Source: wikimediacommons

- Powell speech deemed dovish

- Eurozone data dump, mixed to soft

- US dollar extends Wednesday losses overnight CAD underperforms

FX at a glance:

Source: IFXA Ltd/RP

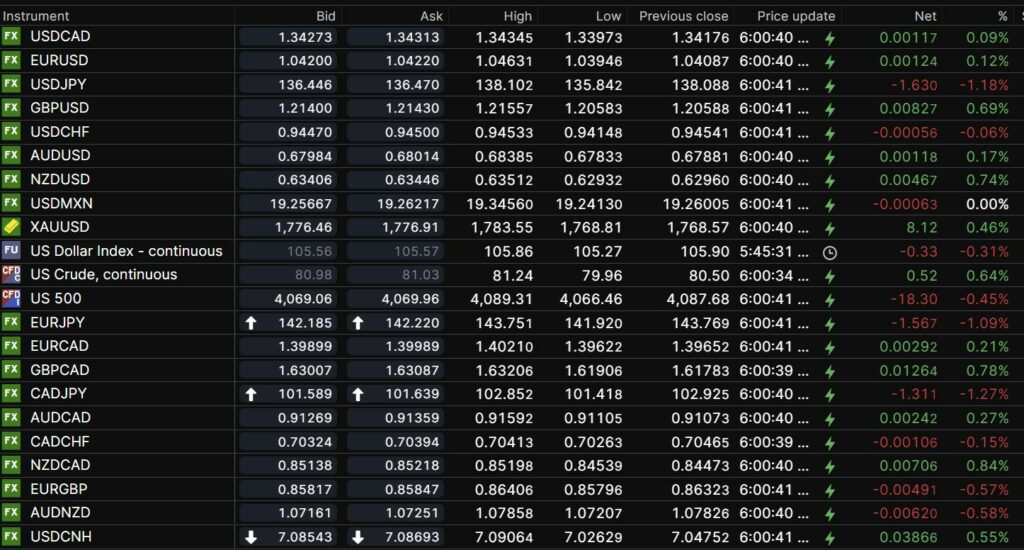

USDCAD Snapshot: open 1.3427-31, overnight range 1.3397-1.3435, close 1.3418

USDCAD dropped on the back of widespread US dollar weakness following Fed Chair Powell’s speech yesterday. Prices dropped from 1.3572 to 1.3414 but quickly ran out of gas.

The Fed plans to slow the pace of rate hikes to 50 bps in December, partly because the impact of this years 350 bp rate increase is starting to be reflected in weaker economic data. The same holds true for the Bank of Canada hikes and the impact on domestic data.

The moves raise the risk of recessions in both countries and if so, investors would prefer US dollars over Canadian. The BoC’s view on recession risks will become clearer after the December 7 monetary policy meeting.

WTI oil climbed from $79.96/b to $81.68 overnight due to the sharp drop in US crude inventories. EIA reported that US inventories fell 12.58 million barrels in the week ending November 25. The rally got a further boost from speculation that China will speed up its reopening pace.

USDCAD direction remains at the mercy of broad US dollar sentiment as measured by S%P 500 moves.

There are no top tier Canadian economic reports today.

USDCAD Technical outlook

The intraday USDCAD technicals are bearish below 1.3510, looking for a break of 1.3390 to test the November uptrend line at 1.3360. If decisively broken, it sets the stage for further losses to 1.3210-20 area, which has contained downside moves since September 16.

Longer term the uptrend line from June 2022 is intact above 1.3090.

For today, USDCAD support is at 1.3390 and 1.3360. Resistance is at 1.3450 and 1.3510

Today’s range 1.3390-1.3490

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Fed Chair Powell’s highly anticipated speech to the Brookings Institution was deemed to be dovish.

The reaction is a bit of a head-scratcher as Mr Powell essentially repeated his remarks from the November 2 post-FOMC meeting press conference.

At that time, his comments were considered hawkish. He said “At some point—as I’ve said in the last two press conferences—it will become appropriate to slow the pace of increases as we approach the level of interest rates that will be sufficiently restrictive to bring inflation down to our 2 percent goal.

The US dollar soared, equities sewered, and the 10-year US Treasury yield popped to 4.09% from 4.00%.

Yesterday, Mr Powell said, “The time for moderating the pace of rate increases may come as soon as the December meeting.” Wall Street stocks and commodities soared while the US dollar and the 10-year Treasury yield fell.

You could just about picture the munchkins from the Wizard of Oz dancing in a circle and singing “ding dong, inflation is dead.”

Semantics aside, traders are only hearing what they want to hear and ignoring increasing recession warnings from weaker than expected data. Wednesday, Pending home sales, Chicago PMI index and the ADP employment reports were sharply lower than expected.

Risk sentiment got another positive boost from Covid developments in China. Recent lockdown restrictions were lifted in Guangzhou, despite rising covid cases and Vice Premier Sun Chunlan said covid fighting efforts entering new phase.

Asia equity markets closed higher with Japan’s Nikkei 225 index gaining 0.92% and Australia’s ASX 200 index rising 0.96%. European bourses are trading higher, but they are not as perky as those in Asia. The German Dax is leading the rally, but it is only up 0.50%.

S&P 500 futures flipped from a loss to a 0.19% gain following the early US data. Weekly jobless claims rose 225,000, 16,000 lower than the previous week while Personal Consumption Expenditures were a tad lower than expected.

EURUSD rallied from 1.0291 to 1.0428 yesterday then extended those gains to 1.0463 before dropping to a short-lived visit at 1.0395 following weaker than expected data. German October Retail Sales fell 2.8% m/m. Manufacturing PMI reports for Germany and the Eurozone were a tad softer than expected and both are in contraction territory. The intraday EURUSD technicals are bullish above 1.0330.

GBPUSD popped following Powell’s speech, rising from 1.1920 yesterday to 1.2156 in NY trading today. Prices got a modicum of support from better-than-expected Markit Manufacturing PMI (actual 46.5 vs forecast 46.2). The Fed’s plans to slow the pace of rate hikes narrowed the 10-year Gilt and 10-year Treasury yield spread is also underpinning prices. The break above 1.1990 targets 1.2250.

USDJPY plunged from 139.84 yesterday morning to 135.84 in Asia, before climbing to 136.22 in NY. Japan’s Manufacturing PMI dipped to 49 from 49.4 in October.

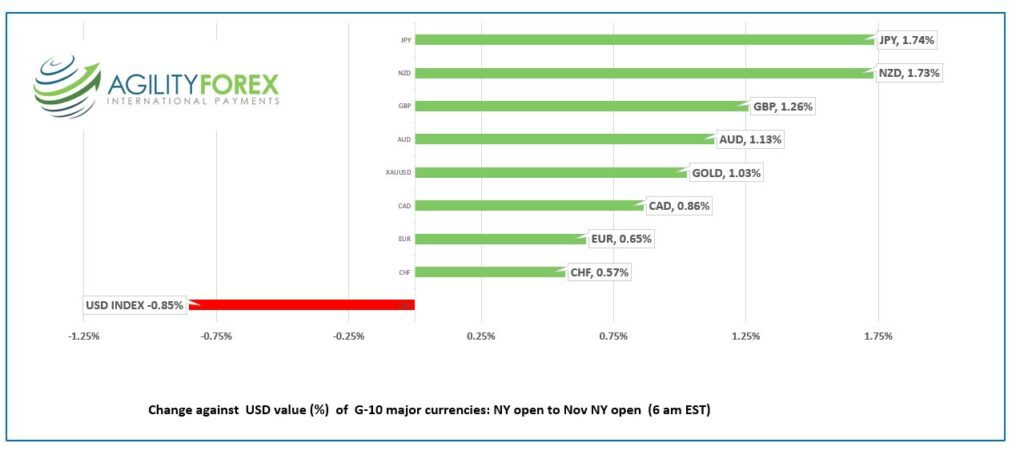

The antipodean currencies got a double boost. The first from broad US dollar weakness after Powell’s speech and the second from reports China is easing covid restrictions. AUDUSD rallied from 0.6676 Wednesday to 0.6839 in Europe, before slipping to 0.6803 in NY. NZD nearly tied with JPY as best performing G-10 currency since Wednesday’s NY open, gaining 1.73%

Today’s data includes weekly jobless claims (forecast 235,000), Core Personal consumption Expenditures Price index and ISM Manufacturing PMI.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

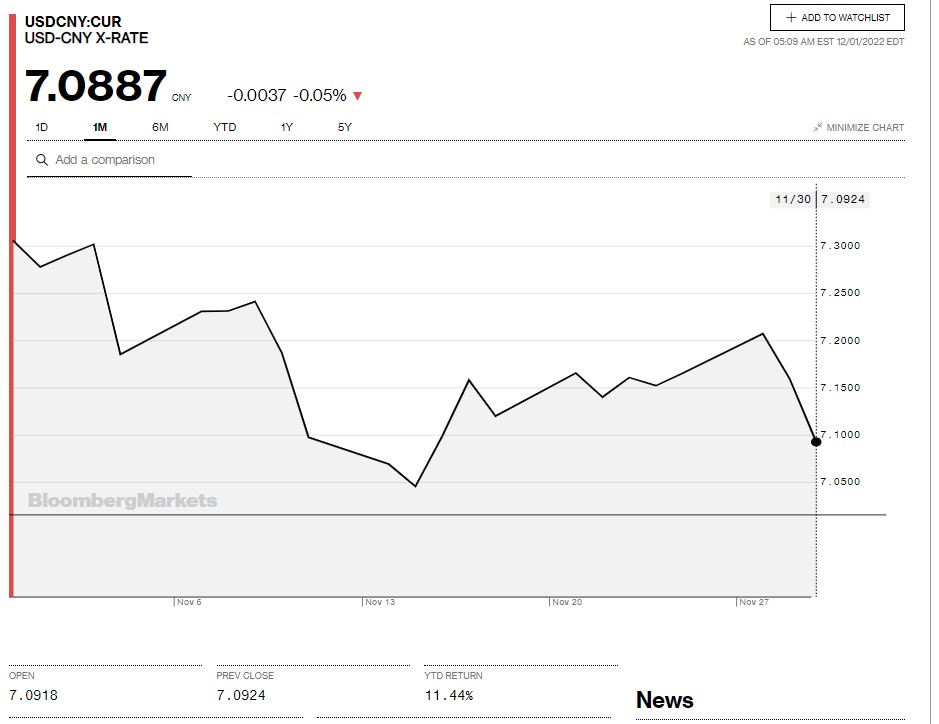

Today’s Bank of China Fix: 7.1225, previous 7.1769

Shanghai Shenzhen CSI 300 rose 1.08% to 3894.77

Caixin Manufacturing PMI 49.4 vs forecast 48.4 and 49.2 in October

Covid protests paying dividends. Guangzhou, the third largest city in China lifted lockdowns in several areas, despite covid cases rising there. Vice Premier Sun Chunlan said covid fighting efforts entering new phase as omicron weakens and more people are vaccinated.

Chart: USDCNY 1 month

Source: Bloomberg