Photo: Wikimedia commons

- Fed hikes 75bps and risk sentiment improves

- US Q2 GDP (preliminary) falls 0.9%

- US dollar retreats post FOMC, opens sharply lower

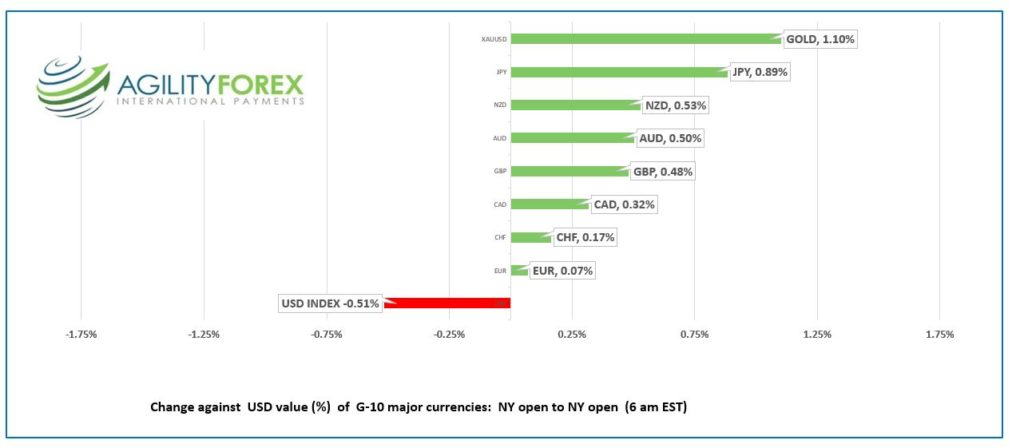

FX at a glance:

Source: IFXA Ltd/RP

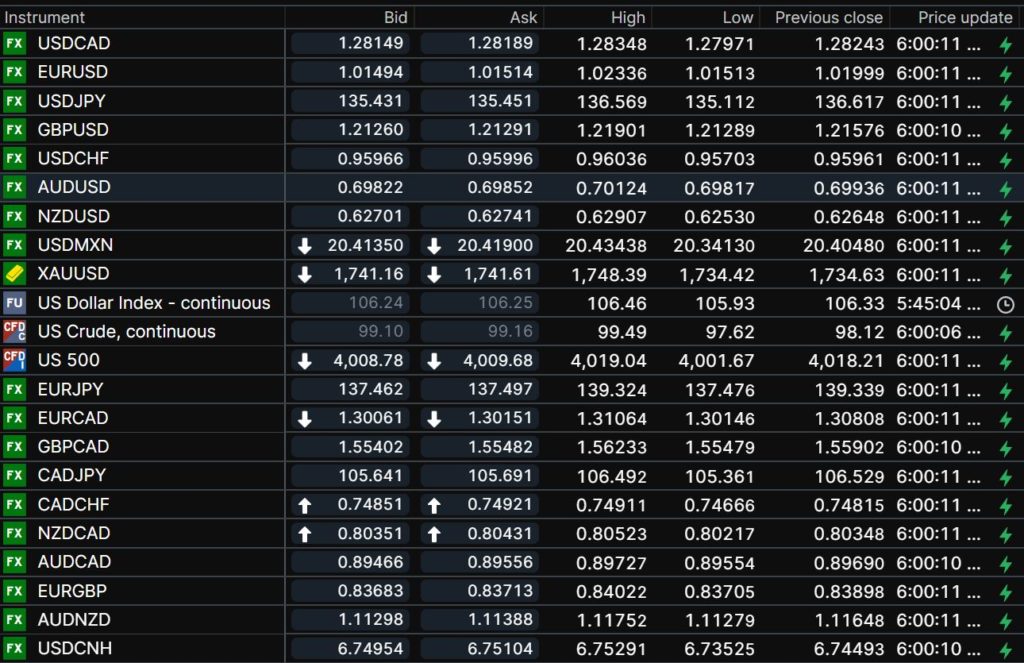

USDCAD Snapshot: open 1.2810-14, overnight range 1.2797-1.2835, close 1.2824

It is fair to say that Bank of Canada Governor Tiff Macklem is muttering that central bankers are not getting any respect. He hiked Canadian rates by 100 basis points on July 13, and the Canadian dollar sank. Yesterday, Jay Powell and colleagues bumped rates 75 bps and promised more hikes and the greenback tanked.

Back in the day, a rate hike of 75 or 100 points would almost guarantee a higher currency. Not today. Traders are ignoring the short-term impact of higher interest rates on the economy, content to believe that central bankers are in control, inflation will fall, the unemployment rate will remain steady, and Russia and Ukraine are merely having a disagreement.

USDCAD is undermined by a rebound in commodity prices especially WTI oil which climbed from $94.45/barrel yesterday to $99.49 overnight. Prices are supported by the weaker greenback and sustained demand in the face of supply concerns. Wednesday the EIA reported a 4.52 million barrel drop in inventories for the week ending July 21 while noting that inventories are 4% below their 5-year average.

The Canadian data calendar is empty.

USDCAD technical outlook

The intraday USDCAD technicals are bearish below 1.2850 looking for a decisive break below 1.2810 to set the stage for an eventual test of 1.2500-20 area. A rebound above 1.2850 suggests further consolidation in a 1.2810-1.2920 range. A break above 1.2920 negates the downside and puts 1.3050 in play.

For today, USDCAD support is at 1.2810 and 1.2780. Resistance is at 1.2850 and 1.2880. Today’s Range 1.2790-1.2870

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

“The Fed be nimble, the Fed be quick, incoming data makes them tick.” That about sums up the gist of Wednesday’s FOMC monetary policy statement and Chair Powell’s press conference.

It appears that the Committee tired of being mocked for erroneous economic outlooks and forecasts, so they dispensed with “forward guidance,” except to say it “anticipates that ongoing increases in the target range will be appropriate.”

Wall Street reacted to the second 75bp rate hike like it was a rate cut. The S&P 500 roared higher and closed with a 2.62% gain which paled in the face of the 4.06% jump in the Nasdaq.

Those gains are a bit of a head-scratcher. The Fed plans on hiking rates until Fed funds reach the 3.25-3.5% level by the end of the year and gave zero indication that rate hikes would stop there. Mr Powell said the Committee needs to see compelling evidence that inflation is coming down. My guess is that another 1.25 bp rate increase won’t do anything to curtail rising prices.

The US is in recession. That is, if you believe that two consecutive quarters of negative growth equals a recession. Preliminary Q2 GDP fell 0.9% y/y (forecast 0.4%) which is rekindled the “recession-no recession” debate.

US weekly jobless claims were close enough to forecasts (actual 256,000 vs consensus 253,000) to be a non-factor.

Asian equity traders were a tad less-enthusiastic. They flipped between gains and losses before finally finishing the session modestly higher. Japan’s Nikkei 225 index gained 0.38%, while Australia’s ASX 200 rose 0.97%.

European bourses gave back opening gains and flittered around unchanged in early NY trading. S&P 500 futures are trading defensively while gold and WTI oil prices rose 1.18% and 2.04%, respectively.

EURUSD is whippy inside a 1.0100-1.0232 range. The bottom was reached at Wednesday’s European close, and the peak was seen in the wake of the FOMC announcement. Today, EURUSD dropped from 1.0210 to 1.0150 after weak eurozone data. The EU Commission said its “Economic Sentiment Indicator (ESI) plummeted in both the EU (-4.2 points to 97.6) and the euro area (-4.5 points to 99.0), falling below its long-term average. The Employment Expectations Indicator (EEI) also decreased markedly (-3.6 points to 106.6 in the EU and -3.2 points to 107.0 in the euro area).”

The dire Euro area economic outlook and looming energy crisis will leave EURUSD on the defensive and looking for further losses to parity.

GBPUSD rallied from 1.2020 prior to the FOMC meeting to 1.2183 in the aftermath, then consolidated the gains in a 1.2125-1.2190 band overnight. The gains were fueled by broad US dollar weakness and EUGBP selling. The intraday GBPUSD technicals are bullish above 1.2030, looking for a move above 1.2190 to extend gains to 1.2330.

USDJPY spiked to 137.40 around the FOMC meeting and then dropped sharply to 135.11 in Asia. Prices are consolidating the losses in a 135.20-135.60 range in NY. The drop is due to soft US Treasury yields, with the 10-year languishing in the 2.78% area.

AUDUSD jumped aboard the “soft dollar” bandwagon and rallied from 0.6915 ahead of the FOMC meeting to 0.7012, then consolidated the gains in a 0.6982-0.7012 band overnight.

NZDUSD tracked AUDUSD moves in a 0.6253-0.6291 range while traders ignored weaker than expected NZ retail sales data (actual 0.2% vs forecast 0.5%).

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

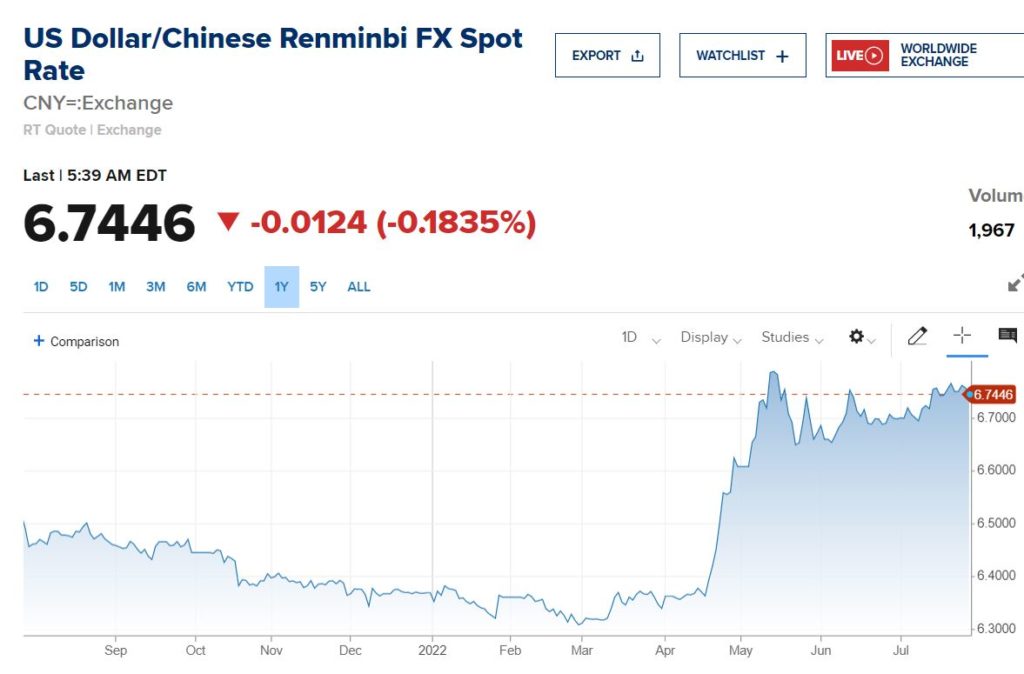

Today’s Bank of China Fix 6.7411, previous 6.7731

Shanghai Shenzhen CSI 300 rose 0.01% to 4,225.67

Bloomberg story argues that Xi Jinping is planning to be a force in Chinese politics beyond a planned third term. He said, “Against the backdrop of accelerating global changes unseen in a century, and more complex risks, challenges, contradictions and problems, the fundamental task is to run our own affairs well.”

Chart: USDCNY 1 month

Source: CNBC