Photo: Flickr

January 17, 2023

- Canada Core CPI falls to 5.4% y/y

- Risk mood turns negative on rising Treasury yields and soft China data

- US dollar opens mixed from Monday.

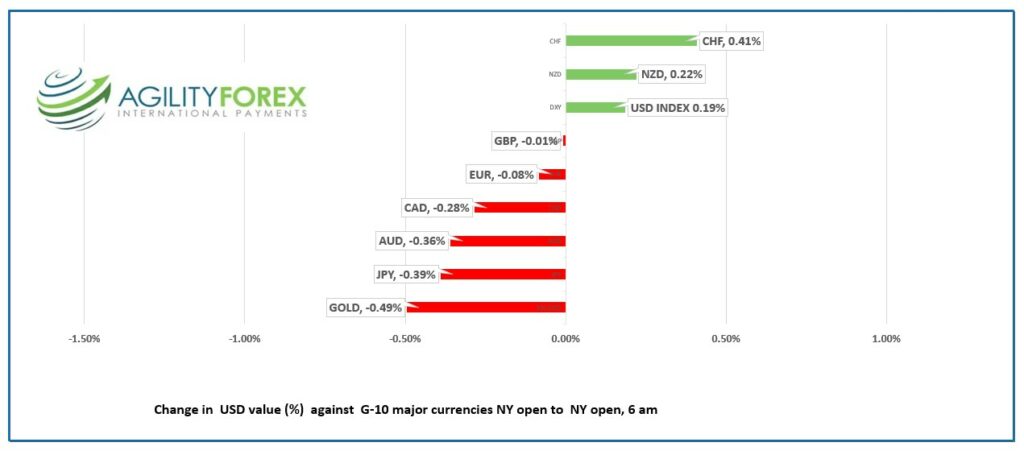

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3422-26, overnight range 1.3396-1.3435, close 1.3407

USDCAD hic-cupped when the inflation report was released but then prices returned to pre-data levels.

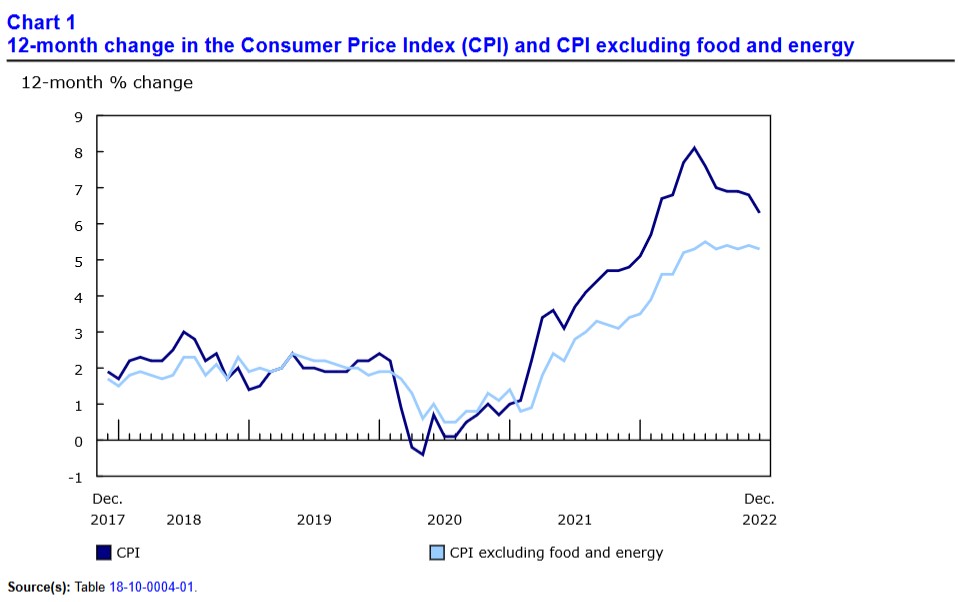

Canada headline CPI rose 6.3% y/y in December, as expected but below Novembers 6.8% y/y result. Core-CPI was the surprise. It only rose 5.4% compared to forecasts for a 6.1% y/y increase. The majority of the declines was due to lower oil prices.

Source: Statistics Canada

WTI oil traded in a $78.57/b-$80.39/b range overnight and it is helping limit USDCAD gains. Goldman Sachs analysts reiterated their call that western economies will avoid a recession, China’s oil demand will improve and Russian supply will sink, which combined will boost crude prices.

USDCAD Technical Outlook

The intraday USDCAD technicals are mildly bullish above 1.3380, looking for a break above 1.3450 to extend gains to 1.3520. A move below 1.3380 targets 1.3340, which if decisively broken sets the stage for further losses to 1.3270.

For today, USDCAD support is at 1.3370 and 1.3330. Resistance is at 1.3440 and 1.3480.

Today’s range 1.3340-1.3440

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

Traders were looking for guidance when Asia opened due to a lack of direction from closed US markets. They found it in Chinese GDP, Industrial Production, and Retail Sales reports. They were not happy. The initial reaction was to sell stocks and buy dollars, but that sentiment is fading as the news was not unexpected thanks to Xi Jinping’s zero-covid policy.

China Q4 GDP rose 2.9% y/y which beat the 1.8% forecast but well below earlier estimates Retail Sales and Industrial production were weaker than the previous result, but still better than expected. The data is also stale and just noise.

The annual bun-fest in Davos has begun and the volume of hot-air from a host of speakers will have bigger impact on global warming than a fleet of 1970’s era 747’s.

Asian equity indexes closed largely unchanged except for Japan’s Nikkei 225 index which rallied on the back of the weaker yen and ahead of tomorrow’s BoJ decision.

European bourses are modestly lower with the German Dax index down 0.21% and the UK FTSE 100 down 0.16%. S&P 500 futures are also in negative territory, down 0.24% as of 6:05 am PT.

EURUSD traded in a 1.0807-1.0838 range overnight despite hawkish comments from ECB officials advocating higher rates. European Union President Ursula von der Leyen is dumping on China for heavily subsidizing clean-technology at the expense of European Union countries. German inflation data was as 8.6% y/y in December, as expected. The German ZEW Indicator of Economic Sentiment jumped 40.2 points to 16.9, taking it into positive territory for the first time since February 2022. EURUSD technicals are bullish and looking for a test of 1.0960.

GBPUSD is at the top of its 1.2171-1.2258 range with prices supported by UK employment data which showed a steady unemployment rate (actual 3.7% vs expectations and prior reading of 3.7%, 3m November) and higher wage earnings. The results leave a 50 bps BoE rate hike in play in February. The intraday GBPUSD technicals are bullish above 1.2150, looking for a move top 1.2320.

USDJPY rallied from 128.22 to 129.15 before prices slipped to 128.78 in NY. The rise in the US 10-year Treasury yield from 3.49% to 3.553% is underpinning prices while the risk of a hawkish result from tomorrows BoJ meeting limits gains.

AUDUSD traded defensively in a 0.6931-0.6977 range due to broad US dollar gains with losses limited by better-than-expected Westpac Consumer Confidence data (actual 5.0% vs 3.0% in December).

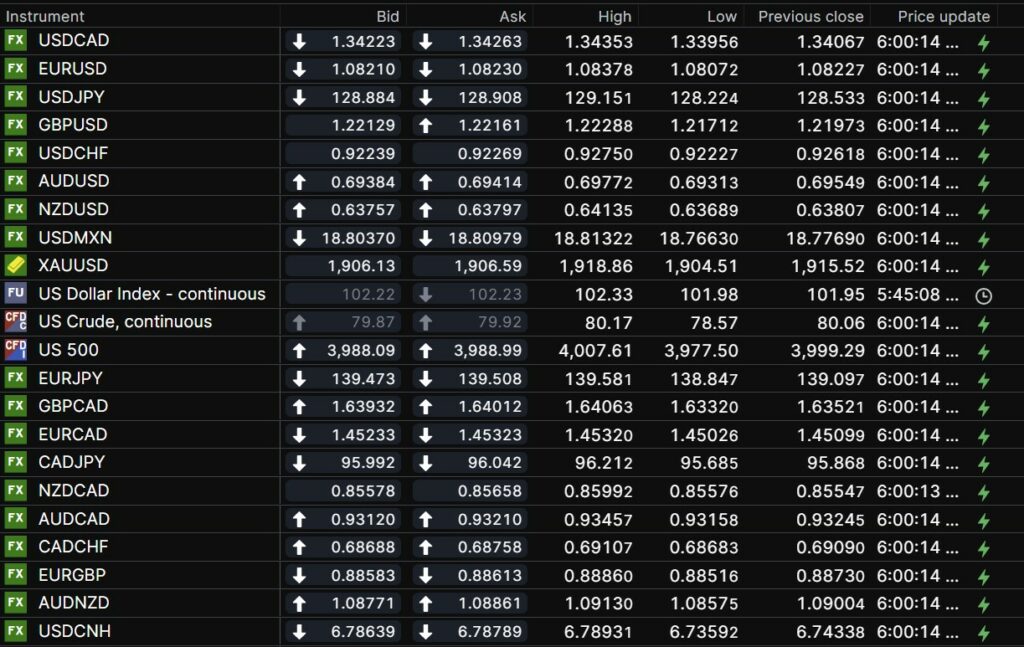

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

China Snapshot

Today’s Bank of China Fix: 6.7234, previous 6.7135

Shanghai Shenzhen CSI 300 rose 1.56% to 4137.96

December Q4 GDP 2.9% y/y (forecast 1.8%, previous 3.9%) was the second slowest pace since the 70’s, which is no surprise do to Xi Jinping’s zero-covid policy.

December Retail Sales fell 1.8% y/y (forecast -7.8%, previous -5.9%)

December Industrial Production rose 1.3% y/y (forecast 0.5%, previous 2.2% y/y)

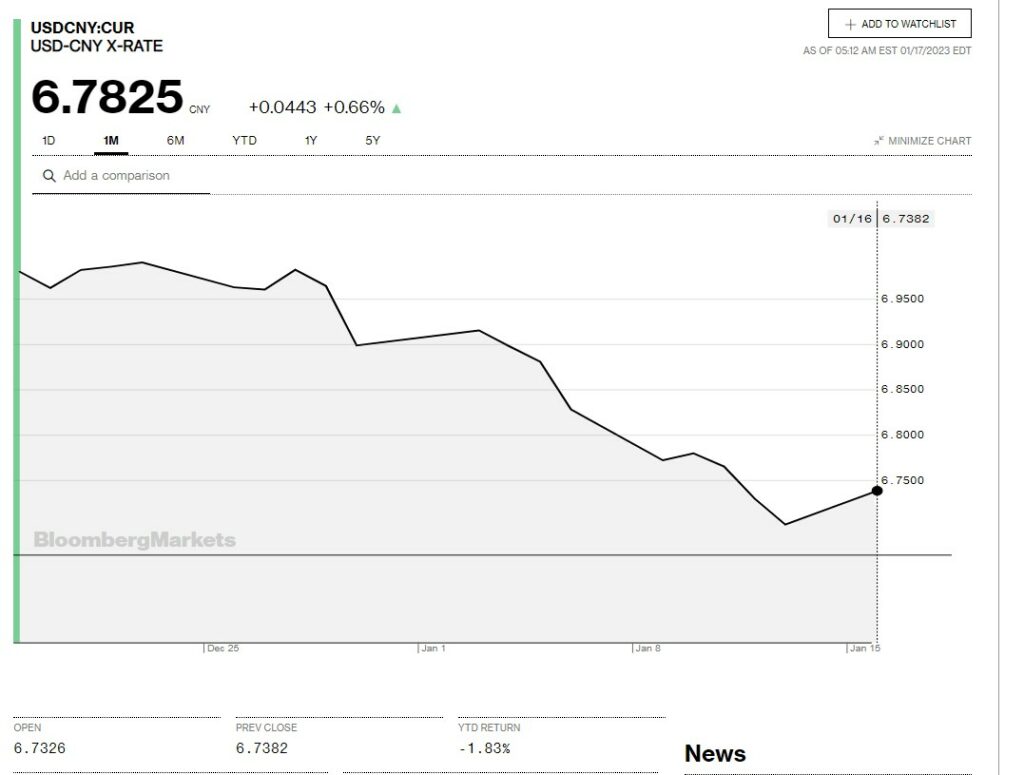

Chart: USDCNY one month

Source: Bloomberg