Source: YouTube

- US data and Fedspeak in focus today

- CAD lags commodity currency performance

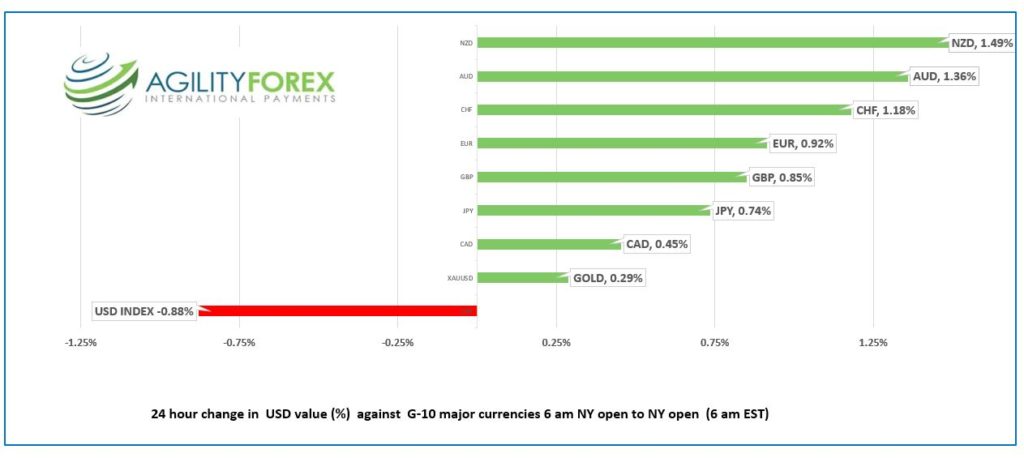

- US dollar extends losses, ignores US rate hike risks

FX at a Glance

Source: IFXA Ltd/RP

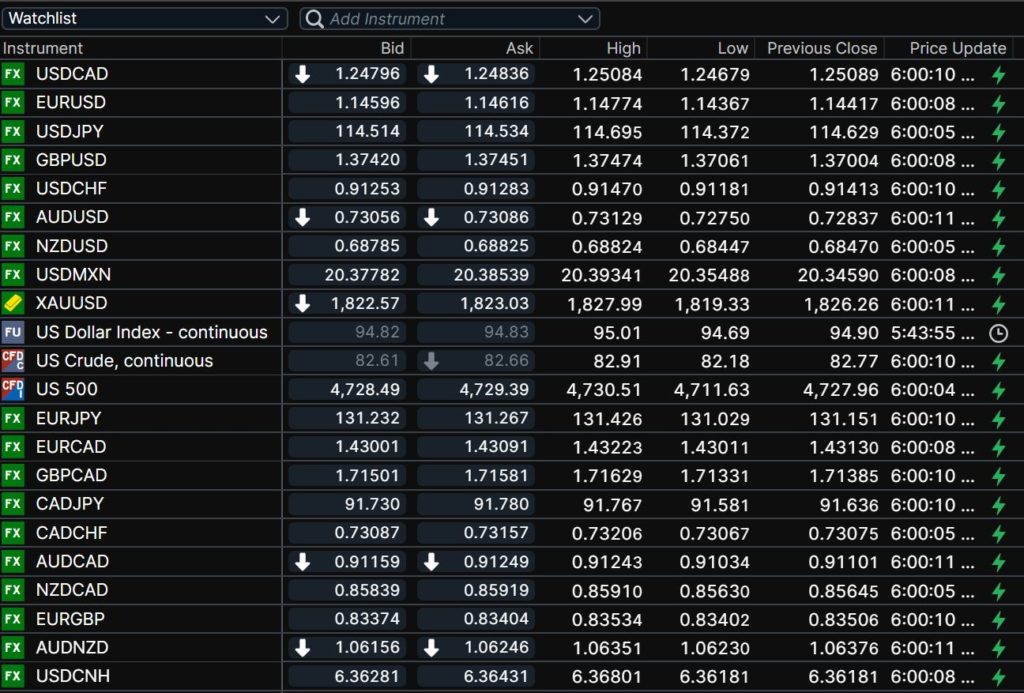

USDCAD Snapshot: Open 1.2480-84, Overnight Range-1.2468-1.2508, previous close 1.2508

USDCAD is sinking under a wave of broad-based US dollar selling and rising oil prices. Prices retested the overnight session low following weaker than expected US weekly jobless claims and PPI data. Traders ignored yesterday’s 7.0% y/y rise in US inflation, steady to firm oil prices, and comments from Fed officials advocating four rate hikes in 2022.

Normally, talk and data supporting higher interest rates would lead to US dollar demand but this time, traders were not surprised. The December FOMC statement was hawkish and when the minutes were released last week, the projected three rate increases in 2022.

Traders bought US dollars in anticipation of Fed tightening, and now that have confirmation, are taking profits and/or squaring positions.

USDCAD is seeing added pressure from the outlook for oil prices. JP Morgan analysts are forecast crude at $125.00/b this year and $150.00/b in 2023, due to Opec’s falling spare capacity.

USDCAD is also undermined by talk the Bank of Canada will raise interest rates at the January 26 meeting followed by four other hikes in 2022.

Technical view: The USDCAD technicals are bearish below 1.2675, the downtrend line from December 20 and following the move through 100 and 200-day moving average support. USDCAD is attempting a decisive move below 1.2484 (50% Fibonacci retracement of Jun-August 2021 range) which if successful targets 1.2373 (61.8% Fibonacci) with 1.2236 lurking as a “stretch” target.

For today, USDCAD support is at 1.2440 and 1.2410. Resistance is at 1.2520 and 1.2550. Today’s Range 1.2440-1.2520

Chart USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar is having a bad week. No one wants it, despite yesterday’s US CPI printing a 40 year high and St Louis Fed President James Bullard predicting the first of four rate hikes, starting in March. Philadelphia Fed President Patrick Harker agrees, saying he would be open to more than three rate increases if inflation worsens. There will be more of the same as Lael Brainard replies to questions at today’s vice chair confirmation hearing.

Today’s US data didn’t help. Weekly jobless claims rose 23,000 rather than drop 7,000 which was predicted. The results were likely skewed as it was the first week of 2022.

Producer Price Index (PPI) rose 0.2% in December below the forecast for a 0.4% increase

It is not all sunshine and unicorns in the world. The Iran nuclear talks have faltered, and the US is baiting China by sending navy carrier groups for cruises in the South China Sea.

Even worse, EU foreign policy head Josep Borrel said they should not negotiate with Russia while Russia troops are on the Ukraine border. The Kremlin said that if the US imposed sanctions on President Putin, it would the same as severing relations.

FX traders are ignoring these developments as well as Omicron outbreaks.

EURUSD accelerated higher after the “as expected” US inflation data yesterday and hasn’t looked back. EURUSD climbed from 1.1323 pre-CPI to 1.1477 in Europe before easing to 1.1463 in NY. ECB policymaker Luis de Guindos may be deviating from the script when he said that inflation might not be as transitory” as recently forecast. The ECB economic bulletin said the global economy was recovering, but rising commodity prices, supply disruptions, and the Omicron variant weigh on the near-term growth prospects. The EURUSD technicals are bullish above 1.1380, looking for a test of 1.1500.

GBPUSD traders appear unconcerned about ongoing Brexit issues and Boris Johnson’s political problems. GBPUSD broke through the top of the uptrend channel from December 20, climbing from 1.3706 to 1.3748. Price have retreated to 1.3723 in NY.

USDJPY slid to 114.37 from 114.69 due to broad US dollar weakness, but prices inched higher when the US 10-year Treasury yield ticked up to 1.75% from 1.722% yesterday.

AUDUSD and NZDUSD rallied due to rising commodity prices and positive risk sentiment. Better than expected New Zealand Building Permits data was not an issue for Kiwi.

Chart of the Day: GBPUSD (4 hour)

Source: Saxo Bank

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

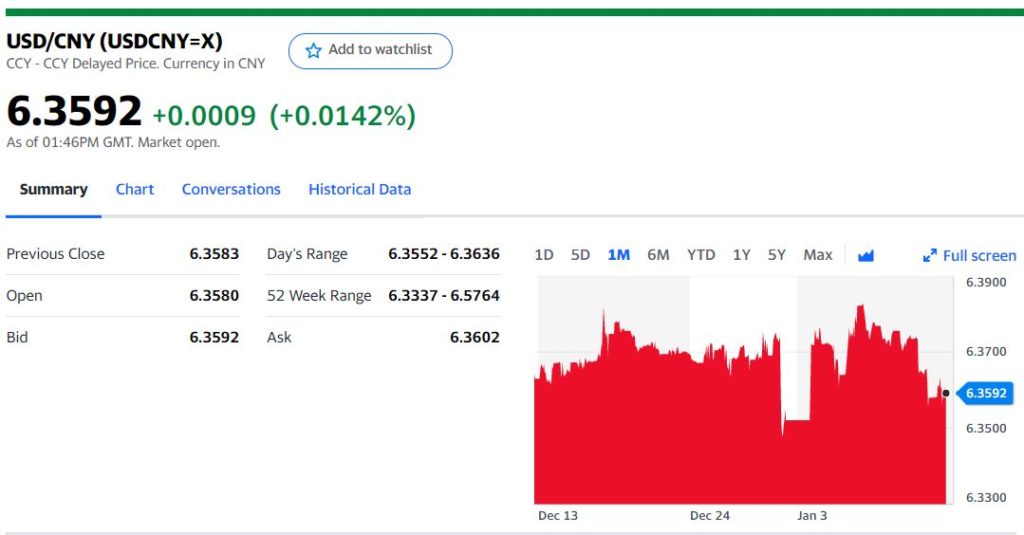

China Snapshot

Today’s Bank of China Fix 6.3542, previous 6.3658

Shanghai Shenzhen CSI 300 fell 1.64% to 4,765.92

Congestion at world’s largest shipping port in Shanghai as traffic from other ports shifts, due to COVID

US baiting China by sending carrier strike group through South China Sea

Chart: USDCNY 1 month

Source: Yahoo Finance