Photo: Pixabay

March 9, 2023

- BoJ Governor Kuroda’s final meeting tonight

- Markets cautious ahead of US data- NFP on Friday and CPI on Tuesday

- US dollar rally pauses, awaiting data-CAD underperforms.

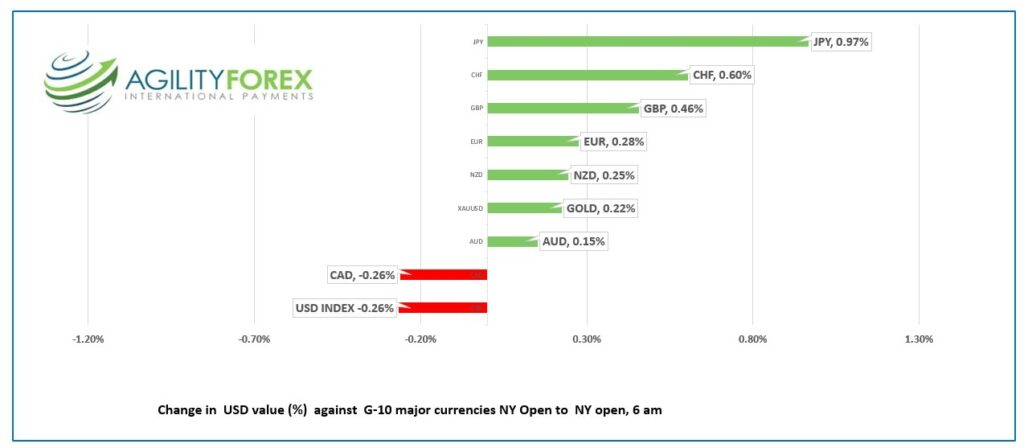

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3790-94, overnight range 1.3788-1.3816, close 1.3803

USDCAD rallied hard yesterday, powered by the dovish Bank of Canada monetary policy statement and by the latest hawkish Fed outlook.

The BoC did what they said they would and left interest rates unchanged due to their believe the previous rate hikes have done enough to bring inflation down to 3.0% this year. But they also said they could raise rates if the economy doesn’t perform as expected.

Many Canadian bank economists believe the BoC is done with rate hikes this year. If they are correct, USDCAD has more upside as Fed Chair Jerome Powell is planning to hike rates higher than previously expected.

Senior Deputy Governor Carolyn Rogers may provide more clarity on the BoC outlook today when she delivers a speech titled Economic Progress Report in Winnipeg around 1: 00 pm ET today.

There are no Canadian economic reports today.

USDCAD Technical Outlook

The intraday USDCAD technicals are bullish while prices are trading above 1.3650, looking for a break above 1.3830 to test resistance at 1.3900. However, that is unlikely to happen today. The RSI studies indicate USDCAD is overbought, suggesting a day of 1.3660-1.3830 consolidation.

The longer term uptrend line is at 1.3370, a level guarded by support in the 1.3550-1.3600 area suggests USDCAD may churn in a 1.3550-1.3900 range for the next month or so.

For today, USDCAD support is at 1.3760 and 1.3730. Resistance is at 1.3820 and 1.3850.

Today’s range 1.3740-1.3830

Chart: USDCAD 4 hour

Source: Oanda

G-10 FX recap and outlook

Will the Fed hike 25 or 50 bps at the March 22 meeting? That debate was reignited following Fed Chair Jerome Powell’s hawkish remarks during his Congressional testimony on Tuesday and Wednesday. The magnitude of the hike will be determined by Friday’s employment report and Tuesday’s inflation data.

Today’s US weekly jobless claims report muddled the rate hike debate waters. Jobless claims were 211,000, 16,000 higher than expected, which helped S&P 500 futures go from negative to unchanged.

For now, traders are content to nurse their drinks despite knowing US rates are rising higher and for longer than previously expected.

Asia equity indexes closed on a mixed note. Japan’s Nikkei 225 index gained 0.63% while China’s main indexes fell marginally, and Australia’s ASX 200 index was flat. European bourses traded defensively with the UK FTSE 100 falling 0.57%, leading the rest lower.

The US 10-year Treasury yield is steady at 3.968% after touching 4.019%.

EURUSD firmed in a 1.0539-105.81 range. Trading was quiet due to a lack of actionable Eurozone data. Gains were capped due to fears the Fed will be more hawkish than the ECB.

GBPUSD is consolidating this weeks losses in a 1.1833-1.1910range while awaiting tomorrow’s US employment report. The currency is on the defensive due to broad US dollar strength and BoE and Fed interest outlooks.

USDJPY traded defensively, falling from 137.24 to 135.95 with prices weighed down by soft Q4 GDP data. BoJ Governor Haruhiko Kuroda chairs his final monetary policy meeting Friday and Kazuo Ueda was confirmed as his replacement. Bing Chat wrote the following Haiku: Kuroda-san leaves After nine years of easing What will come next

AUDUSD climbed from an Asia low of 0.6578 to 0.6635 in NY with the peak coming on the heels of the worse than expected jobless claims data.

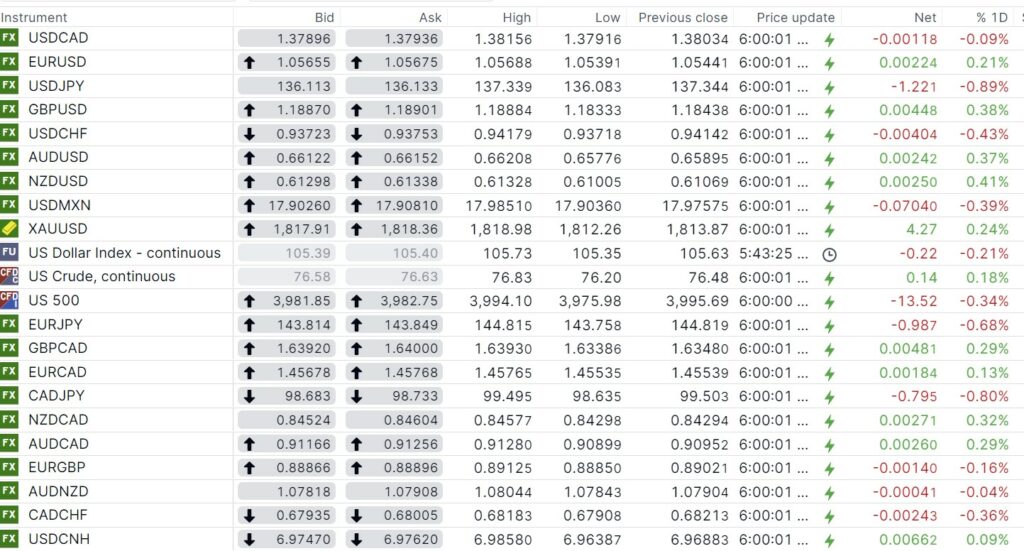

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

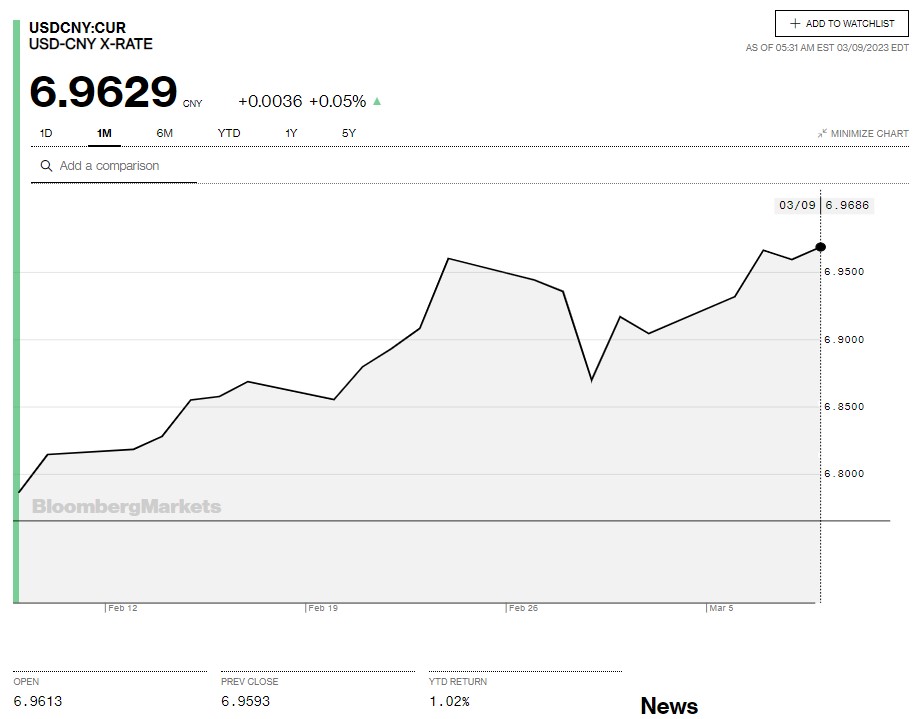

China Snapshot

Bank of China Fix: 6.9666, Previous: 6.9525

Shanghai Shenzhen CSI 300 fell 0.35% to 4019.85.

February CPI rose 1.0% y/y but fell 0.5%m/m.

Producer Price Index fell 1.4% y/y (forecast -1.3%, January -0.8%)

Chart: USDCNY 1 month

Source: Bloomberg