Photo: creazilla

May 31, 2023

- Chinese Manufacturing PMI weaker than expected.

- Canada’s economy a tad stronger than expected.

- USD grinds out gains into month-end.

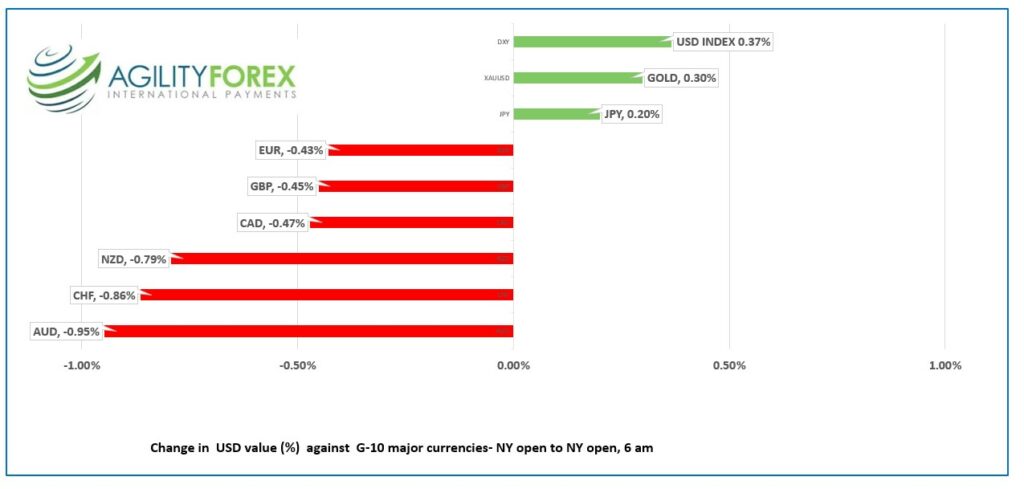

FX at a glance

Source: IFXA Ltd/RP

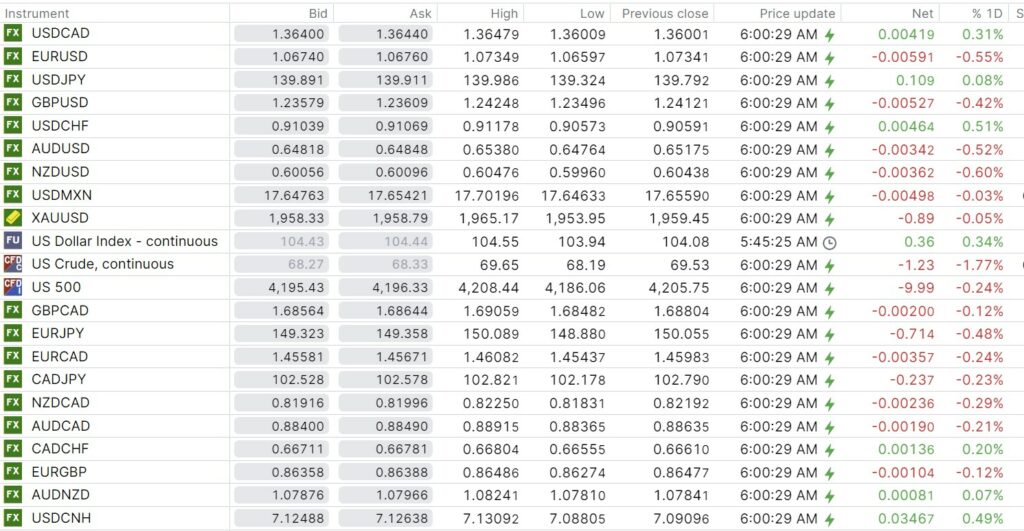

USDCAD Snapshot: open 1.3640-44, overnight range 1.3601-1.3650, close 1.3600.

USDCAD rallied on the back of weak Chinese PMI data, sharply lower oil prices and broad-based US dollar demand. However, this mornings domestic GDP data is exerting a bit of downward pressure on the currency pair.

Canada Q1 GDP rose 0.8% q/q compared to 0.4% forecast. (3.1% y/y, vs forecast 2.5%). Q2 GDP is off to a slow start as March GDP was flat, a tick lower than February’s 0.1%. Statistics Canada said,“Favourable international trade and growth in household spending were moderated by slower inventory

accumulations as well as declines in housing investment and business investment in machinery and equipment.”

USDCAD dropped to 1.3630 from 1.3650 on the news. But further losses may be limited due to falling oil prices.

WTI oil prices dropped to $67.09 from an overnight peak of $69.65/barrel. The sell-off is due to a mix of month-end flows, concerns around the US debt ceiling debate, and fears of a global growth slowdown. The latest Chinese data exacerbated the sell-off as did reports that drones caused a fire at a Russian refinery.

USDCAD direction will continue to be determined by external influences.

.USDCAD Technical Outlook

Yesterday’s mildly bearish bias turned bullish with the break above 1.3620 but the rally ran out of steam near the 1.3650-60 area. The 1.3660 zone was support in March but since dropping below that level on March 28, it has capped all upside moves.

The rally from the May 8, 1.3310 low is intact above 1.3570 with the breech of the downtrend line from March 6 (1.3560) suggesting further upside. A break above 1.3660 targets 1.3800, while a move below 1.3560 suggests a retest of 1.3400.

For today, USDCAD support is at 1.3610 and 1.3560. Resistance is at 1.3660 and 1.3710

Today’s range 1.3580-1.3680.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap and outlook

It was good while it lasted. The highly anticipated Chinese post-covid-zero economic resurgence that was expected to lift global growth appears to have come and gone.

China’s May manufacturing PMI revealed a deepening economic contraction. Emperor wannabe Xi Jinping’s heavy handed economic guidance, the ongoing property crisis, the detainment of successful businessmen, and his dream of world dominance weigh on growth.

Meanwhile back in Washington, politicians are doing their best to derail the American economy. The deal to suspend the debt ceiling for two years will be debated in the House today.

It is also month end and rebalancing flows are taking a toll on some markets. The Treasury market is one of them which helps to explain the drop in the 10-year Treasury yield from 3.85% on May 26 to 3.65% today, even though traders expect higher US interest rates.

Chinese PMI data sank Asian equity markets. Australia’s ASX 200 led the race down, losing 1.64% to finish the month with a 2.94% loss. Japan’s Nikkei 225 Index dropped 1.41% but was up 7.04% in May.

European bourses are trading negative. The UK FTSE 100 is down 0.23% and on its way to losing 4.64% for the month.

S&P 500 futures have lost 0.49% (as of 5:50 am) while gold dropped 2.6% and WTI oil is down 3.05%.

Fed decisions are data dependent, and a spate of recent data suggests further rate hikes are needed. Such being the case, today’s speeches from FOMC voting members, Michelle Bowman, Patrick Harker, and Philip Jefferson may have an outsized impact on markets.

EURUSD is trading defensively in a 1.0660-1.0734 range with prices near the bottom in NY. Sharply lower German CPI (actual 6.3% y/y vs 7.6% y/y in April combined with weaker than expected inflation data from France and Germany a less aggressive ECB interest rate policy. Meanwhile, the Fed is likely to hike rates on June 14.

GBPUSD is trading in a 1.2369-1.2425 band with the selling pressure due to global growth concerns, hawkish Fed expectations and weak Chinese PMI data.

USDJPY bounced in a 139.32-140.06 band with the bottom seen in Europe. Topside gains are limited because of BoJ FX intervention concerns and lower US Treasury yields.

AUDUSD was spanked by Chinese PMI data and fell from 0.6538 to 0.6476. Lower domestic Core CPI (actual 6.5% y/y in April vs previous 6.9%) and the ongoing US debt-ceiling issue also fueled AUDUSD selling pressures.

The JOLTS jobs opening report and Chicago PMI are due.

FX open, high, low, previous close as of 6:00 am ET

Source: Bloomberg

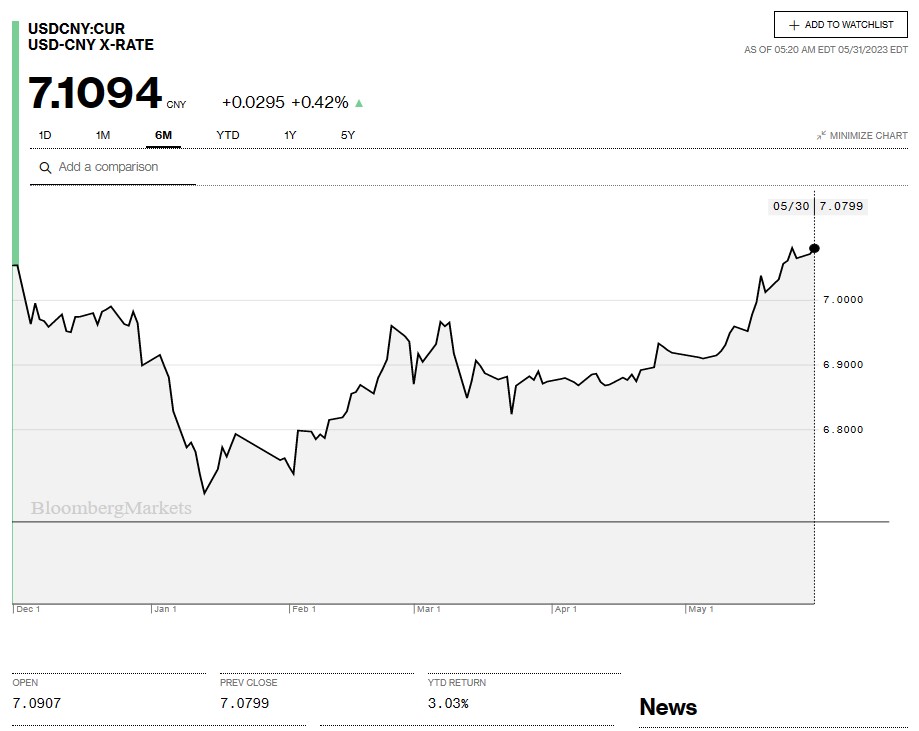

China Snapshot

Bank of China Fix: 7.0821, previous 7.0818.

Shanghai Shenzhen CSI 300 fell 1.02% to 3798.54.

May Manufacturing PMI 48.8 (forecast 49.4, April 49.2)

Non-Manufacturing PMI 54.5 (forecast 50.7, April 56.4)

Today’s PMI data suggests that the China post-Covid zero recovery has stalled and previous economic problems, including property developer woes are weighing on growth.

Chart: USDCNY 6 month

Source: Bloomberg