Photo: MGM entertainment

January 13, 2023

- US 10-year Treasury yield at 3.448%, down from 3.591% yesterday

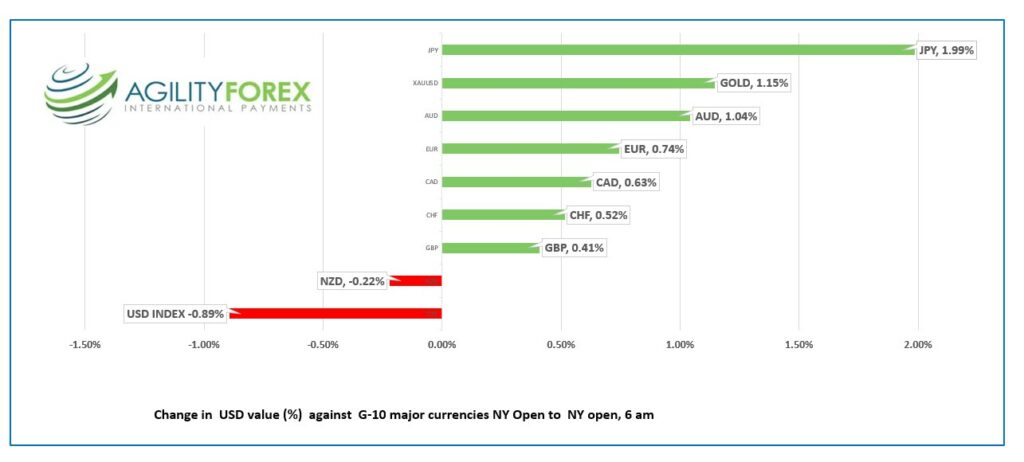

- USDJPY plunge driving greenback lower

- US dollar getting spanked, JPY outperforms

FX at a glance

Source: IFXA Ltd/RP

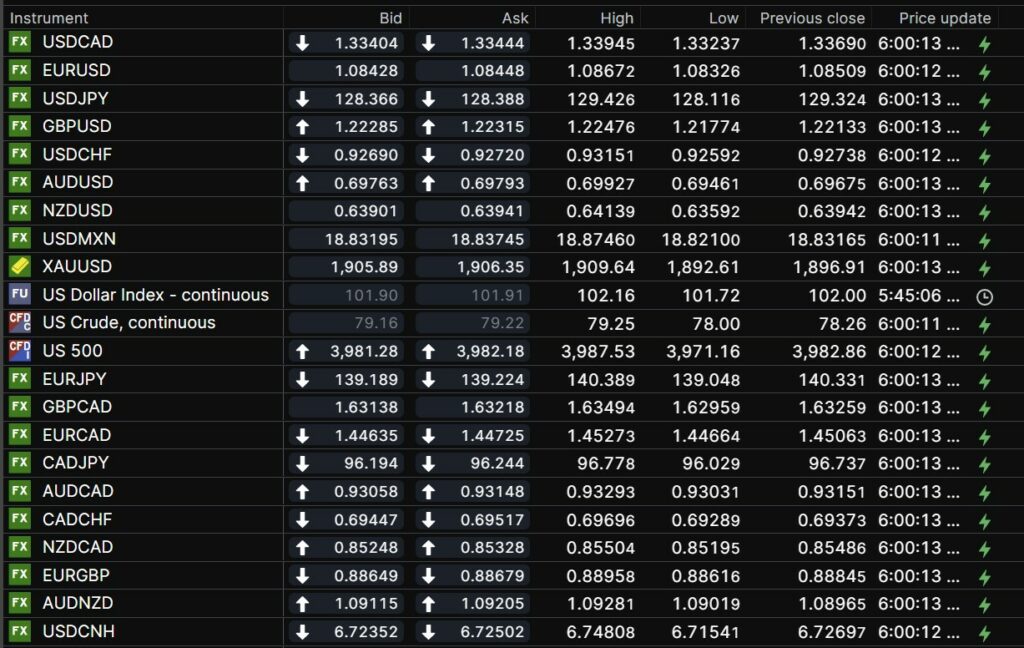

USDCAD Snapshot: open 1.3340-44, overnight range 1.3324-1.3395, close 1.3369

USDCAD is riding the bearish greenback wave but is hitting a lot of support before the June uptrend line comes into play.

USDCAD is riding the bearish greenback wave but is hitting a lot of support before the June uptrend line comes into play.

The USDCAD pressure extends from external factors, particularly, the downgrading of US rate hike expectations. The bond market is in open revolt against the Feds outlook and have driven the US 10-year Treasury yield down from 3.805% on January 3, to 3.448%. The bond traders are reacting to a couple of data points suggesting inflation is receding despite the FOMC projections of rates above 5.0% for all of 2023.

Oil prices ticked higher on the back of broad US dollar weakness. WTI traded in a $78.00-$79.25% overnight on hopes for sharply higher Chinese demand and lower Opec supply, while dismissing last week’s steep rise in US crude inventories.

USDCAD will react to S&P 500 price action which may be volatile with major banks reporting earnings including JPMorgan Chase, and Wells Fargo.

There are no Canadian economic reports today.

USDCAD technical outlook.

The intraday USDCAD technical are bearish below 1.3440, looking for a decisive break below 1.3340 to extend losses to the June 2022 uptrend line at 1.3270. A break below 1.3270 will extend losses to 1.3230 and target 61.8% Fibonacci retracement level support of the June-October range, at 1.3060. A break above 1.3450 would negate the short-term downtrend pressure and shift the focus to 1.3530.

For today, USDCAD support is at 1.3340 and 1.3310. Resistance is at 1.3440 and 1.3480.

Today’s range 1.3340-1.3420

Chart: USDCAD weekly

Source: Saxo Bank

G-10 FX recap and outlook

“Ladies and Gentlemen, welcome to the “Battle of the Brains.” In the left corner, the current champion, the smug, all-knowing, and mostly geriatric, FOMC. In the right corner, Wall Street, a disrespectful, not-yet-elderly Millennial/Gen-Z mix. Who will win the fed funds prize?

The FOMC believe they are the Masters of the Universe, the all-knowing stewards of US monetary policy and that US rates will rise to 5.25% in 2023 and remain unchanged for the entire year.

The challenger, Wall Street believes the Fed has lost its touch and is reality-challenged, pointing to a string of failures in 2022.

The fight has begun, and the Fed has been rocked by a series of headshots by the challenger. The latest in the form of an as expected CPI reading, was a more akin to a “bitch-slap” than a knock-out punch.

Nevertheless, the December CPI data (headline 6.5% and Core 5.7% y/y) were exactly as forecast.

Richmond Fed President Thomas Barkin said the Fed could be less aggressive, but believed the interest rate path was “slower, longer, and potentially higher.”

St Louis Fed President James Bullard is firmly in the rate hike camp and wants fed funds above 5.0% “expeditiously.”

Bond traders clearly don’t believe the Fed.

Asia equity markets closed with gains except Japan’s Nikkei 225 index which lost 1.25% due to a weaker USDJPY. European bourses are modestly higher while S&P 500 futures have dropped 0.31%.EURUSD consolidated yesterdays gains in a 1.0809-1.0867 range and is trading at the low end of that band in NY. The sell-off is mainly due to profit-taking ahead of the weekend. The German Economy Minister predicted the economic slowdown in the winter will be milder than expected. His comment was supported by news that Euro area Industrial Production rose 1.0% m/m in November. EURUSD technicals are bullish above 1.0760.

GBPUSD rallied in the early morning in Europe then erased the entire move as NY opened, falling from 1.2248 to 1.2172. UK GDP rose 1.0% m/m in November (forecast -0.1% m/m) raising hopes that the country will avoid a recession. Capital Markets Senior Economist Ruth Gregory said “If GDP avoids a monthly fall of more than 0.4% in December, then it won’t contract in 4Q as a whole and thus it will have avoided a technical recession in 2022, Gregory says. However, a recession is still likely in 1H 2023, she says. “It is too soon to conclude the economy will be able to get through this period of high interest rates and high inflation largely unscathed.”

USDJPY dropped to 128.11 from 129.43 and is down 3.3% since last Friday. Markets are anticipating more hawkish tweaks to monetary policy when the BoJ meets next week. The perception of higher Japanese rates as US rates peak, then drop is driving USDJPY losses.

AUDUSD traded in a 0.6946-0.6993 range with softer US 10-year Treasury yields, and the improved outlook for China’s economy underpinning prices.

Today’s US data includes Michigan Consumer Sentiment, expected to rise to 60.5 in January from 59.7 in December.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

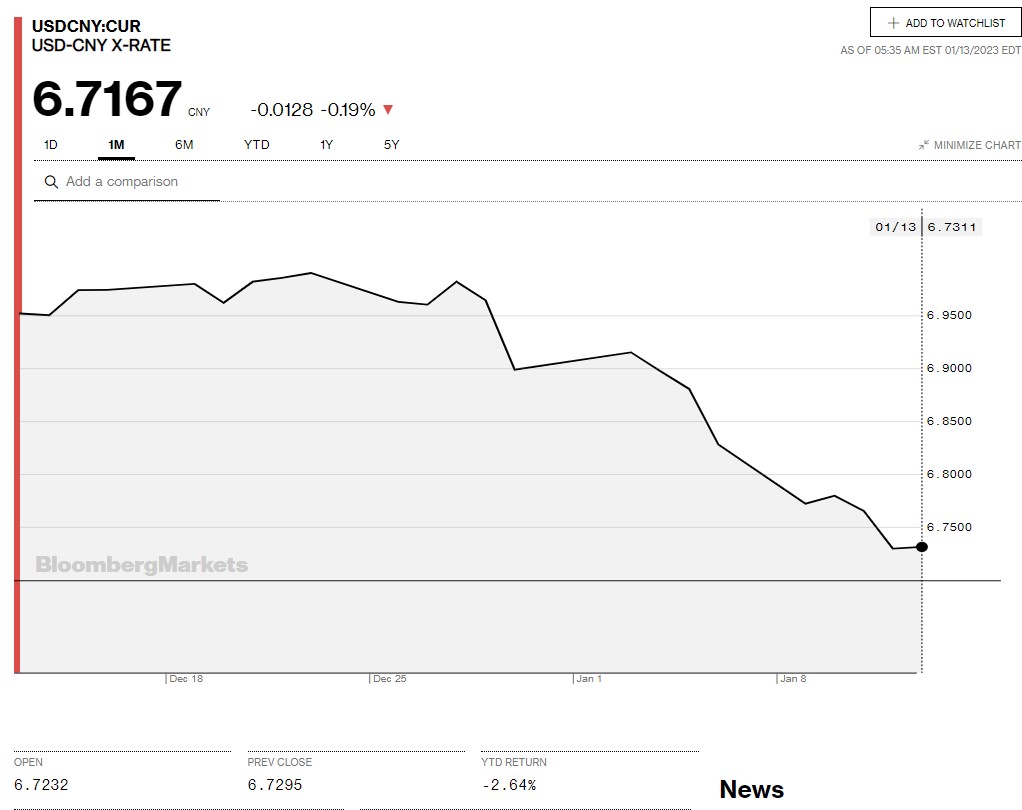

China Snapshot

Today’s Bank of China Fix: 6.7292, previous 6.7680

Shanghai Shenzhen CSI 300 rose 1.41% to 4074.38

China Trade surplus widens to $78 billion from $69.84 bn in November.

PboC Governor promises “appropriate monetary policy” and no “flood-like” stimulus while planning to “effectively resolve risks of quality property developers.

Chart: USDCNY one month

Source: Bloomberg