Photo: Pixabay

March 14, 2023

- Markets repricing Fed rate hike intentions.

- Hot inflation takes back seat to bond jitters.

- US dollar consolidating losses.

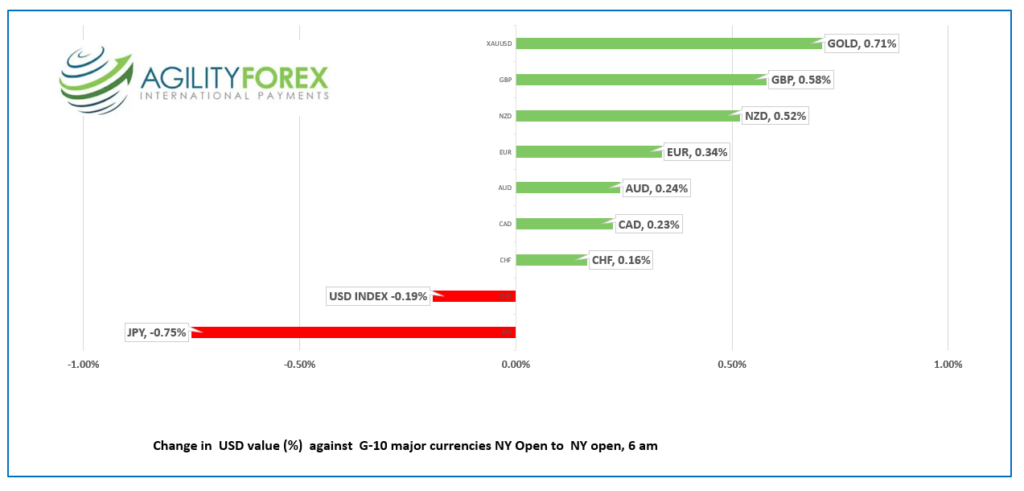

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3734-38, overnight range 1.3704-1.3748, close 1.3731

It was just last week when Bank of Canada Senior Deputy Governor Carolyn Rogers made a case for the BoC “going our own way” in setting monetary policy. The Silicon Valley Bank debacle says, “no you can’t.”

Canadian bond yields plunged in the wake of similar moves in US bonds with the Government of Canada 2 year bond yield falling 42 bps to 3.532%, and that changed the domestic narrative for rate hikes. Credit markets suggest the odds for a BoC rate cut in April are 40%. And that’s because the Fed faces a similar dilemma. So much for independent monetary policy.

Markets have quickly reduced their guess for the Fed’s terminal Fed Funds rate from around 5.7% to 5.0%. That downgrade fueled wide-spread USDCAD selling (alongside all the major G-10 currencies).

Markets are befuddled and today’s US inflation report may not provide any clarity as the Fed may be more focused on the health of the US banking system then CPI.

Canada Manufacturing PMI is expected to rise 3.9% (previous -1.9%)

USDCAD Technical Outlook

The intraday USDCAD technicals are bearish below 1.3770 looking for a break below 1.3705 to extend losses to 1.3660. A move above 1.3770 targets 1.3860.

The uptrend line from February 14 is intact above 1.3660 with a break above 1.3860 targeting 1.4000. A break below 1.3660 puts the 100-day moving average at 1.3500, then 1.3315 in play.

For today, USDCAD support is at 1.3710 and 1.3660. Resistance is at 1.3770 and 1.3820.

Today’s range 1.3670-1.3770

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

The outlook for US rates is akin to a dog’s breakfast, or at least a dog’ poker game.

Analysts at Nomura Securities are predicting the Fed will cut rates by 25 bps and stop quantitative tightening, next week. Barclay’s Bank and Goldman Sachs analysts are saying the Fed will pause its rate hike program, while UBS economists say the Fed will keep hiking. They think the market is “overshooting in the opposite direction” and think that a hot inflation report could lead to a 50 bp hike.

US Core-CPI was hotter than expected, rising 0.5% m/m (forecast 0.4% m/m) but the y/y result was as expected at 0.5%. The results gave the greenback a bit of a bid while knocking S&P 500 futures from their overnight peak.

Asian equity indexes closed with losses, following the lead from Wall Street. Japan’s Nikkei 225 index fell 2.19% while Australia’s ASX 200 dropped 1.41%. European bourses started the day with losses but are now in positive territory except for the UK FTSE 100 index which is flat %. (as of 5:45 am PDT)). S&P 500 futures are up 0.50% while the 10-year US Treasury yield is 3.586%.

EURUSD traded1.0680-1.0748 range with the peak occurring in the wake of the US CPI report. Prices are supported ahead of Thursday’s ECB meeting where a 50 bp rate hike is still expected.

GBPUSD traded narrowly in a 1.2143-1.2202 range. The UK unemployment rate dipped to 3.7% (3m ending in Jan) from 3.8% previously. Average earnings ex-bonus rose 6.5% (3month y/y January) vs 6.7% previously.

USDJPY traded from 133.04 in Asia to 134.64 in NY, post CPI, supported by the US 10-year Treasury rising to 3.586%.

AUDUSD climbed in a 0.6633-0.6690 band despite disappointing Consumer and Business Confidence data.

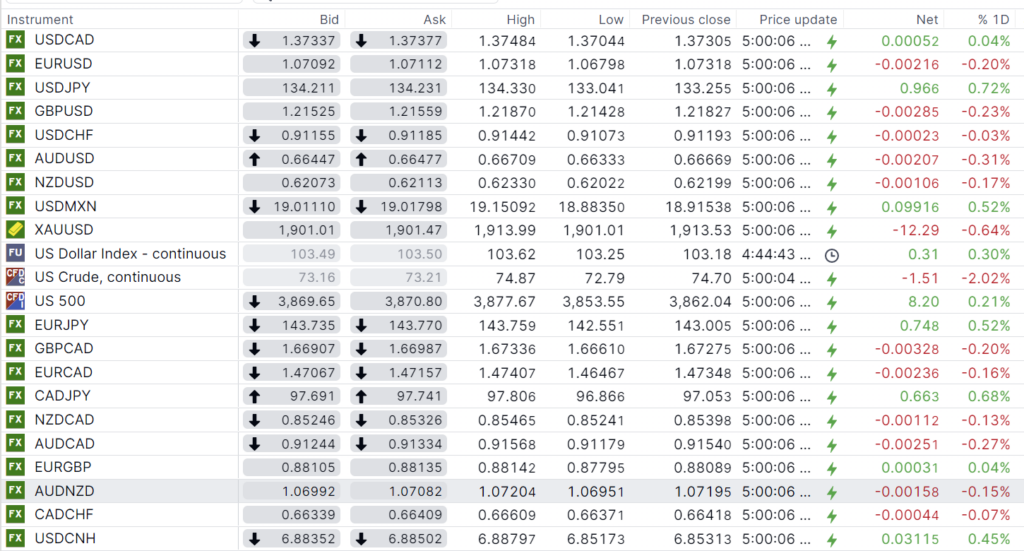

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

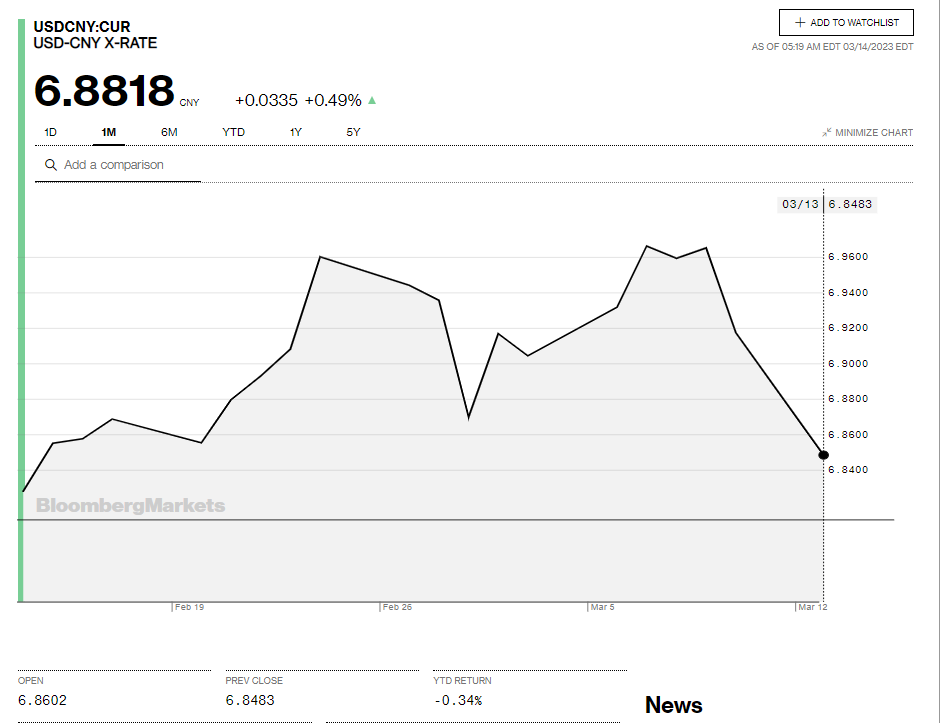

China Snapshot

Bank of China Fix: 6.8949, Previous: 6.9375

Shanghai Shenzhen CSI 300 fell 0.60% to 3984.70.

Xi Jinping rumoured to be visiting Putin next week.

Chart: USDCNY 1 month

Source: Bloomberg