Source: Pixabay

- Canada CPI rises 6.9% y/y as expected

- Errant Ukrainian missile hit Poland, not one from Russia

- US dollar opens mixed compared to Tuesdays NY open

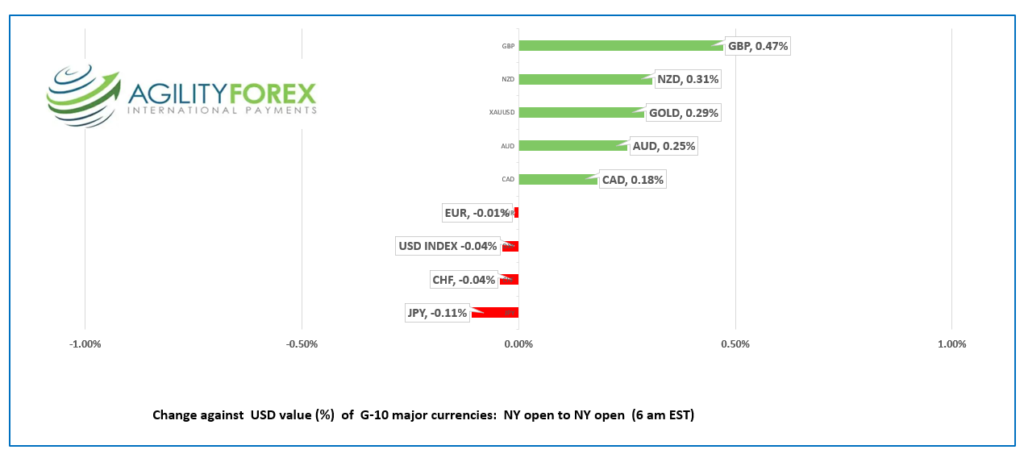

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3248-52, overnight range 1.3230-1.3305, close 1.3280

USDCAD rose in Asia, dropped in Europe, and then inched higher in early NY, all within the confines of yesterday’s 1.3228-1.3335 range. The price action was driven by shift risk perceptions.

The Poland missile crisis (not to be confused with the Cuban missile crisis of October 1962) proved to be a tempest in a teapot and traders have reverted to assessing how economic data will impact Fed monetary policy.

USDCAD didn’t get any action after October CPI rose 6.9% y/y, as expected. The monthly increase of 0.7% was also as estimated, but well-above the 0.1% increase in September. That leaves USDCAD direction at the whim of broad US dollar sentiment.

WTI oil prices traded sideways in a $85.86/b-$87.48/b range with gains from a weaker US dollar offset by fears of slowing demand.

USDCAD Technical outlook

The USDCAD technicals are trading with a bearish bias in a 1.3200-1.3400 range. A topside break targets 1.3560 while a break below 1.3200 puts 1.3000 in play.

For today, USDCAD support is at 1.3230 and 1.3170. Resistance is at 1.3310 and 1.3360.

Today’s range 1.3170-1.3270

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Global risk sentiment rebounds after WW lll is averted. US President Joe Biden claimed that the missile that landed in Poland and killed two people was not fired from Russia, but from Ukraine. The news sorely disappointed Ukraine President Volodymyr Zelenskiy who wanted to drag NATO into the Russia/Ukraine war.

And speaking of wars, Donald Trump formally announced his 2024 presidential run yesterday, surprising no one, as he has been informally announcing his plans ever since he didn’t lose the 2018 election. The circus is back in town.

Yesterday’s FX market chaos has evolved into a broad-based orderly US dollar retreat with traders focus shifting back to hopes for a slower pace of Fed rate hikes after Tuesday’s weaker than expected PPI report showed evidenced inflation pressures are easing.

Wall Street rallied, sank, then rallied into the close on Tuesday as traders digested cooling inflation data and burning geopolitical tensions. Asian markets closed mixed. Australia’s ASX 200 lost 0.27% while Japan’s Nikkei 225 index gained a meagre 0.14%.

European equity traders are far more cautious and trading in negative territory, except for the UK FTSE 100 which is 0.17% higher. S&P 500 futures are modestly higher gaining 0.10%, and gold and oil prices are firmer.

The US 10-year Treasury yield is trading at 3.792% after an overnight range of 3.758%—3.837%.

The “Fed-to-slow-rate-hike-pace” narrative got a bit of boost from Kansas City Fed President Ester George. She said it would make sense to slow the pace of rate hikes next year to a more traditional 25 bps. However, she also said it was very premature to be looking ahead to when the Fed stops hiking proving you can suck and blow at the same time.

US Retail Sales and Retail Sales ex-autos rose 1.3% m/m in October beating expectations and giving the Fed more ammunition to keep hiking interest rates.

EURUSD climbed steadily overnight, rising from 1.0332 to 1.0438, but remains below the post-PPI peak of 1.0481.

Bank of Italy Governor and ECB board member Ignazio Visco said, “The need to continue with restrictive policy is evident, although reasons to follow a less aggressive approach are gaining ground.” The suggestion of more timid ECB rate increases combined with caution around the Russia and Ukraine war may limit EURUSD gains. However, the short term technicals are bullish above 1.0300 and looking for a break above 1.0500.

GBPUSD traded with a bullish bias in a 1.1834-1.1940 range overnight, failing to regain yesterday’s post-PPI peak of 1.2028. UK inflation was a scorching 11.1% y/y in October (forecast 10.7%, September 10.1%), a 41-year peak. It would have bee 18.8% if the Liz Truss government did not introduce an energy price cap.

USDJPY traded in a 138.74-140.28 range and is trading at 139.50 in NY. Price action continues to be dictated by broad risk sentiment and US Treasury yields.

AUDUSD traded in a 0.6732-0.6792 range due to improved risk sentiment. Australian wage inflation rose 3.1% but was not much of a factor for markets.

NZDUSD traded in a 0.6133-0.6192 range. Prices are supported by expectations that the RBNZ will raise rates by 75 bps on November 23.

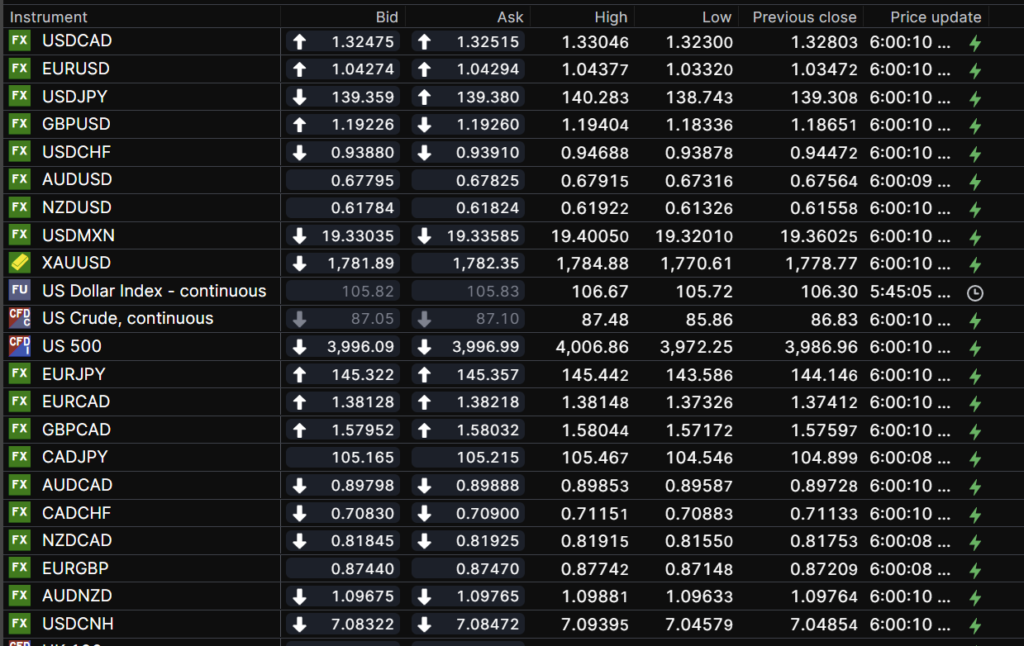

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

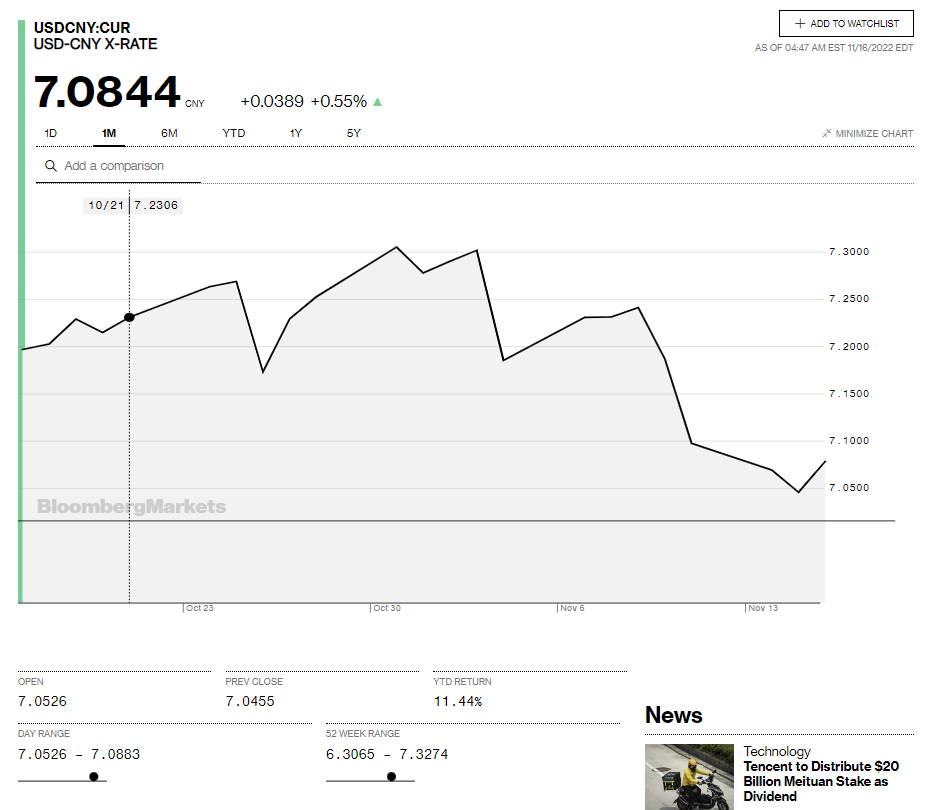

China Snapshot

Today’s Bank of China Fix: 7.0363, previous 7.0421

Shanghai Shenzhen CSI 300 fell 0.82% to 3834.39

PboC Governor YI and US Treasury Secretary Yellen had “constructive and candid” talks.

China’s state planner said growth stabilization policies would begin in Q4.

Chart: USDCNY 1 month

Source: Bloomberg