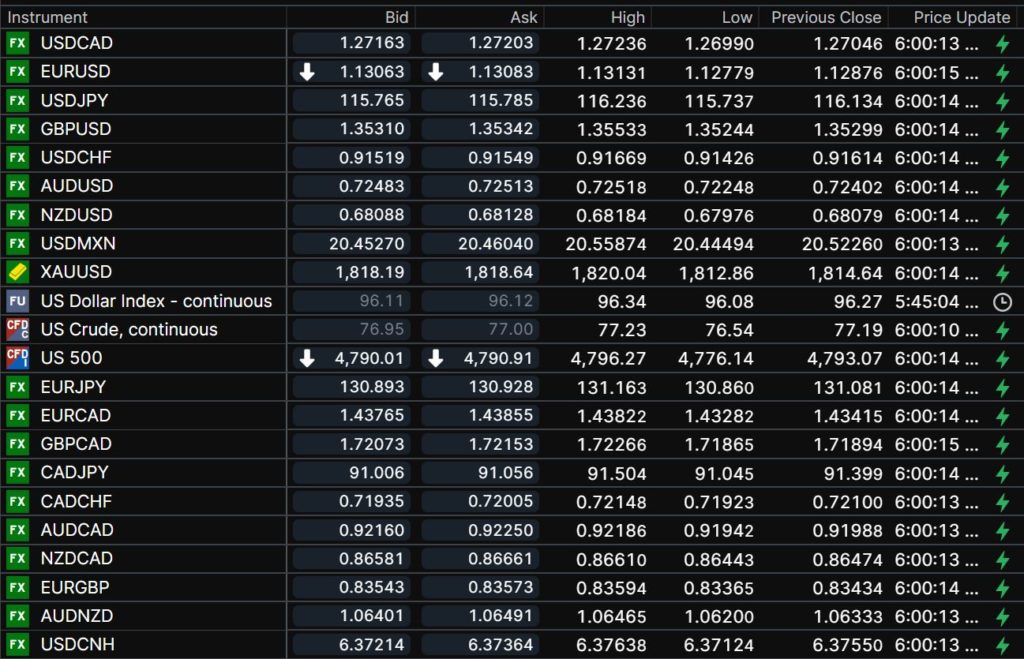

USDCAD Snapshot: Open 1.2716-20, Overnight Range-1.2699-1.2724, previous close 1.2705

USDCAD is trading sideways ahead of the FOMC minutes with some traders hoping to get some clarity as to the timing of a Fed rate hike. They won’t find it in the minutes, and the market has already priced in a 90% chance for a rate hike in June.

Opec and friends agreed to increase production in February by the previously announced 400,000 barrels per day and lowered its forecast for the size of a projected surplus in Q1 2022. That news, plus the weekly API crude report that showed US inventories declined by 6.43 million barrels, underpinned prices. WTI consolidated recent gains in a $76.54/b-$77.23/b range overnight.

USDCAD may also see support thanks to renewed US trade hostilities. The USMCA trade dispute panel found that the Canada is in breach of the trade treaty due to dairy industry protections. It is good news for Canadian consumers but not so much for domestic farmers. The US went after Canadian softwood lumber in November and slapped on new tariffs.

USDCAD may see modest support from the latest Omicron restrictions across the country, particularly in Quebec, and Ontario, which may weigh on Q1 GDP.

Canada New Housing Price Index rose 11.7% y/y in November while Building Permits surged 6.8% m/m compared to 2.4% in October.

Technical view: The intraday USDCAD technicals are bearish below the 1.2750 and looking for a test of support in the 1.2600 area which has contained downside moves since the middle of November. A decisive breach will target 1.2500. A break above 1.2750 opens the door to a retest of the 1.2960 area.

For today, USDCAD support is at 1.2690 and 1.2660. Resistance is at 1.2750 and 1.2790. Today’s Range 1.2660-1.2750

Chart USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

It is a cautious start to the day as releasing the FOMC minutes from the December 15 meeting gives traders an excuse to sit on the sidelines.

Surging numbers of Omicron cases empower doomsayers, but traders have bought the story that the variant is less severe than Delta and is moderately risk positive.

ADP employment rose 807,000 in November (forecast 400,000) which to some, bodes well for an upward surprise to Friday’s nonfarm payrolls report.

Source: ADP

Asia equity indexes closed flat to slightly lower except those in China, which suffered from news of adverse regulatory actions on a few tech companies. European stocks are higher, while US equity futures flitter around flat. WTI oil is a tad lower than yesterday’s closing level, while gold is slightly higher, and US 10-year yields sit at 1.642%.

EURUSD is trading near the top of its overnight 1.1278-1.1323 range. Eurozone Services and Composite PMI reports were a tick lower than expected at 53.1 and 53.3 respectively, but the results had negligible impact on the currency as it was due to the Omicron outbreak. ECB policymaker Francois Villeroy suggested that inflation was peaking.

GBPUSD traded in a narrow 1.3524-1.3553 range. The currency pair is modestly supported because the UK government did not impose any new restrictions due to the Omicron outbreak, while Euro area governments opted for lockdowns. Prices are also supported by the prospect of higher UK interest rates. The GBPUSD uptrend channel from December 20 is intact.

USDJPY drifted lower, falling from 116.24 to 115.63, in tandem with the retreat in the US 10-year yield from 1.683 yesterday to 1.651% today.

AUDUSD and NZDUSD rallied on the back of mildly positive risk sentiment, which led to broad US dollar weakness.

Chart of the Day: GBPUSD 4 hour

Source: Investing.com

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

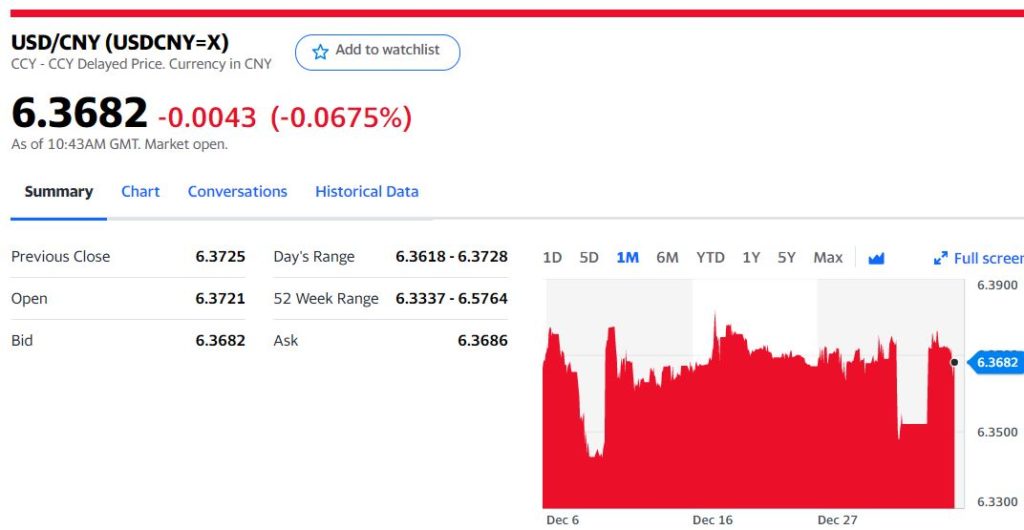

China Snapshot

Today’s Bank of China Fix 6.3779, previous 6.3794

Shanghai Shenzhen CSI 300 fell 1.01% to 4,868.12

China fines some tech companies (Alibaba, Tencent, Bilibili) for failure to report some deals

Chart: USDCNY 1 month

Source: Yahoo Finance