Source: Pixabay

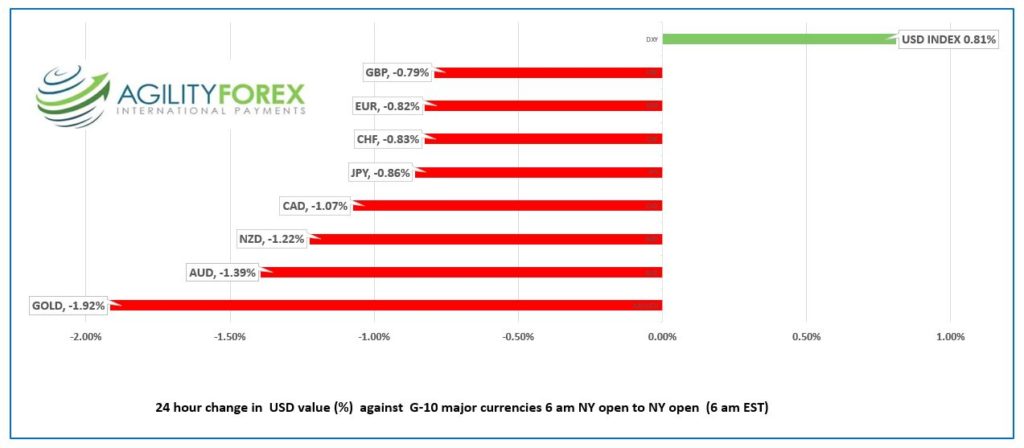

- Hawkish FOMC overshadows hawkish BoC

- US Q4 GDP soars 6.9%q/q (forecast 5.5%)

- US dollar gains with commodity bloc underperforming

FX at a Glance

Source: IFXA Ltd/RP

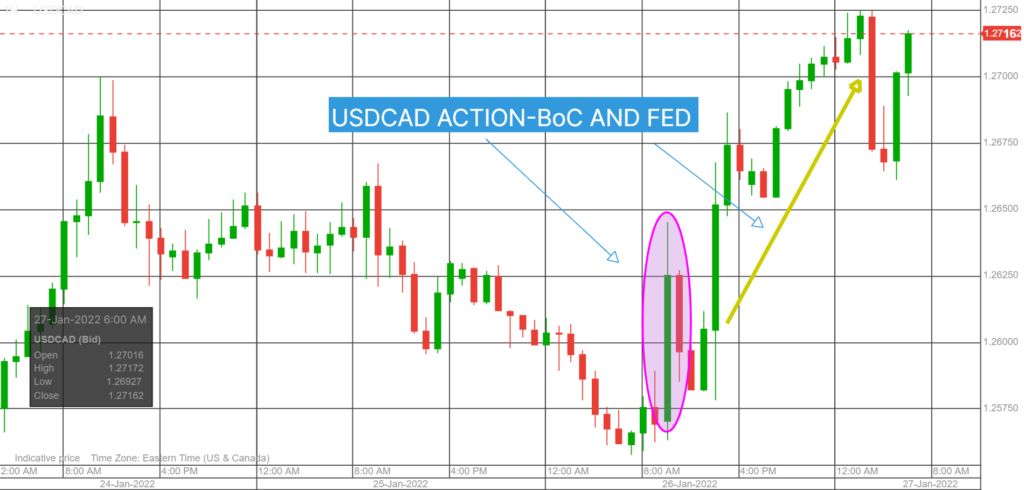

USDCAD Snapshot: Open 1.2702-06, Overnight Range-1.2659-1.2725, previous close 1.2668

USDCAD was adrift around the 1.2560 area just ahead of the Bank of Canada policy meeting. The domestic economic data had met all the requirements that Tiff Macklem needed to see before raising interest rates. He checked the box for each one in a self-aggrandizing monologue at the MPR press conference. He stressed: “Canadians can be confident that the Bank of Canada will control inflation. We are committed to bringing inflation back to target.”

But he choked on his meatloaf. There was no paradise by his dashboard light.

The BoC left interest rates unchanged but emphatically warned of a rising path for rates to control inflation. USDCAD rallied on the news, climbing from 1.2560 to 1.2640 before sliding to 1.2593 ahead of the Fed meeting.

Yesterday, Fed Chair Powell sounded more hawkish than expected and USDCAD soared and continued to do so overnight until peaking at 1.2725 at the European open. which coincided with a plunge in S&P500 futures falling to 4264 from the closing level of 4356.

USDCAD and S&P 500 correlation was on full display in early NY trading with USDCAD dips coinciding with S&P gains which will continue today.

Oil prices surged. WTI rose to $8766 in early NY trading, underpinned by supply concerns, more missile attacks on UAE, and Russia/US tensions over Ukraine. USDCAD resistance from the higher crude price was offset by short USDCAD position covering after the BoC meeting.

Technical view: The USDCAD technicals are bullish while prices are above 1.2570. A break above the 1.2730-40 area suggests further gains to 1.3000. It won’t be a one-way street as there is resistance at 1.2820 and 1.2870. A move below 1.2550 suggests 1.2450-1.2750 consolidation

For today, USDCAD support is at 1.2660 and 1.2610. Resistance is at 1.2740 and 1.2810. Today’s Range 1.2660-1.2740

Chart USDCAD 1 hour

Source: Saxo Bank

G-10 FX recap and outlook

Fed Chair Jerome Powell switched off the snooze button and acknowledged that 7.0% y/y inflation might be an issue. Of course, he didn’t come right out and say that; he muttered that “I would be inclined to raise my core PCE forecast by a few tenths.”

The Fed opened the pandora’s box of balance sheet reduction, then rattled markets with a vague outline of how it would occur. Traders are pricing in 5 rates hikes in 2022.

Global equity indexes were whippy following the FOMC meeting. The major Asia equity indexes closed with steep losses led by a 3.11% drop in Japan’s Nikkei 225. European bourses are mixed. The UK FTSE 100 is a tad higher, while the German DAX is red. S&P 500 futures are flat after a roller coaster overnight session. The US 10-year Treasury yield consolidates yesterday’s gains in the 1.82% area. The US dollar index surged to an 18-month peak rising from 96.40 to 97.14.

US Q$ GDP soared. The Bureau of Economic Analysis wrote: “Real gross domestic product (GDP) increased at an annual rate of 6.9 percent in the fourth quarter of 2021, following an increase of 2.3 percent in the third quarter. The acceleration in the fourth quarter was led by an upturn in exports as well as accelerations in inventory investment and consumer spending.”

Better than expected weekly jobless claims data offset disappointment from modestly weaker than expected US Durable Goods Orders ,

EURUSD is contending with Russian issues along with a stubbornly dovish ECB. No one cared that the German Gfk Consumer confidence survey was a tad better than expected. Instead, bearish technicals exacerbated by the drop through 1.1250-60 area are weighing on prices. A break below 1.1150 sets the stage for testing the pandemic low of 1.0780.

GBPUSD suffered from broad US dollar demand and dropped to 1.3376 from 1.3467. The risk that the Bank of England hikes rates at the February meeting is allowing GBP to outperform against EURUSD. However, Brexit and UK political issues are capping gains.

USDJPY soared to 115.24 from 114.49 due to US rate hike fever driving Treasury yields higher.

AUDUSD was the worst-performing G-10 currency overnight, falling to 0.7065 from 0.7120 due to the hawkish FOMC outlook. Traders ignored news that S&P reaffirmed Australian debt at AAA-stable.

There are plenty of US data releases today, including Q4 GDP (forecast 5.5%y/y), Durable Goods Orders, and weekly jobless claims.

Chart of the Day: US Dollar Index (USDX)

Source: Saxo Bank

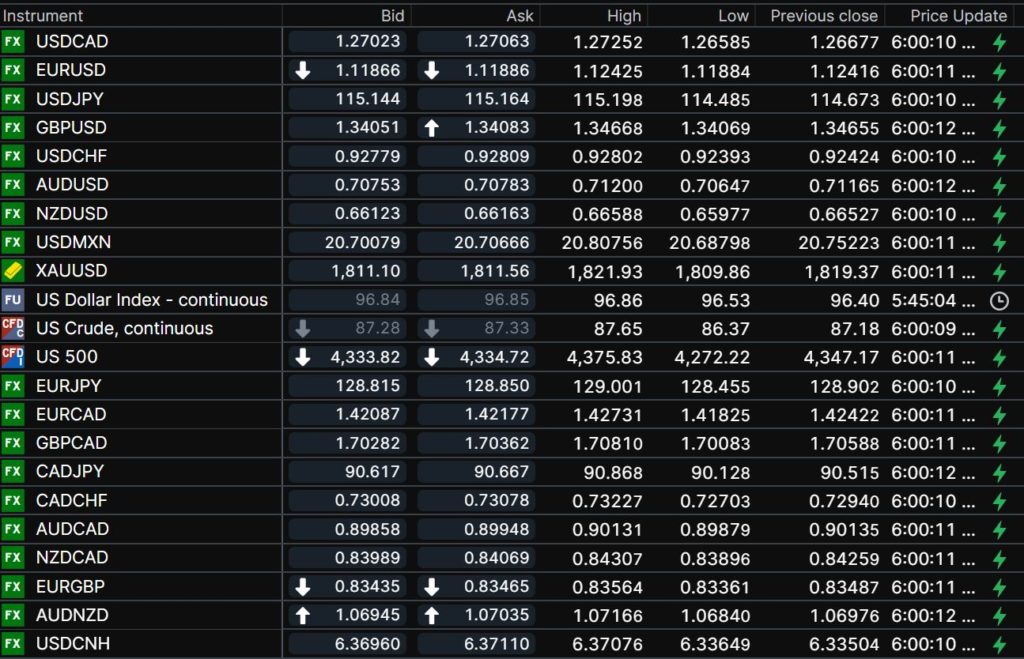

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

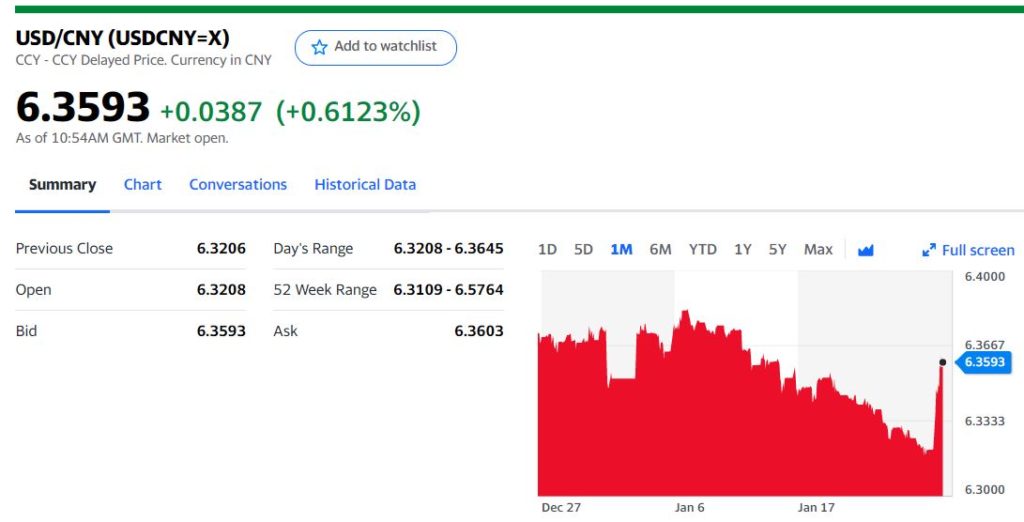

China Snapshot

Today’s Bank of China Fix 6.3382, previous 6.3359

Shanghai Shenzhen CSI 300 fell 1.96% to 4,619.88

Bloomberg articles says China discussing breaking up indebted property developer Evergrande

EU launches WTO action against China over Beijing’s spat with Lithuania.

Chart: USDCNY 1 month

Source: Yahoo Finance