Source: clipground

- Eurozone inflation hits 9.1%-ECB now expected to hike 75 bps

- Canada Q2 GDP slows to 3.3% (forecast 4.5%)

- US dollar extends gains against majors

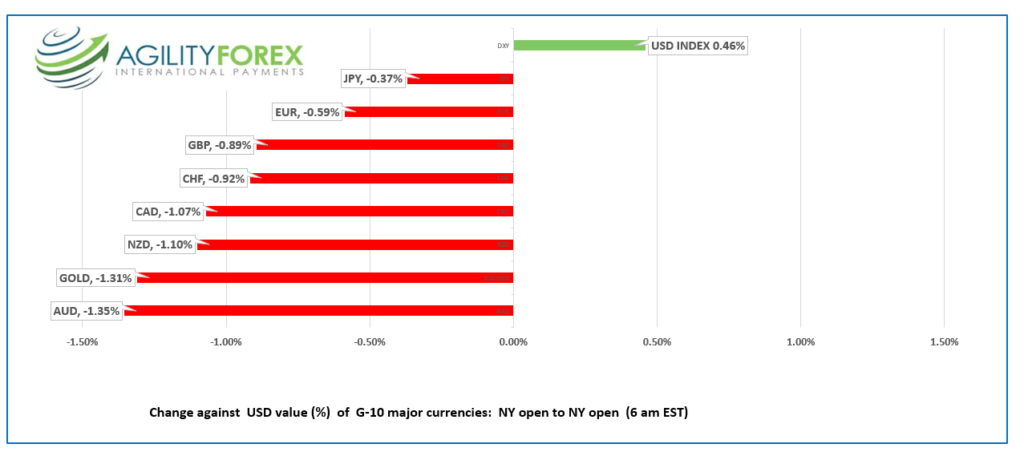

FX at a glance:

Source: IFXA Ltd/RP

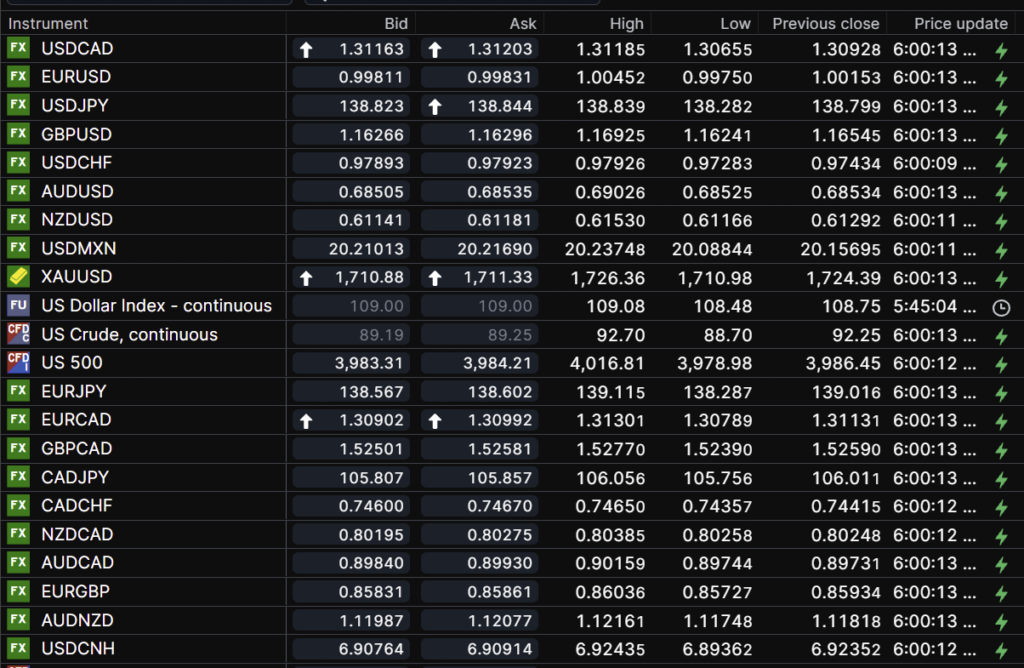

USDCAD Snapshot: open 1.3116-20, overnight range 1.3066-1.3116, close 1.3093

“As God is my witness, I thought turkeys could fly. WKRP in Cincinnati station manager Arthur Carlson said those words after his Thanksgiving promotion went awry. Loonie bulls are having the same thought.

USDCAD is on a tear despite domestic data suggesting prices should be falling. The data shows a strong employment picture, with a hawkish central bank, with consumers are still spending.

However economic growth is slowing. June GDP rose 0.1% and 3.3% y/y in Q2. The forecast was for GDP to rise 4.5% y/y although the risks were to the downside after aggressive BoC rate hikes knocked home sales lower.

None of that matters.

It is Fed Chair Jerome Powell and the FOMC’s monetary policy outlook that is driving FX, bond, commodity and equity trading. Traders are beginning to believe policymakers when they say they will bring inflation down to the 2.0% target. Mr Powell reiterated that desire in his Jackson Hole speech last Friday, while invoking the spectre of 1978, Paul Volker.

The US dollar rallied, stocks tanked, and they haven’t recovered yet. Markets are extra-volatile today due to month-end rebalancing flows.

USDCAD Technical outlook

USDCAD broke above resistance in the 1.3070-90 area, which contained gains since the middle of July. The move is bullish and suggests further gains to the 2022 peak of 1.3213, on a move above 1.3140. A drop below 1.3050 would alleviate the upside pressure but only a break below 1.2960 would negate the bullish bias.

Keep in mind, that the FX market is still in summer-holiday-mode, and liquidity is poor, which exaggerates prices swings. USDCAD needs to spend a few days above 1.3070 to confirm the upside break.

For today, USDCAD support is at 1.3060 and 1.3020. Resistance is at 1.3140 and 1.3170. Today’s range: 1.3060-1.3140

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Fed Chair Powell and his colleague’s hawkish inflation-fighting rhetoric, China/Taiwan tensions, and month-end portfolio rebalancing flows are roiling markets.

Wall Street closed in the red, with the S&P 500 losing 1.10%. The futures market suggests the bleeding has stopped, at least for now, as S&P futures are 0.21% higher. Asian equity markets closed in negative territory, and European bourses also suffered losses, although not dramatically.

WTI oil plunged 8.5% since yesterday’s $97.51/barrel peak. The steep drop is due to increased recession fears from rising global interest rates and concerns over slumping Chinese growth. Prices are also hurt because Russia sanctions only hurt Europe since China and India stepped up crude purchases.

Russia is playing “silly buggers” with the Nord Stream 1 pipeline. They shut it down, saying it needed repairs, but the shutdown is meant to disrupt EU plans to stockpile supplies.

The “new and improved” ADP employment report returned after a two-month absence to improve the accuracy of the results. ADP reported, “Private sector employment increased by 132,000 jobs in August, and annual pay was up 7.6% according to the August report.” The forecast was for an increase of 288,000.

EURUSD churned in a 0.9972-1.0045 band. A rally following a higher Eurozone inflation print (actual 9.1% vs 8.9%in July) was short-lived. Nevertheless, the results convinced some economists to forecast a 75 bp rate hike at next week’s ECB meeting.

However, EURUSD gains are capped due to recession concerns stemming from the war in Ukraine and the energy crisis.

GBPUSD fell to 1.1615 in NY today after falling from 1751 yesterday. Month-end portfolio rebalancing flows exacerbated the plunge.

GBPUSD is vulnerable to further losses from the ongoing leadership vacuum and energy crisis.

A break of 1.1610 targets 1.1500, a level last seen in 1985. If broken, there is not much support ahead of 1.0400.

USDJPY spent a whippy 24 hours in a 136.05-139.05 range and is sitting at 138.76 in NY. Month-end demand and the higher US 10-year treasury yield (3.144%) support prices.

AUDUSD is at the bottom of its 0.6846-0.6903 range due to month-end flows and weaker commodity prices.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

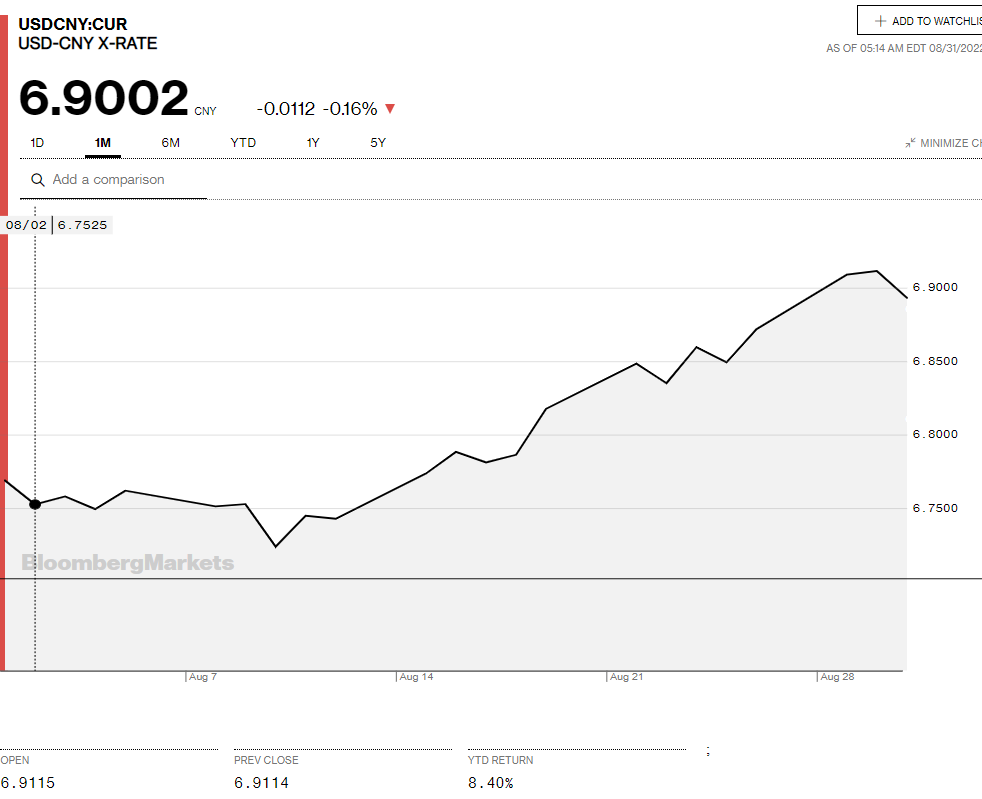

China Snapshot

Today’s Bank of China Fix: 6.8906, previous 6.8802

Shanghai Shenzhen CSI 300 rose 0.07% to 4,078.84

Reuters reports Chinese State-owned banks selling USDCNY

Chart: USDCNY 1 month

Source: Bloomberg