Source: Pixabay

- Awaiting ECB and BoE on Thursday

- ADP employment drops 301,000

- US dollar in retreat, CAD underperforms

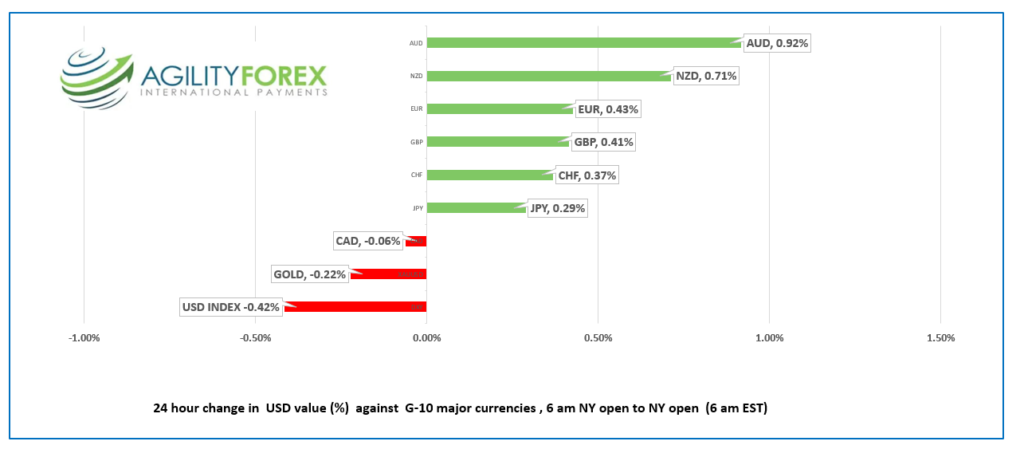

FX at a Glance

Source: IFXA Ltd/RP

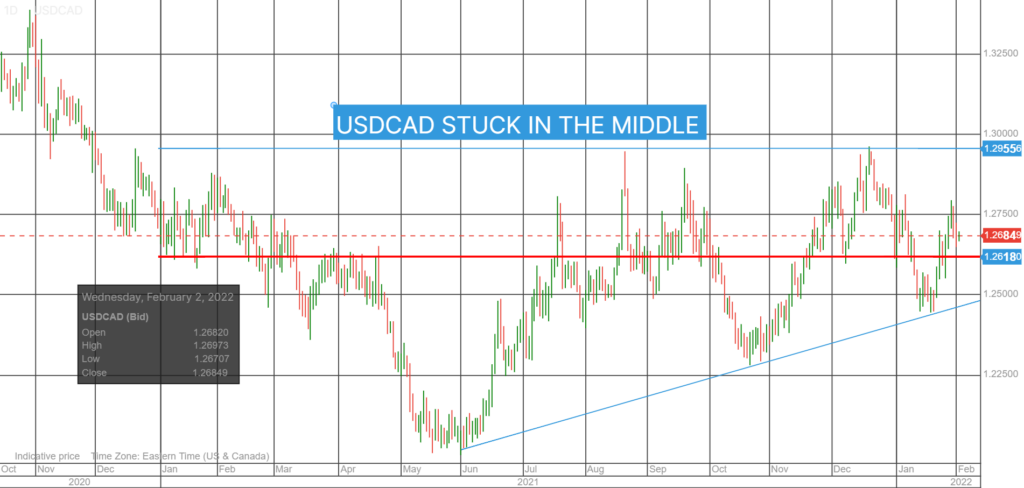

USDCAD Snapshot: Open 1.2682-86, Overnight Range-1.2677-1.2697, previous close 1.2685

USDCAD traded sideways in an uneventful FX market overnight after ignoring yesterday’s better than expected November GDP (actual 0.8% m/m vs forecast 0.3% m/m). However, the results were a tad stale, and they did not capture the impact of Omicron.

Global equity indexes are trading as if it’s a “risk-on” environment, while FX markets are cautious ahead of Thursday’s ECB and BoE monetary policy meetings.

WTI oil is trading just below its recent peak ahead of Opec’s announcement. Traders appear to be ignoring speculation that the cartel would increase production in March or that Saudi Arabia may provide a one-off boost.

USDCAD may see some late afternoon movement if Governor Tiff Macklem’s remarks to the Standing Senate Committee on Banking offer any fresh insight.

Until then, USDCAD will remain choppy inside its well-defined range.

Technical view: The intraday USDCAD technicals are bearish below 1.2700 which represents the top of the downtrend channel from the end of December. A move below 1.2620 (bottom of channel targets 1.2550 while a topside break shifts focus to 1.3000.

Longer term, USDCAD is just above the middle (1.2620) of its 2021, 1.2280-1.2960 range

For today, USDCAD support is at 1.2640 and 1.2610. Resistance is at 1.2710 and 1.2750. Today’s Range 1.2640-1.2720

Chart USDCAD daily-one year

Source: Saxo Bank

G-10 FX recap and outlook

ADP employment surprised with a 301,000 drop, which was far below the forecast (207,000) and last month’s 776,000 increase. The results imply a downside risk to Friday’s NFP forecast of 150,000. Nevertheless, the US is already at full-employment and neither the ADP nor NFP reports will have any bearing on the March FOMC decision.

The few Asian equity indexes that were open followed Wall Streets’ lead and closed with gains. The Nikkei 225 rose 1.68% while Australia’s ASX 200 gained 1.17%. The UK FTSE 100 leads European bourses higher, and S&P 500 and DJIA futures firmed. Oil and gold prices are modestly higher, while the US 10-year Treasury yield is steady at 1.783%.

Traders appear to be bored with the Russia and NATO dance over the Ukraine, while Chinese New Year festivities sucked the energy from Asia markets.

FX traders are content to languish on the sidelines awaiting tomorrow’s ECB and BoE meetings.

EURUSD has caught a bit of a bid and rallied from 1.1268 to 1.1313 in New York due to speculation (hope) that ECB President Christine Lagarde will follow Fed Chair Powell’s example and adopt a hawkish interest rate outlook. That view gained traction today after Eurozone inflation rose 5.1% y/y. Core inflation rose 2.3% in January, down from 2.6% in December but above the forecast of 1.9%.

GBPUSD is also underpinned by rate hike expectations. The BoE is almost universally expected to hike rates 0.25% at Thursday’s meeting. Traders ignore ongoing political issues and reports that PM Johnson will face a “no-confidence” vote today. The UK/EU Brexit spat about the Northern Ireland borders is also on the radar, with the Irish DUP agricultural minister contemplating halting border checks.

USDJPY is at the bottom of its overnight 114.33-114.79 range, remaining under pressure from broad US dollar weakness and steady to soft US Treasury yields.

AUDUSD traded at 0.7153 in NY today after touching 0.7130 yesterday, when the RBA surprised many players with a dovish monetary policy statement. RBA Governor Philip Lowe repeated, “the end of QE did not mean an increase in the cash rate was imminent.” Then he muddied the waters saying “If things go well, and the economy performs strongly, then there are clearly scenarios where we would be increasing rates later this year if some of the uncertainties are resolved.”

NZDUSD traded modestly firmer. The NZ unemployment rate fell to 3.2% m/m from #.4% but that news was offset, as the rest of the data was weaker than expected.

Chart of the Day: EURUSD 4 hour

Source: Saxo Bank

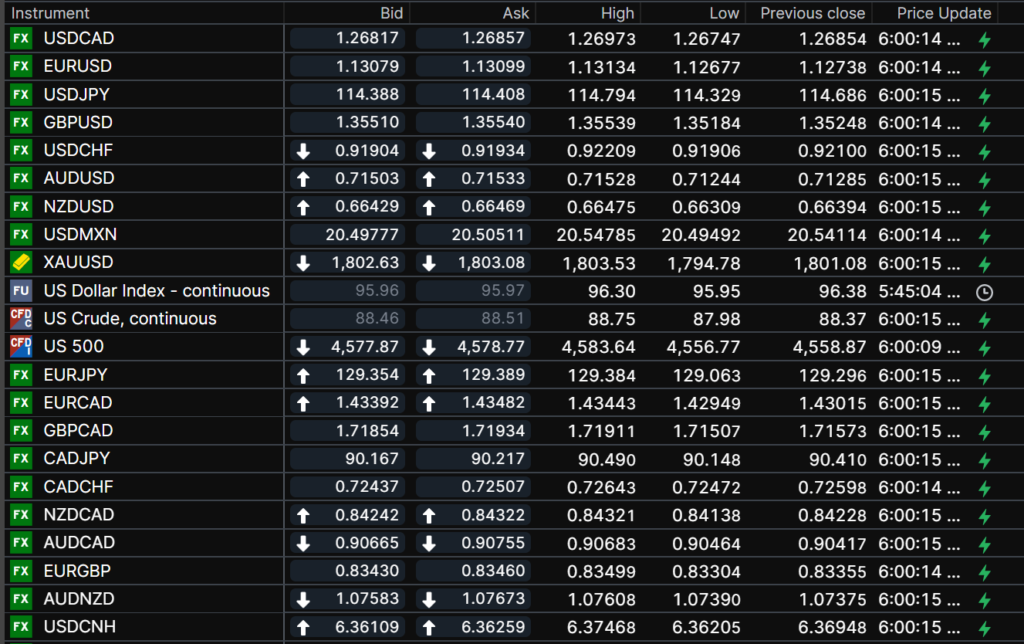

FX open, high, low, previous close as of 6:00 am ET

Chart: Saxo Bank

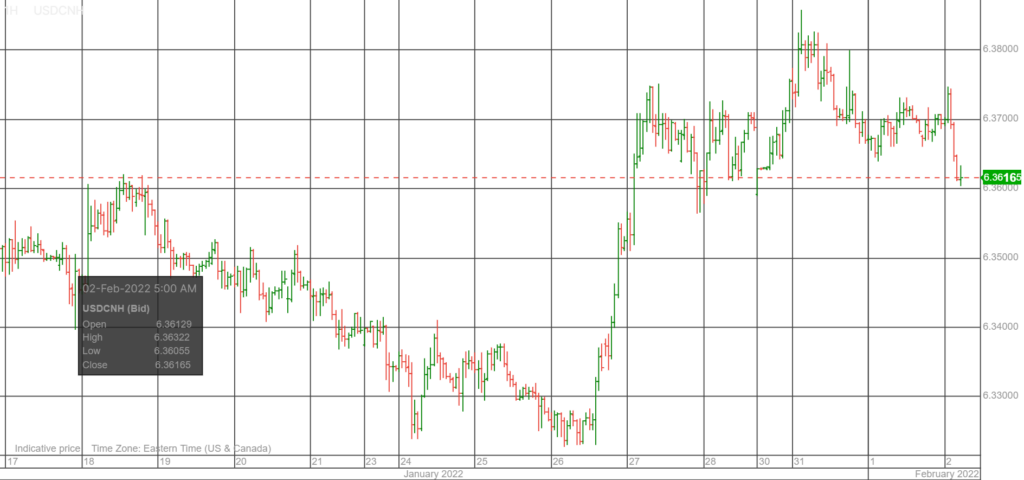

China Snapshot

Today’s Bank of China Fix 6.3746, previous 6.3746-Close

Shanghai Shenzhen CSI 300 closed

Chinese New Year-January 31 to February 15.

Chart: USDCNH (offshore yuan) hourly-20 days

Source: Saxo Bank