Photo: pixabay

April 27, 2023

- Markets-to-ing and fro-ing into month-end and FOMC meeting.

- US Q1 GDP rises 1.1%-forecast 2.0%.

- US dollar opens mixed, trades sideways overnight.

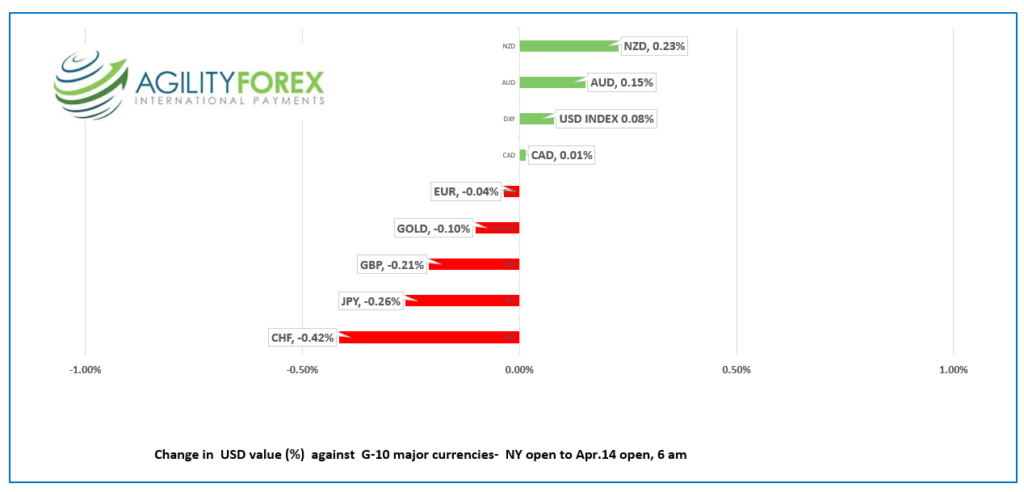

FX at a glance

Source: IFXA Ltd/RP

USDCAD Snapshot: open 1.3632-36, overnight range 1.3618-1.3644, close 1.3636

USDCAD traded narrowly overnight and managed to retain its modestly bullish bias despite improved risk sentiment following Meta’s quarterly earnings data, thanks to falling oil prices.

WTI oil fell sharply again on Wednesday, dropping from $78.09/b to $74.20, then traded in a $74.27/b-$74.81/b range overnight. The drop occurred even after the Energy Information Administration (EIA) reported US crude inventories fell by 5 .0 million barrel in the week ending April 21. The decline also filled the gap that occurred on April 3, after Opec surprised the world with another round of production cuts. If Opec’s aim was to boost prices, it isn’t working at the moment. The intraday WTI technicals are bearish while trading below $77.50.

USDCAD Technical Outlook

The USDCAD technicals are unchanged from yesterday. They have a slight bullish bias while above 1.3600 (hourly chart), but the failure to take out resistance in the 1.3650 area risks further downside.

The uptrend from April 14 is intact above 1.3550, looking for a break above 1.3650 to extend gains to break above 1.3700 . A break below the 1.3550 area targets 1.3440.

For today, USDCAD support is at 1.3600 and 1.3560. Resistance is at 1.3650 and 1.3700

Today’s range 1.3570-1.3650

Chart: WTI oil 4 hour

Source: Saxo Bank

G-10 FX recap and outlook

The race to the finish is on. As far as traders are concerned, April ends tomorrow and that means month-end rebalancing flows and the release of the Fed’s favourite inflation gauge, Personal Consumption Expenditures Price Index.

The FOMC meeting is Tuesday leaving traders content to await the results and Fed Chair Powell’s press conference.

First Republic Bank’s (FRC: Nasdaq) shares were in free-fall yesterday and that soured the mood for the entire equity market. However, there is nothing like news of jumbo earnings from Meta (formerly known as Facebook) to make traders forget about banking woes. Zuckerberg’s company reported a 3% increase in earnings compared to a year earlier, easily topping analyst estimates.

The results came after hours but they were enough to staunch the flow of red ink in globally equity markets.

There is much ado about Chinese President Xi Jinping telephoning Ukraine President Volodymyr Zelensky. Reporters are not sure who initiated the call by my bet is on Zelensky because an hour later an order of Chinese food was delivered by Uber-eats.

Asian equity indexes closed with small gains except Australia’s ASX 200 index which dipped 0.32%. European bourses opened with a small negative bias but have since turned positive, led by a 0.42% gain in the French CAC-40 index. S&P 500 futures trimmed earlier gains after the US GDP data.

They US economy grew slower than expected raising the odds for a recession but the negative sentiment was offset, to a degree, by the 16,000 drop in weekly jobless claims to 230,000.

The US 10-year Treasury yield is steady at 3.454%.

EURUSD drifted aimlessly in a 1.1035-1.1063 band, supported by Eurozone data and expectations for a hawkish ECB meeting result next week. The European Commission reported that “Eurozone Economic Sentiment was broadly unchanged in the EU and Euro-area. The data noted that consumers were more optimistic than businesses.

GBPUSD traded in a 1.2442-1.2487 range. EURGBP is slowing GBPUSD gains due to the perception the ECB will be far more hawkish than their counterparts at the Bank of England. The GBPUSD technicals are bullish above 1.2400, looking for a retest of resistance at 1.2550.

USDJPY is steady in a 133.40-133.94 range ahead of tomorrows Bank of Japan monetary policy meeting. Pundits are making a big deal about the meeting being Kazuo Ueda’s first as Governor and although the consensus is for unchanged policy, analysts think he could make a hawkish tweak to the statement.

AUDUSD rallied from 0.6601 to 0.6634, garnering some support after Commonwealth Bank of Australia (CBA) Chief Economist Gareth Aird reiterated his prediction for the RBA to hike rates by 25 bps next Tuesday.

Today’s US data includes Q1 GDP, weekly jobless claims, and pending home sales.

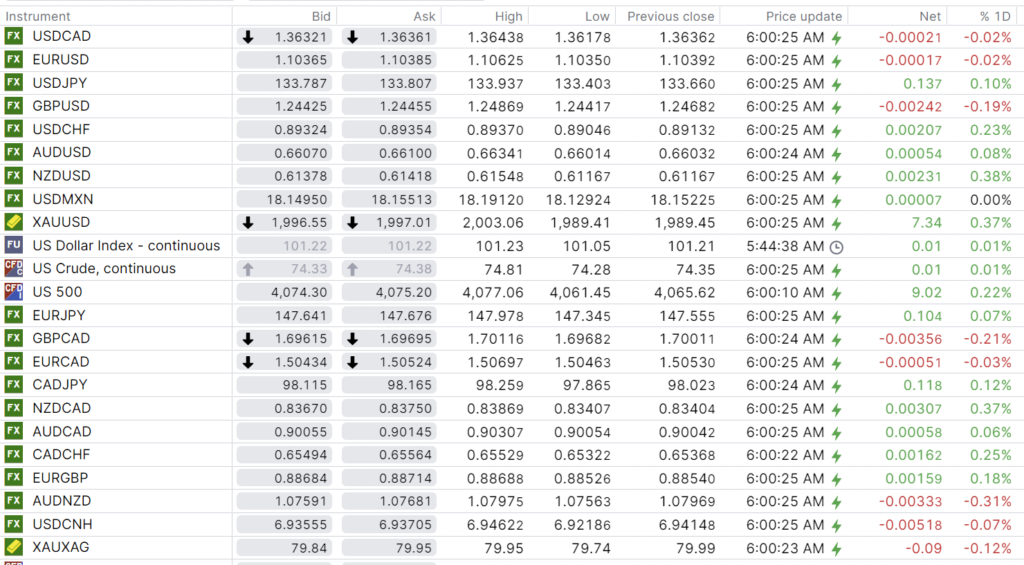

FX open, high, low, previous close as of 6:00 am ET

Source: Saxo Bank

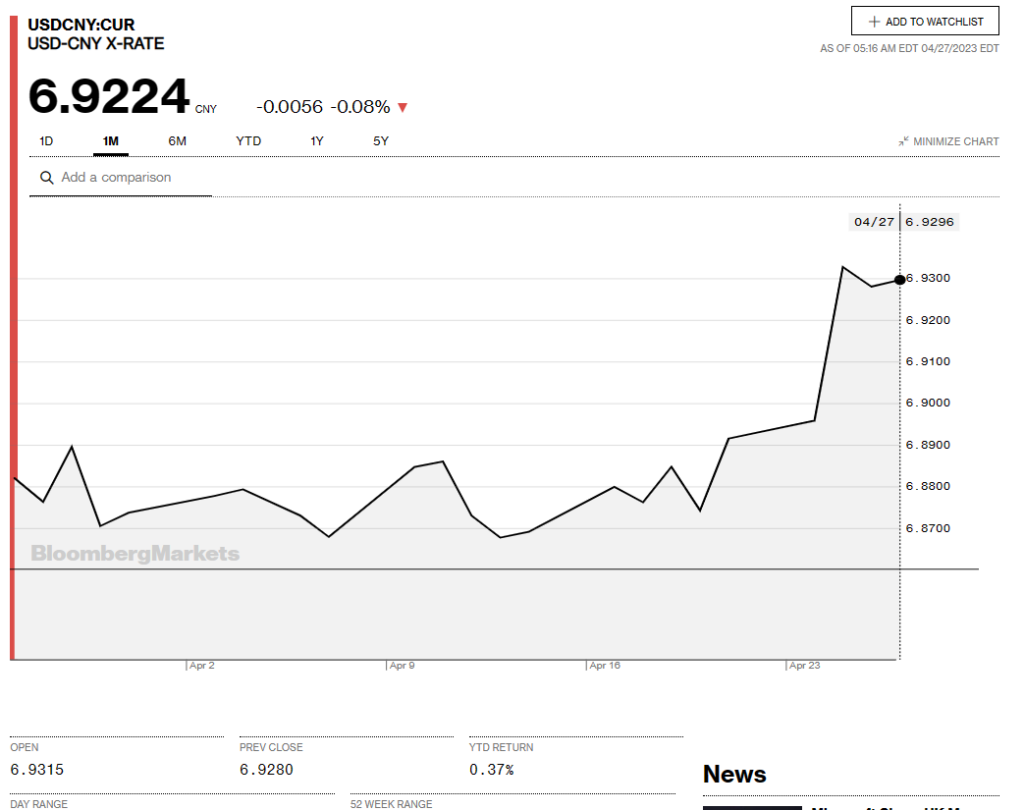

China Snapshot

Bank of China Fix: 6.9207, Previous: 6.9237

Shanghai Shenzhen CSI 300 rose 0.74% to 3988.42.

Chart: USDCNY 1 month

Source: Bloomberg