Source: New Line Cinema

- Eurozone Sentiment continues to sour

- European equity index and Wall Street futures rebound

- US dollar trading sideways to softer due to month-end flows

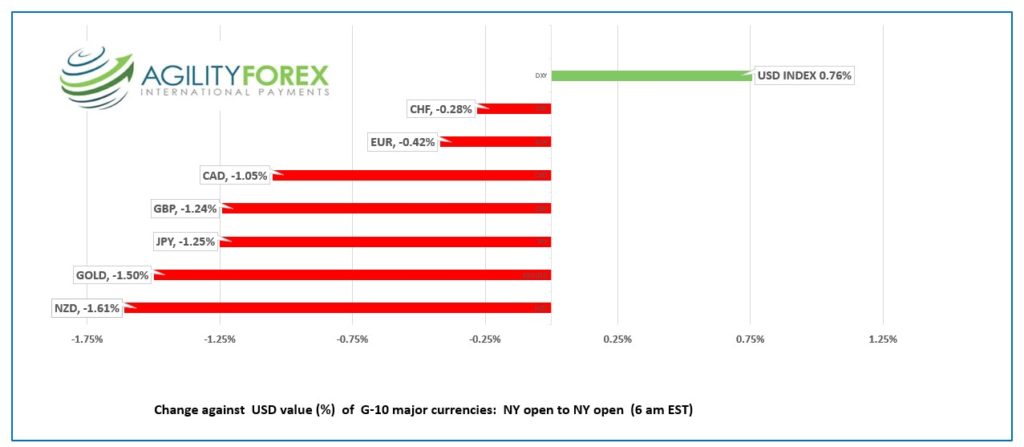

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.2977-81, overnight range 1.2974-1.3024, close 1.3011

USDCAD gave back all of Tuesday’s gains due to widespread month-end US dollar selling, and mildly improved risk sentiment.

USDCAD direction continues to be dictated by broad US dollar moves and risk sentiment as measured by S&P 500 price action. Even so, better than expected GDP data tomorrow and expectations for a hawkish outcome at next week’s Bank of Canada monetary policy meeting should limit USDCAD gains.

WTI oil is trading near the bottom of its overnight $94.59-$97.62/b range do the ongoing supply/demand debate and US dollar price swings.

Canada’s Q2 Current Account balance disappointed at just $2.7 billion compared to expectations for an increase to $6.6 billion from 5.03 billion. The news did not affect USDCAD

USDCAD Technical outlook

The intraday USDCAD technicals choppy inside a 1.2940-1.3070 range. The hourly chart shows a minor downtrend from 1.3070 intact while prices are below 1.3010, while the uptrend from August 11 provides support at 1.2940. A break below 1.2940 will target 1.2880, while a move above 1.3030 targets 1.3070.

For today, USDCAD support is at 1.2940 and 1.2910. Resistance is at 1.3010 and 1.3140. Today’s range: 1.2940-1.3030

Chart: USDCAD 1 hour

Source: Saxo Bank

G-10 FX recap and outlook

The financial market panic following Fed Chair Powell’s Jackson Hole speech last Friday eased somewhat overnight. Traders have turned their focus to month-end portfolio rebalancing flows, where analysts at Morgan Stanley and Citibank expect to see US dollar selling.

FX markets will remain in flux until Friday’s US employment report, which is expected to show a gain of 285,000 jobs while the unemployment rate remains at 3.5%.

Asian equity indexes closed higher except for those in China. Japan’s Nikkei 225 index gained 1.14%, while Australia’s ASX 200 rose 0.47%.

European bourses are enjoying a robust session led by a 1.68% gain in the German Dax. However, oil and gold prices are modestly lower

S&P 500 futures are up 0.44%, DJIA futures gained. 034%, but both are well below levels seen in Europe. The US 10-year Treasury yield retreated from 3.11% at yesterday’s close to 3.08% in NY.

The Case-Shiller Home Price Index was a tad weaker than forecast at 18.6% y/y in June (forecast 19.5% y/y vs previous 20.5%).

EURUSD climbed from 0.9998 to 1.0054 thanks to month-end flows but gave back most of those gains in NY trading. Comments from ECB Chief Economist Philip Lane provided some support for the single currency, even though he appeared to advocate for a smaller rate increase then the 75 bp bump suggested by another ECB policymaker. He said the ECB should hike rates at rates at a “steady pace,” which he described as one “that is neither too slow nor too fast, in closing the gap to the terminal rate is important.”

The Eurozone Economic Sentiment Indicator fell to 97.6 from 98.9 in August which underscored recession concerns and limited EURUSD gains.

GBPUSD is given back earlier gains and is trading near the bottom of its 1.1689-1.1759 range. Price action is dictated by month-end flows, but gains are limited due to UK recession risks which are exacerbated by the energy crisis. Credit Suisse is forecasting UK inflation at 15% in January 2023, which is higher and later than their previous forecast.

USDJPY traded in a 138.15-138.77 band supported by steady US 10-year Treasury yields and widening US and Japan interest rate differentials.

AUDUSD traded in a 0.6875-0.6955 range overnight but slipped to 0.6919 in NY trading. NZDUSD mirrored AUDUSD moves and both currency pairs are tracking broad US dollar sentiment.

Today’s US data includes Consumer Confidence, and JOLTS Job openings.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 6.8802, previous 6.8698

Shanghai Shenzhen CSI 300 fell 0.34% to 4,075.79

Chinese stock markets lower due to Covid disruptions in Dalian region and a district in Shenzhen.

Chart: USDCNY 1 month

Source: Bloomberg