Photo: hdclipartall.com

January 31, 2023

- Canadian economy grows 0.1% in November

- IMF predicts UK with be the only G-10 economy to contract in 2023

- US dollar rises overnight but poised to end month sharply lower.

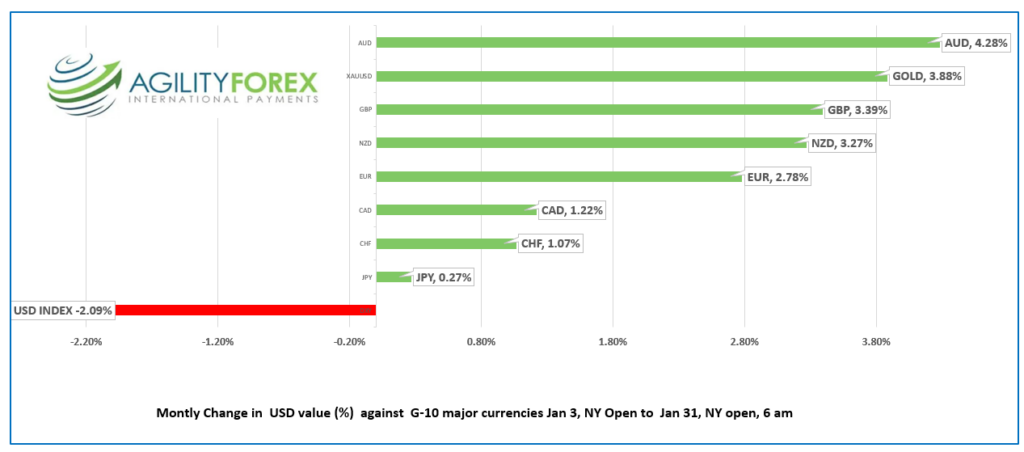

FX at a glance -monthly change

Source: IFXA Ltd/RP

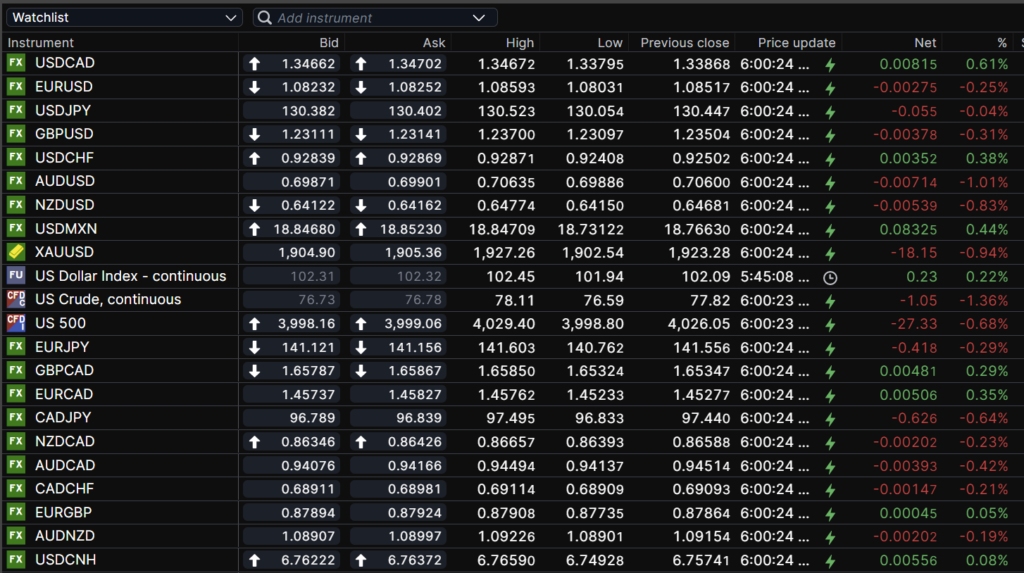

USDCAD Snapshot: open 1.3466-70, overnight range 1.3380-1.3468, close 1.3387

USDCAD rallied overnight on the back of broad US dollar demand due to a bout of risk aversion.

The Bank of Canada’s flash GDP guess for November was correct. The Canadian economy grew a mere 0.1%.

WTI oil prices dropped from $78.11/b to $76.59/b due to broad US dollar strength which also underpinned USDCAD.

USDCAD direction will continue to track S&P 500 moves. It is also month-end and the 4.64% MTD return suggests USDCAD selling as due to portfolio rebalancing.

USDCAD Technical Outlook

The USDCAD technicals flipped to bullish with the decisive break above the 1.3360-80 resistance area which also suggests a short-term bottom is in place in the 1.3000-10 area.

The technicals are bullish above 1.3410, looking for a break above 1.3480 to test resistance in the 1.3530-50 area. A move above 1.3550 targets the 1.3670-1.3700 area.

For today, USDCAD support is at 1.3390 and 1.3360. Resistance is at 1.3450 and 1.3490

Today’s range 1.3280-1.3360

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

Traders preferred to view market risk with a jaundiced eye overnight and bought US dollars while selling stocks. They are starting to fear that the Fed may strongly disagree with the market view that US rates will be cut sooner than expected.

The also were not overly enthusiastic after the IMF predicted that the global economy would slow further in 2023, blaming inflation and Russia’s war in Ukraine for the weakness. The predict US growth at 1.4% and Canada’s a tick better at 1.5%.

Source: IMF

The US dollar opened with gains across the board compared to Monday’s close, but the rally is mostly due to profit-taking and position adjustment ahead of Wednesday’s FOMC decision. However, it’s a different story for the greenback since the start of the year. China’s sudden reversal from covid-zero policies to reopening the economy to the world with open arms, powered the Australian dollar to a 4.28% gain in January, making it the best performing currency. The Japanese yen was the laggard after government and BoJ officials leaned against monetary policy tightening euphoria.

Asian equity indexes followed Wall Street’s lead and closed lower. Japan’s Nikkei 225 index finished down 0.39% while Australia’s ASX 200 finished close to unchanged. European bourses opened soft and are all in negative territory with a 0.90% drop in the UK FTSE 100 index leading the parade.

S&P 500 futures rallied from a lost of 0.67% overnight to just about unchanged after today’s Q4 Employment Cost Index rose just 1.0% rather than 1.1% forecasted.

EURUSD dropped to 1.0803 from 1.0859 range in Europe, undermined by weaker retail sales in Germany. Prices rebounded to 1.0848 following the US employment cost index data and the subsequent rebound in S&P 500 futures. EU Q4 GDP rose 0.1% q/q (forecast -0.1% q/q) and 1.9% y/y (forecast 1.8%) also underpinned prices.

GBPUSD has a negative bias in a 1.2309-1.2370 range after the IMF said the UK would be the only major G-10 economy to shrink in 2023. In addition, widespread US dollar demand ahead of Wednesday’s FOMC meeting undermined the currency. Traders fear that the ECB will be more hawkish than the BoE which will lift EURGBP and put negative pressure on GBPUSD.

USDJPY was uneventful, trading in a 130.05-130.52 range. Japanese consumer confidence rose to 31 in January from 29.3 in December.

AUDUSD declined in 0.7000-0.7064 range. Sentiment soured when December retail sales data showed a drop of 3.9% m/m , well below the forecast for just a -0.3 decline.

The US data calendar has Consumer Confidence, Chicago Purchasing Managers Index ,and Case-Shiller Home Price Index.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

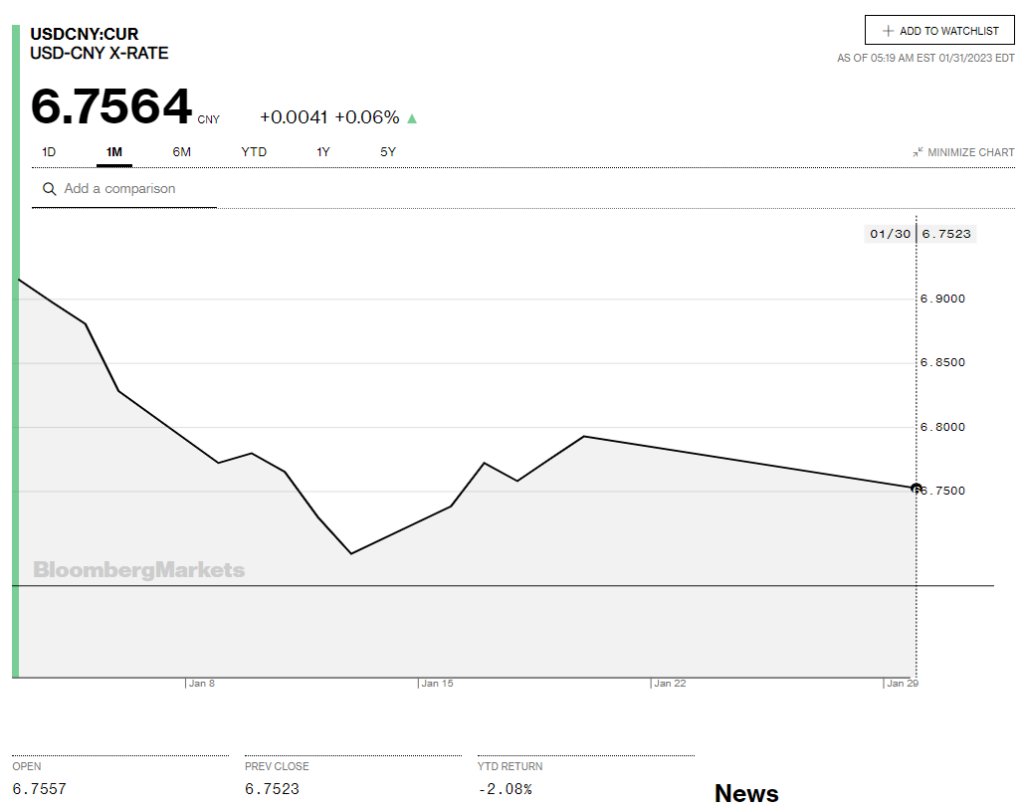

China Snapshot

Bank of China Fix: 6.7604 Previous 6.7626,

Shanghai Shenzhen CSI 300 fell 1.06% to 4156.86.

December Manufacturing PMI climbed into expansion territory at 50.1 compared to 47.0 in December. Non-manufacturing PMI rallied to 54.0 from 41.6 in December, due to pent up demand as services areas reopened.

IMF forecasting 2023 growth at 5.2%.

Chart: USDCNY 1 month

Source: Bloomberg