Source: wikimediacommons

- Powell speech headlines big data dump

- Eurozone inflation falls more than expected

- US dollar opens higher compared to Tuesday, but retreats from closing levels

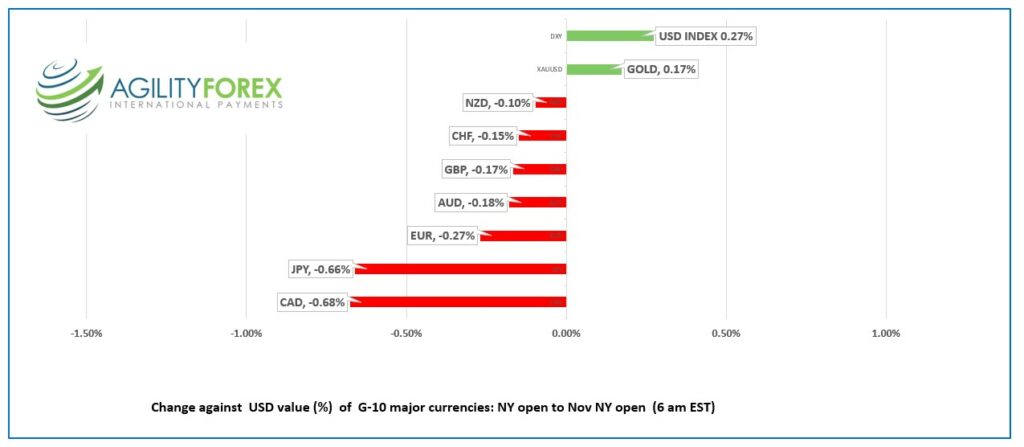

FX at a glance:

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3544-48, overnight range 1.3498-1.3592, close 1.3579

It is rare to see USDCAD moving while the other G-10 currencies are somewhat somnolent, but it happened yesterday. USDCAD rallied from the opening bell and rose from 1.3411 to 1.3644 by lunch hour.

Coincidently, RBC announced an agreement to purchase HSBC Canada for $13.5 billion, all in cash.

The deal is expected to close “late in 2023.”

Regardless of the closing date, HSBC ‘s parent company is British. If management thinks it’s a great idea to bail out of Canada, they are unlikely to want to hold Canadian dollars, which explains yesterday’s USDCAD rally. They certainly did not unload the entire amount, but they more than likely trimmed a billion or two. (rule of thumb-one big figure for every billion dollars)

The RBC news overshadowed Canada’s better than expected Q3 GDP growth which rose 0.7% q/q compared to expectations for a 0.4% q/q gain. BMO economists argue that upward historical revisions suggest the economy is larger than previously thought, paving the way for a 50 bp rate hike on December 7.

But that was yesterday. Today, everything is about what tone Fed Chair Powell will adopt with his speech to the Brookings Institution at 10:30 am PT today. Bet on “slow and steady wins the race.”

WTI oil prices continue to consolidate losses after falling below support at $82.50/barrel on November 17. Prices climbed from a low in Asia of $78.43 to $80.96 in NY today. Opec has opted for a “virtual meeting” this weekend which means no change in policy, according to analysts.

USDCAD Technical outlook

The intraday USDCAD technicals are bullish above 1.3450 and looking for a break above resistance in the 1.3590-1.3600 area for a test of downtrend line resistance at 1.3680 (daily chart). A break below 1.3505 will target 1.3430.

Longer term the uptrend line from June 2022 is intact above 1.3090.

For today, USDCAD support is at 1.3490 and 1.3440. Resistance is at 1.3570 and 1.3610

Today’s range 1.3470-1.3570

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Global market attention has shifted from Opec and China’s covid issues to Fed Chair Jerome Powell’s 10:30 pm PT speech. Consequently, trading was subdued overnight.

Asian equity markets closed mixed; Australia’s ASX 200 rose 0.43% while Japan’s Nikkei 225 index fell 0.21%. European bourses are all in the green led by a 0.54% rise in the UK FTSE 100. S&P 500 futures have squeezed out a 0.07% gain. Gold (XAUSUD) climbed to $1764.61 from the NY close of $1749.80 but dipped following the ADP employment data.

ADP reported employers added 127,000 jobs in November, the slowest pace since January 2021. ADP Chief Economist Nela Richardson said “Turning points can be hard to capture in the labor market, but our data suggest that Federal Reserve tightening is having an impact on job creation and pay gains. In addition, companies are no longer in hyper-replacement mode. Fewer people are quitting and the post-pandemic recovery is stabilizing.”

So, what will Powell say? You will recall that in his post-FOMC press conference on November 2, Mr Powell rejected claims that the Fed was dovish. He said that “The question of when to moderate the pace of increases is much less important than the question of how high, and how long to keep monetary policy restrictive. He added it was “very premature to discuss when the Fed would pause rate hikes.

Arguably he won’t be changing his message today which suggests US dollar demand and lower stock prices

EURUSD is trading in a 1.0320-1.0381 range, supported by Eurozone November inflation (actual 10% y/y, forecast 10.4%, October 10.6%) data. Gains may be limited due to suggestions that the results mean the ECB will only hike 50bps at the December meeting.

GBPUSD dropped to the middle of its 1.1943-1.2028 range following the ADP data. Prices are supported by comments from Bank of England Chief Economist Huw Pill suggesting UK rates need to go higher, but gains were tempered when he said rates will finish lower than financial markets expect.

USDJPY traded is at the top of its 138.34-139.33 range following the ADP data and a rise in the US 10-year Treasury yield to 3.77% from 3.74%.

AUDUSD got a boost from improved China reopening hopes and climbed to 0.6740 from 0.6672.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

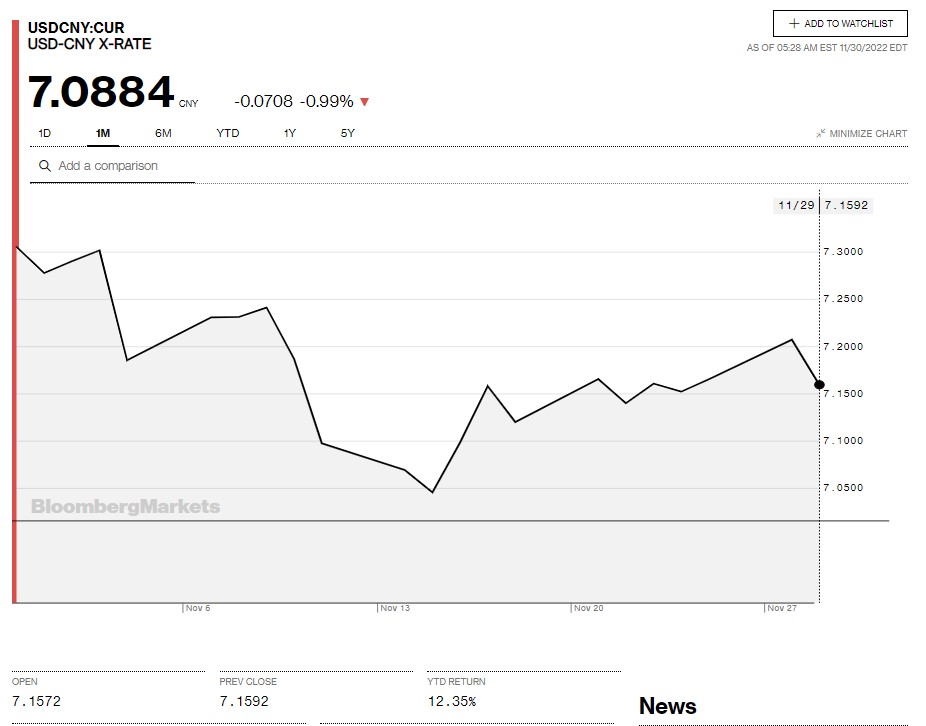

China Snapshot

Today’s Bank of China Fix: 7.1769, previous 7.1989

Shanghai Shenzhen CSI 300 rose 0.12% to 3853.04

NBS November Manufacturing PMI 48 (forecast 49, October 49.2)

NBS Non-Manufacturing PMI 46.7 (forecast 51.7, October 48.7)

China activity slowed by Covid-19 outbreak

Chart: USDCNY 1 month

Source: Bloomberg