Source: Wikimedia commons

- Biden ratchets up geopolitical tensions

- UK markets closed, risk sentiment negative

- US dollar gains slightly on hawkish Fed fears

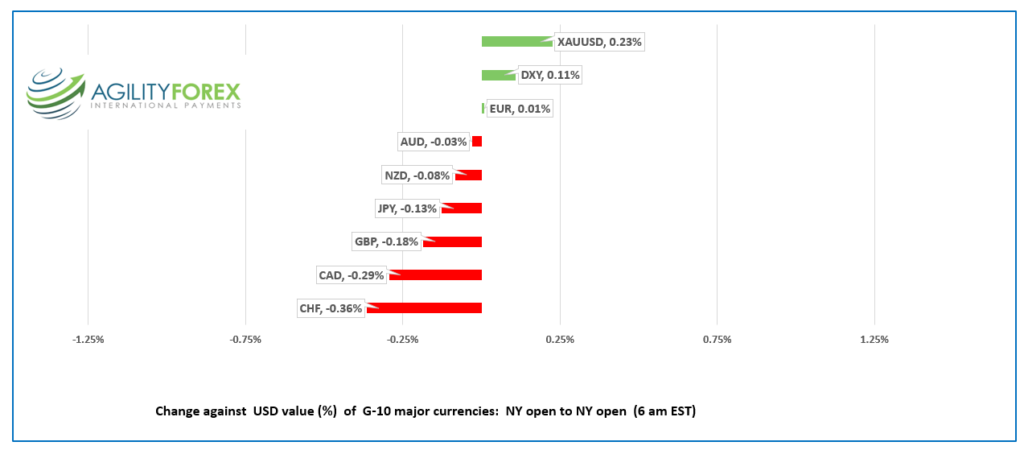

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3307-11, overnight range 1.3252-1.3314, close 1.3265

USDCAD started climbing in Asia and continued into the NY open, on the back of widespread US dollar strength ahead of Wednesday’s FOMC meeting.

S&P 500 futures are under pressure, having dropped 0.90% and is underpinning USDCAD.

Canada has a similar inflation story as the one in the US and the Bank of Canada has been quicker and more aggressive than the Fed in addressing it. However, the currency has not received any benefit from the surge in the BoC overnight rate from 0.25% in January 2022 to 3.25% on September 7. The BoC is widely expected to match September’s 75 bp hike at the October 26 meeting.

WTI oil prices are traded with a bearish bias and dropped to $83.43/b from $86.20/b overnight. Prices are weighed down by concerns of a global economic slowdown dragging down demand.

Canada Industrial Product Price Index fell 1.2% m/m in August (forecast -2.7%) while the Raw Material Price Index dropped 4.2% (forecast 0)

USDCAD Technical outlook

The intraday USDCAD are bullish. The uptrend from last Tuesday is intact while prices are above 1.3205, a previous triple top, and now guarded by support at 1.3250. The breach of minor resistance at 1.3310 targets 1.3370 then 1.3430. A break below 1.3250 suggests further losses to 1.3210.

For today, USDCAD support is at 1.3260 and 1.3240. Resistance is at 1.3340 and 1.3370. Today’s range: 1.3260-1.3350

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The week begins with rising geopolitical tensions, souring risk sentiment, and a massive storm in and around Japan.

President Joe Biden said the US would defend Taiwan “if there was an unprovoked attack.” Then the befuddled geriatric said, “there is a one-China policy and Taiwan makes its own judgements on independence. Taiwan leaders welcomed the comments, especially after reports of more Chinese fighter jets in Taiwan airspace. The White House said there is no change to the “one-china policy.

Chinese officials were not impressed, and they lodged “stern representation” against these comments.

Japan has evacuated 9 million people in the face of Typhoon Nanmadol which is a crummy way to spend a national holiday.

Traders fear the fed.

Not really, but they fear the fed may overcompensate for missing the signs inflation was becoming problematic and overreact by hiking rates too aggressively. A 75 bp rate hike is expected Wednesday, along with a hawkish statement.

The Typhoon and the Japanese holiday sapped liquidity from Asian markets that were risk averse following the weak close on Wall Street Friday and ahead of the FOMC meeting Wednesday. Australia’s ASX 200 closed down 0.26%.

European bourses are in the red, led by a 1.20% drop in the French CAC index. UK markets are closed. DJIA and S&P 500 futures fell 0.77% ahead of the NY open, while gold dropped 0.63% and WTI oil fell 1.30%. The US 10-year Treasury yield is at 3.448%.

EURUSD peaked at 1.0029 in early Asian trading, then slid steadily to 0.9967 just before NY opened. Bundesbank President Joachim Nagel is advocating for higher ECB rates even after an expected rate hike in October.

UK markets are closed. GBPUSD dropped from 1.1441 to 1.1365 due to broad US dollar strength and thin markets. The UK’s penchant for pomp and pageantry is on full display for the funeral of Queen Elizabeth. The Bank of England is expected to raise rates by 50 bps at Thursday’s meeting.

USDJPY rallied from 142.65 to 143.54 due to broad US dollar strength and expectations for a hawkish FOMC outcome on Wednesday. However, traders are cautious due to fears of BoJ intervention if prices rise above 145.00.

AUDUSD traded defensively in a 0.6675-0.6733 range. Hopes for AUDUSD support as China eased lockdown restrictions did not materialize as the focus was on the FOMC outlook. NZDUSD mirrored AUDUSD moves and traded in a 0.5945-0.6001 range.

The US data calendar is empty.

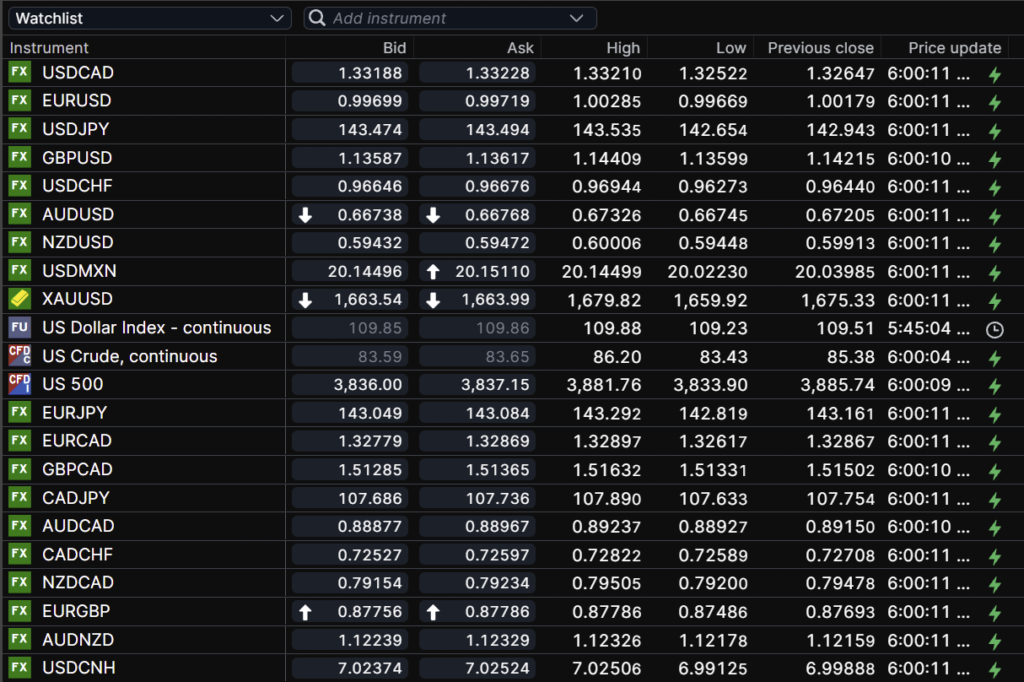

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

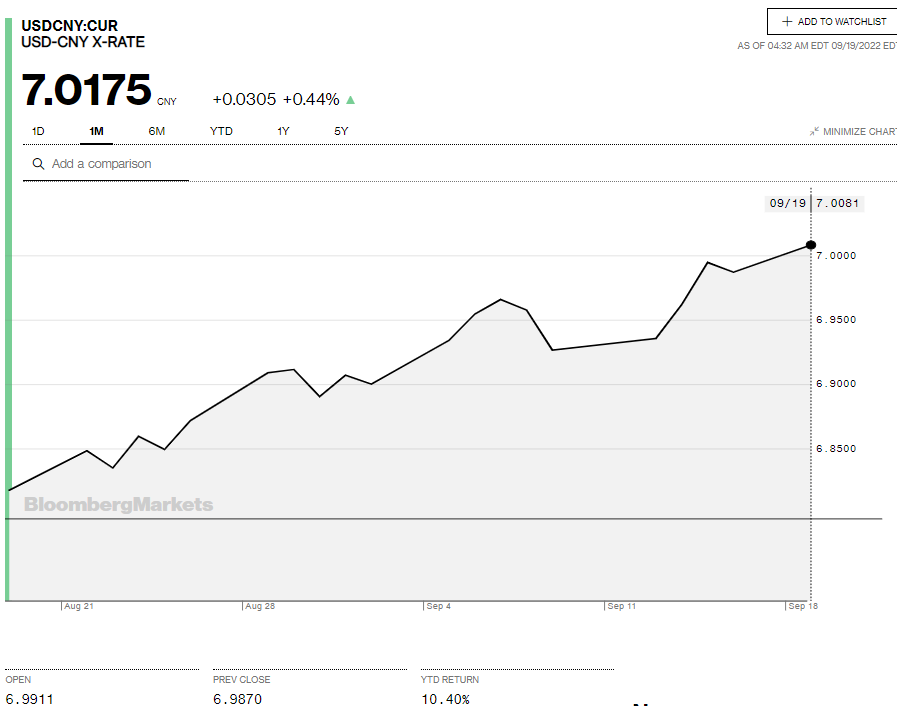

China Snapshot

Today’s Bank of China Fix: 6.9396, previous 6.9305

Shanghai Shenzhen CSI 300 fell 0.12% to 3,928.00

PBoC pushes back against US dollar strength and fixes the rate below expectations, for the 18th consecutive time.

UBS downgrades China 2022 forecast from 3.0% to 2.7%.

China easing some lockdown restrictions.

Chart: USDCNY 1 month

Source: Bloomberg