Photo: hddclipartall.com

- Canada Headline inflation dips to 6.8% from 6.9% y/y

- Global stock indexes inch higher, US 10-year Treasury yield steady at 3.69%

- US dollar opens lower, consolidating Tuesday’s losses

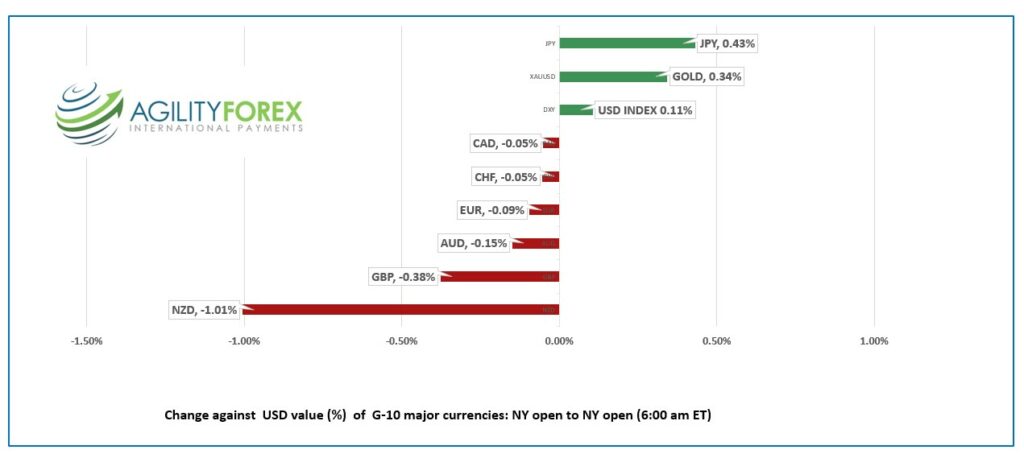

FX at a glance:

Source: IFXA Ltd/RP

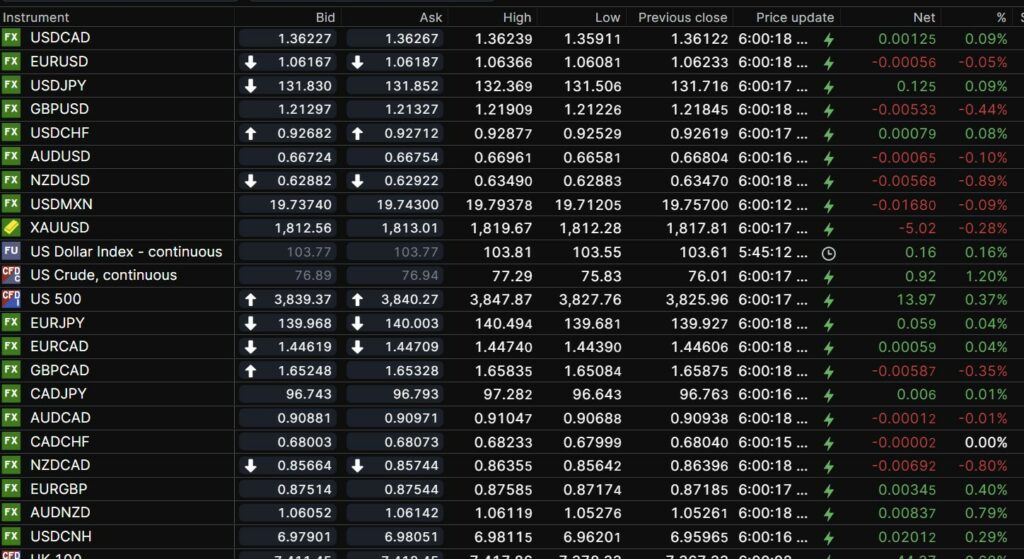

USDCAD Snapshot: open 1.3623-28, overnight range 1.3591-1.3624, close 1.3612

Statistics Canada reported CPI rose 6.8% y/y in November, a tick lower than Octobers 6.9% y/y reading but above the 6.7% y/y forecast. Excluding Food and energy, CPI rose 5.4%, just above the 5.3% y/y result in October.

USDCAD was adrift in a quiet overnight market with little news or economic data to draw traders away from the bar.

Canada Retail Sales rose 1.4% m/m in October and the ex-autos component gained 1.7% m/m. The results are not a positive as they look. The increases came from higher prices, especially at the gas pump. Stats Canada’s preliminary November estimate is for a 0.5% decline.

USDCAD was undermined by a rising WTI prices which have climbed from $73.85/barrel on Monday to $77.29/b just before NY opened today. The 4.6% gain is partly due to API reporting crude inventories fell 3.06 million barrels last week which was lower than expected.

The G-7 oil sanctions on Russia are filling Xi Jinping’s wallet as he thumbs his nose at the US. China increased imports of heavily discounted Russian crude by 17% in November. Excluding Food and Energy, CPI rose 5.4%, which is a tick above the 5.3% result in October.

USDCAD technical outlook.

USDCAD is chopping about in a 1.3500-1.3700 range which has contained price action since December 6. Today’s Canadian CPI data is unlikely to change that.

The intraday technicals are bullish above 1.3580, looking for a break above 1.3650 to extend gains to 1.3700. A move below 1.3580 targets 1.3540 then 1.3510.

For today, USDCAD support is at 1.3580 and 1.3540. Resistance is at 1.3560 and 1.3710

Today’s range 1.3580-1.3660

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The market holiday season officially kicked off December 15, following the FOMC meeting. Books are closing and bottles are uncorking as traders celebrate or drown their sorrows, mostly the latter.

Some Asian equity indexes managed to stop the bleeding following Tuesday’s BoJ induces trauma. Japan’s Nikkei 225 was not one of them. It closed down 0.68%. Down under, Australia’s ASX 200 gained 1.29%.

European bourses are all posted gains in a low volume session. The German Dax has climbed 0.95% while the French CAC index rose 1.26%. S&P 500 futures rose 0.65% as of 5:42 am PT.

Gold prices have risen by $1.75 cents since Tuesday’s close. The US 10-year Treasury yield flitted about in a 3.677-3.722% range and is at 3.681% in early NY.

EURUSD traded in a 1.0608-1.0637 range. German Consumer Confidence improved for the third time in a row, but it still remains weak and is vulnerable to another energy price shock. EURUSD is in a downtrend below 1.0730 with a break below 1.0600 targeting 1.0500.

GBPUSD is trading poorly, falling from 1.2191 to 1.2088 in NY. The currency is suffering from a fresh focus on the government borrowing a record £22.0 billion in November mainly due to fund energy price support. The currency is also suffering from concerns about the economic impact of a wave of worker strikes.

USDJPY is consolidating yesterday’s losses in a 131.51-132.37 range. The BoJ’s surprise increase of the 10-year JGB yield band has increased speculation of further hawkish monetary policies ahead.

AUDUSD traded quietly in a 0.6658-0.6713 range with peak seen in NY. NZDUSD traded in a 0.6288 0.6349 range undermined by weaker than expected Consumer Confidence and November trade data.

US Consumer Confidence and Existing Home Sales data reports are ahead.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

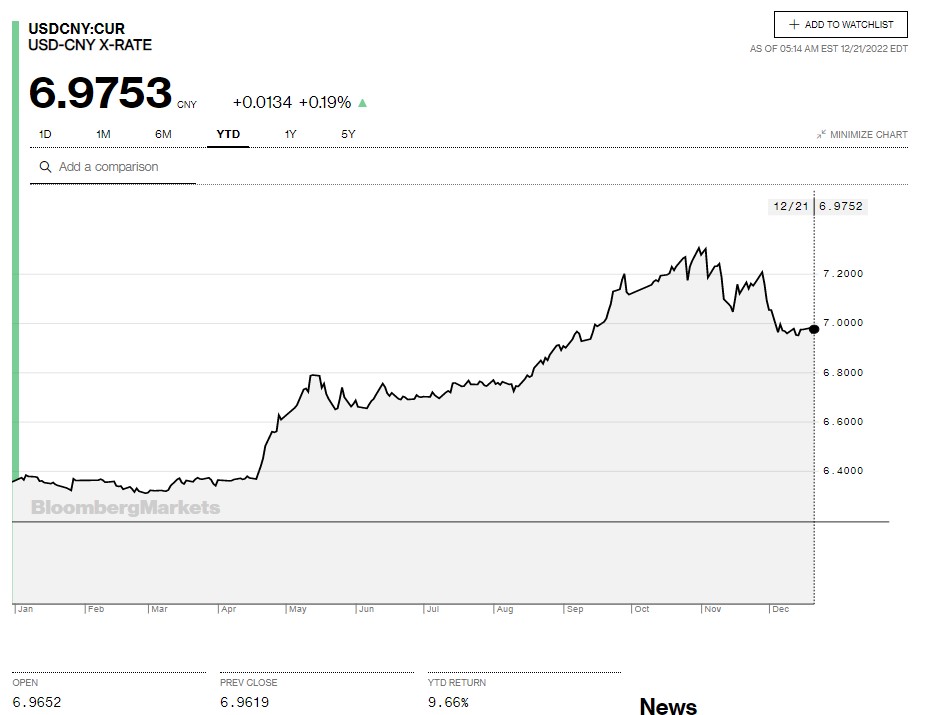

China Snapshot

Today’s Bank of China Fix: 6.9650, previous 6.9861

Shanghai Shenzhen CSI 300 rose 0.04% to 3830.54

Chart: USDCNY year-to-date

Source: Bloomberg