Source: hdclipartall.com

- Equities awaiting mega-cap earnings reports at end of day

- Weak German Ifo Survey weighs on EURUSD

- US dollar

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3732-36, overnight range 1.3681-1.3746, close 1.3706

USDCAD drifted aimlessly overnight mostly because S&P 500 futures didn’t get traction in any direction. Traders are not motivated ahead of tomorrows Bank of Canada meeting. A 75 bp hike is expected.

At the last policy meeting, Governor Tiff Macklem assured Canadians that driving inflation to its 2.0% target is his priority. It is too soon for him to flip-flop and suggest that enough progress has been made that he can slow the pace of hikes.

WTI oil prices are rangebound in a $83.09-$85.07/b band with gains capped by concerns of a global slowdown while fears of tight supply underpin prices.

The Canadian economic data calendar is empty.

USDCAD Technical outlook

The USDCAD technicals are bullish above 1.3630, looking for a break above 1.3810 to extend gains to 1.3900, then 1.3950. A break of support at 1.3630 targets 1.3500.

For today, USDCAD support is at 1.3660 and 1.3610. Resistance is at 1.3760 and 1.3810. Today’s range: 1.3680-1.3780

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

FX traders were looking for something to fret about and they found in the rapidly falling Chinese yuan. The Peoples Bank of China (PboC) fixed onshore USDCNY at a 14-year peak, a tacit nod to accepting a weaker currency. The news helped underpin the US dollar against the majors in an otherwise subdued overnight session.

Equity traders are hitting the hookah pipe hard and are trying to convince themselves that the Fed will be discussing a “pause” or at least a slower pace of rate hikes at the November 2 meeting. Fed Chair Powell, Deputy Chair Brainard, and NY Fed President John Williams have not suggested anything of the kind in their recent speeches, and they are the “first among equals.”

Asian equity markets closed on a mixed note. Chinese markets were modestly lower while Japan’s Nikkei 225 index finished with a 1.02% gain and the Australian ASX 200 rose 0.28%. European bourses traded in a similar fashion as the German Dax dipped 0.55% and the French CAC rose 0.25%. S&P 500 futures are modestly lower while the US 10-year Treasury yield sits at 4.18%.

EURUSD traded choppily in a 0.9854-0.9898 range as weak German Ifo survey data helped to limit gains. The Survey noted “Sentiment in the German economy continues to be grim. The ifo Business Climate Index dipped to 84.3 points in October, following 84.4 points1 in September. Companies were less satisfied with their current business. Their expectations improved, but they are still worried about the coming months. The German economy is facing a difficult winter.

GBPUSD is rangebound in a 1.1273-1.1339 band ahead of Rishi Sunak’s meeting with King Charles (hmm another new Prime Minister and an elderly monarch-what could go wrong?). Traders are awaiting Sunak’s speech today after he warned of “difficult times ahead,” which is underscored by yesterday’s weak PMI survey data.

USDJPY is choppy in a 148.49-149.09 range. The fear of widening US and Japanese interest rate spreads supports prices while the threat of BoJ intervention limits gains.

AUDUSD traded in a narrow 0.6305-0.6340 band mainly due to US dollar indifference. Treasure Jim Chalmers unveils his budget tomorrow. He is expected to say the economy will slow in 2023 with GDP forecast dropping to 1.5% from the 22.5% guess in April.

US Case-Shiller Home Price Index and Consumer Confidence are due.

Chart: US dollar index and USDCNY weekly

Source Saxo Bank

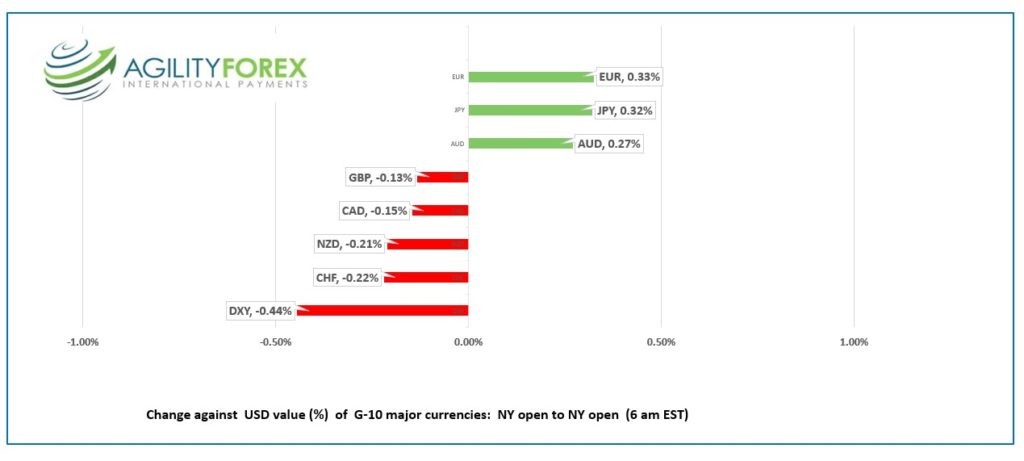

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 7.1668, previous 7.1230

Shanghai Shenzhen CSI 300 fell 0.16% to 3627.45

PboC appears to have given up managing yuan and is letting it mix near the top of its -+2% band. A weak yuan is good for US dollar globally.

Chart: USDCNY 1 month

Source: Saxo Bank