Photo: Wikimedia commons

March 3, 2023

- Fed policymakers muddling the message make markets chaotic.

- Soft Eurozone data weighs overshadows hawkish ECB comments.

- US dollar retreats overnight and poised to head the week with losses.

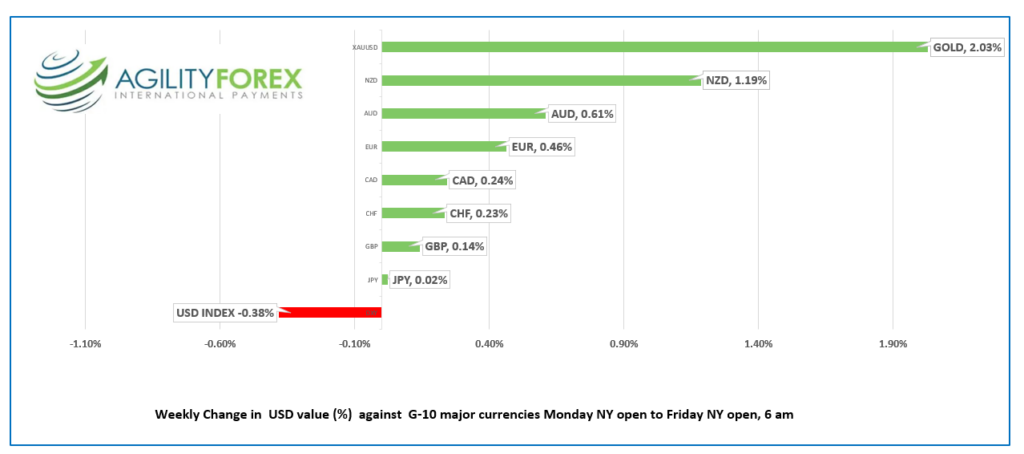

Weekly FX at a glance

Source: IFXA Ltd/RP

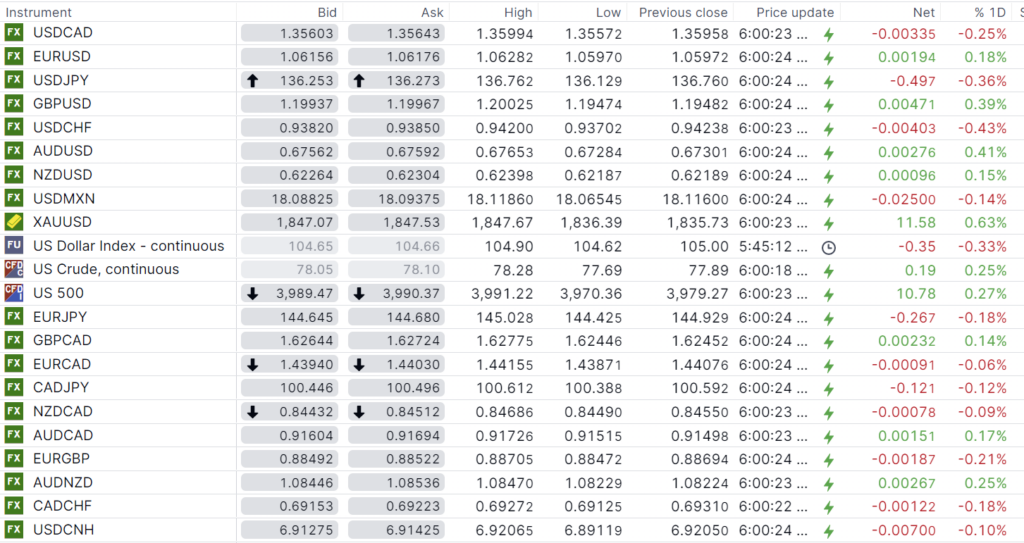

USDCAD Snapshot: open 1.3560-64, overnight range 1.3557-1.3599, close 1.3596

USDCAD retreated yesterday on the back of US dollar selling vs the majors and higher oil and commodity prices. The end result is that USDCAD is sitting just below the middle of the 1.3530-1.3665 range that has contained prices since last Friday.

Traders are looking ahead to Wednesday’s Bank of Canada monetary policy report without a lot of enthusiasm as there is no press conference. The BoC essentially pre-announced that rates will be left on hold.

WTI oil prices traded in a $77.69-$77.28 range, underpinned by the drop in the US dollar against the majors and by hopes of renewed Chinese demand.

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish while prices are below 1.3610, looking for a break below 1.3550 to extend losses to 1.3510, and the 100-day moving average at 1.3498. A break above 1.3610 targets the 1.3660-80 resistance zone.

The weekly USDCAD chart suggests that the downtrend line from October 2022 has been breeched with last week’s move above 1.3520, opening the door to further gains to 1.4000.

For today, USDCAD support is at 1.3550 and 1.3510. Resistance is at 1.3610 and 1.3660.

Today’s range 1.3550-1.3650

Chart: USDCAD 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

“Hike, Pause, Hike, Pause, Hike, Hike, Hike.” Fed policymakers need to stop talking, headline writers need to be more accurate, and traders need to stick to a view for longer than a few hours.

Global markets have been chaotic in recent days and weeks as traders react to contradictory data reports and flip-flopping Fed policymaker views. It’s enough to make one long for the pandemic days when heavily masked Fed speakers messages were muffled.

Wednesday, Minneapolis Fed President Neal Kashkari and FOMC voter said he was leaning towards raising rates beyond his previous peak of 5.4%. Atlanta Fed President Raphael Bostic advocated hiking rates to 5.0-5.25% and leaving them there until 2024.

Yesterday, rate-hawk Bostic who apparently likes seeing his comments scorch markets, repeated his remarks but when asked about a pause, said “I would expect that we could be in position by the middle of the summer, late summer. We’ll have to see sort of where things are.”

Headline writers focused on “pause.” The S&P 500 which was tumbling, reversed and turned an ugly loss into a 0.76% gain. The US dollar retreated, and commodity prices rose. And Bostic doesn’t even have a vote on the FOMC.

Fed Governor Christopher Waller added his voice to those warning of higher rates for longer, late yesterday. He’s a voter, but traders ignored him.

The incessant Fed yammering serves only to confuse markets, especially if they aren’t singing from the same songbook. Enough already.

Asian equity indexes closed with gains across the board, led by a 1.56% rally in Japan’s Nikkei 225 index .European bourses are trading positively with the German Dax gaining 1.12%. S&P 500 futures are up 0.35% while gold gained $11.76.

EURUSD traded in a 1.0597-1.0628 range. Soft Eurozone PMI data overshadowed hawkish comments from ECB officials. S&P Global February Services PMI dipped to 52 from 52.3 in January. The January Producer Price Index fell 2.8% compared to forecasts for a 0.3% dip. ECB Governing Council member and Estonian central bank governor Madis Muller warned that more rate hikes will follow the expected 50 bps this month. His colleague Bostjan Vasle said the same thing. The short term EURUSD technicals are bearish below 1.0680.

GBPUSD bottomed out at 1.1947 in Asia and drifted up to 1.2003 in early NY. The currency pair got a lift after S&P Global Services PMI rose 53.5 in February compared to 53.3 in January. However, gains are limited following BoE Governor Bailey’s somewhat dovish view of UK rates and expectations that UK economic growth will lag that of other G-7 countries. GBPUSD technicals are bearish below 1.2080.

USDJPY retreated from 136.76 to 1.3603, where it sits in NY after the US 10-year Treasury yield dropped from 4.072% at yesterday’s close to 4.003% today.

AUDUSD climbed from 0.6728 to 0.6765 do the higher China Services PMI data and broad-based US dollar weakness. The RBA is expected to raise rates by 50 bps on March 7 but deliver a dovish statement as recent data shows slowing inflation and economic growth.

The ISM Services PMI data along with speeches from Fed policymakers Lorie logan, Raphael Bostic and Michelle Bowman.

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

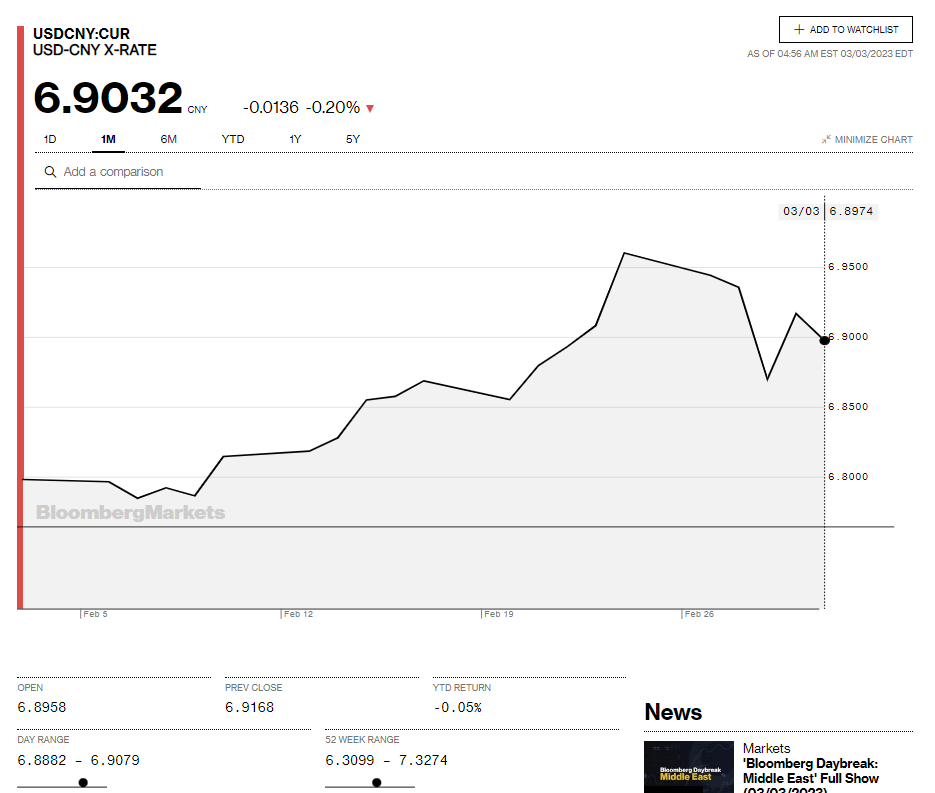

China Snapshot

Bank of China Fix: 6.9117, Previous: 6.8808

Shanghai Shenzhen CSI 300 rose 0.31% to 4130.55.

Caixin Services PMI rose to 55 in February (January 52.9)

PBoC Deputy Governor Liu Quoqiang said China’s economy is improving but there are still uncertainties.

,Annual meetings of Chinese legislature and the top political advisory group are this weekend.

Chart: USDCNY 1 month

Source: Bloomberg