Photo: Wikimedia

- $2 Trillion worth of options expire today

- Canada Retail Sales Rise 1.1% m/m beating forecast

- US dollar surges as Treasury yields jump

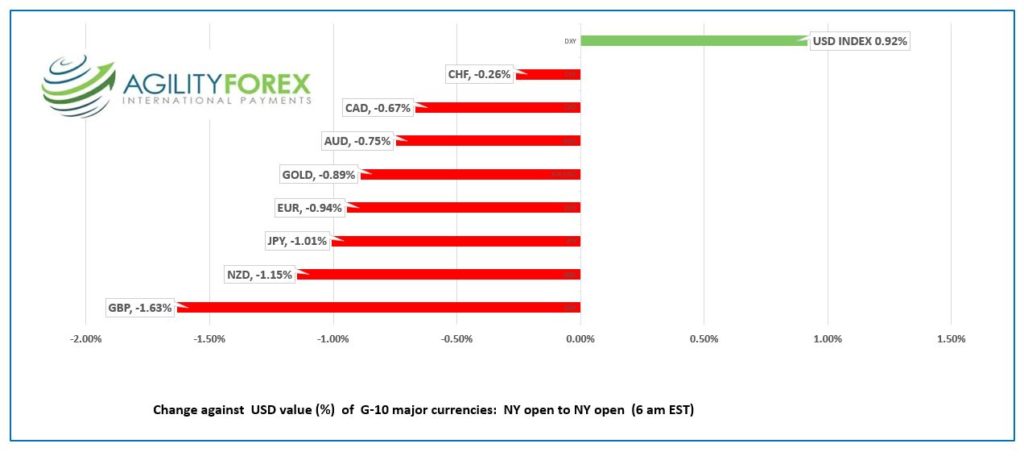

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.2973-77, overnight range 1.2946-1.3002, close 1.2947

USDCAD has been on a one-way street higher since yesterday’s NY open, fueled by hawkish Fed-speak and a surge in Treasury yields that fueled broad US dollar gains.

Trading may be extra-erratic today as $2.0 trillion in option expiries across all asset classes roils thin summer markets. If so, USDCAD will not be immune.

Canada June Retail Sales climbed 1.1% m/m, well above the 0.3% m/m predicted and it was the sixth consecutive increase.

WTI oil prices consolidated Thursday’s gains in $89.06-$90.80/barrel range but are poised to end the week down 2.6% from last Friday’s close. Gains are limited because of rising fears of a global recession and the possibility of new supply from Iran.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish (on 4-hour chart) while trading above 1.2910, looking for a break above 1.3010 to extend gains to 1.3080 then 1.3140. A move below 1.2910 negates the upside pressure and suggests more 1.2750-1.3000 range trading ahead. A topside break is supported by the July/August Fibonacci retracement analysis which projects a move to 1.3030 with the break above 1.2912.

For today, USDCAD support is at 1.2940 and 1.2910. Resistance is at 1.3000-1.3010, and 1.3040. Today’s range: 1.2940-1.3030

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The US dollar caught a bid yesterday and hasn’t looked back. St Louis Fed President James Bullard got the ball rolling when he told the Wall Street Journal, “I would lean toward the 75 basis points at this point. Again, I think we’ve got relatively good reads on the economy, and we’ve got very high inflation, so I think it would make sense to continue to get the policy rate higher and into restrictive territory.”

Kansas City Fed Chief Ester George wants to see more rate hikes but said, “The question of how fast that has to happen is something my colleagues and I will continue to debate.”

Cleveland Fed President Neel Kashkari sounded like he agreed with Bullard, but he didn’t say anything about the size of the next rate hike. Instead, he warned that a recession might be unavoidable in the drive to lower inflation.

Bond traders noted hawkish comments from Fed officials and concluded that perhaps the current Treasury yield did not reflect the Fed’s reality. They sold bonds, and the US 10-year Treasury yield popped to 2.965% in NY from 2.845% yesterday.

Asian equity indexes closed relatively unchanged, and European Bourses are in negative territory.

S&P 500 and DJIA futures have lost 0.95% and 0.77%, respectively (as of 5:40 am PDT). WTI oil is down 1.72% from the close, and gold has slid 0.47% to $1750.25.

EURUSD dropped from 1.0193 yesterday to 1.0047this morning, with a drop to 1.000 almost inevitable. The single currency is getting hammered from European recession woes, supply chain disruptions from the Russia/Ukraine war, the ongoing energy crisis, and widening US and ECB interest rate differentials.

GBPUSD dropped from 1.2077 on Thursday to 1.1817 in NY trading today suffering from the same malaise as EURUSD, in addition to its self-inflicted wounds. Those wounds include political uncertainty, ongoing Brexit tensions, a rash of ongoing or upcoming labour disruptions, and sky-high inflation. A move below 1.1750 suggests a test of the Brexit-vote low of 1.1448 is likely.

USDJPY caught Treasury yield fever and rallied from 134.65 Thursday to 137.13 this morning. Japanese inflation was higher than expected. July CPI rose 2.6% y/y, easily beating the 2.2% consensus forecast.

AUDUSD is trading at the bottom of its 0.6877-0.6918 range, weighed down by broad US dollar strength. NZDUSD mirrored the AUDUSD decline and fell from 0.6256 to 0.6200.

There are no US economic reports of note, leaving the massive option expiries to dictate FX direction.

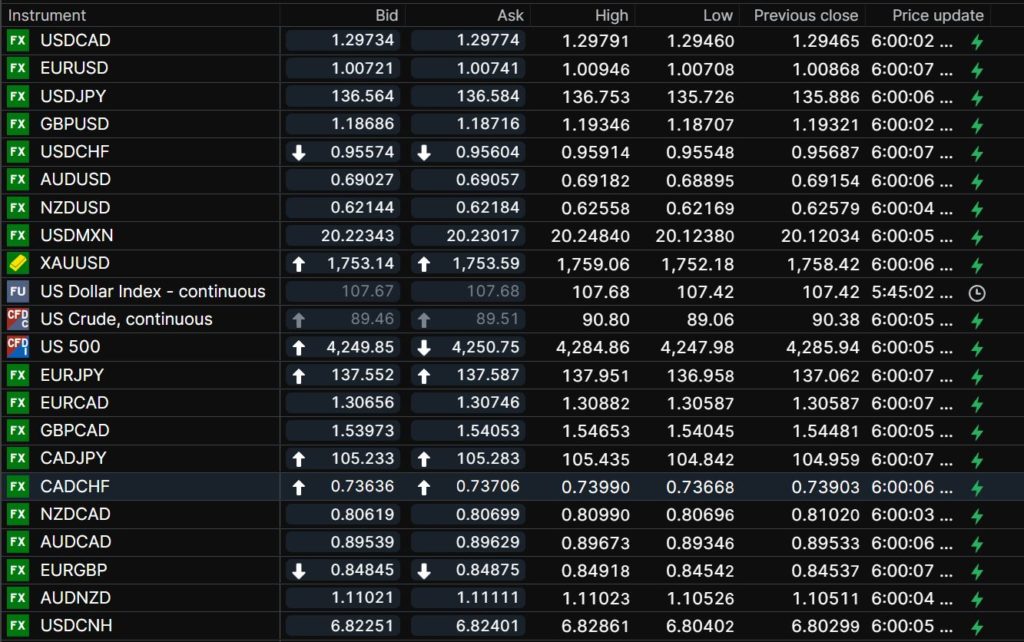

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 6.8065, previous 6.7802

Shanghai Shenzhen CSI 300 fell 0.69% to 4,151.07

Analysts speculating that PboC will cut Loan Prime Rates on Monday.

Traders fear PboC will “devalue CNY” by allowing USDCNY to sustain gains above 7.0%

Chart: USDCNY 1 month