Photo:Bing Image Creator

August 16, 2023

- FOMC minutes on tap.

- UK inflation falls but recession risks remain.

- USD dollar remains bid due to lingering risk aversion.

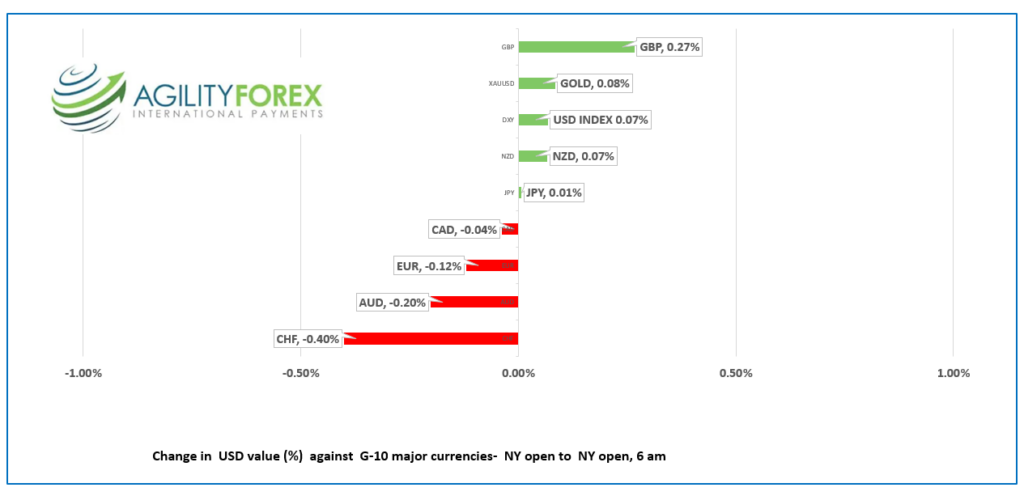

FX at a Glance

Source: IFXA/R

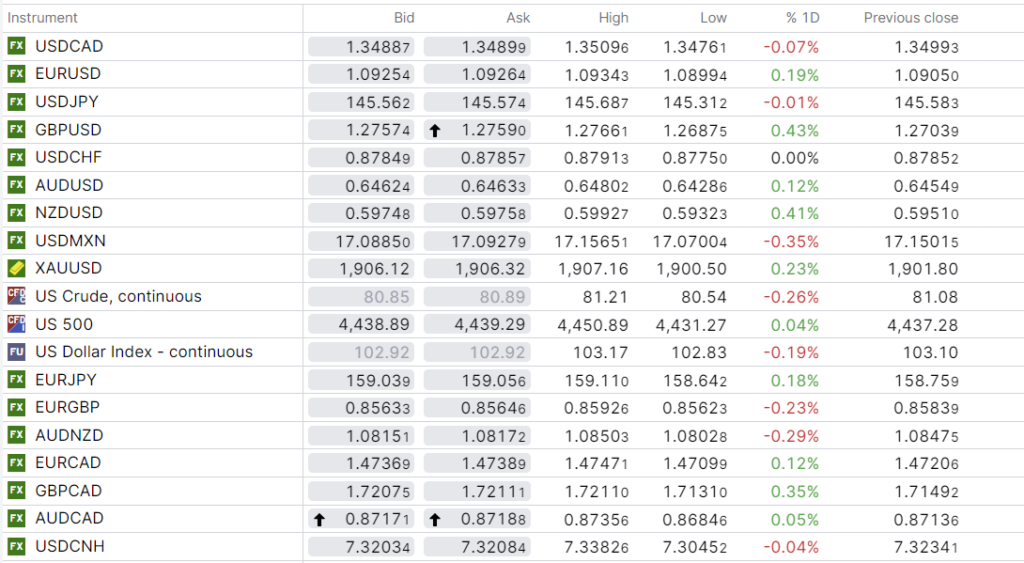

USDCAD Snapshot: open: 1.3486-90, overnight range: 1.3476-1.3510, close 1.3499.

USDCAD did not get any lasting benefit from yesterday’s hotter-than expected inflation data mainly because the devil was in the details. The Core-CPI data was a tad cooler but not enough to put a smile on any faces at the Bank of Canada and analysts are debating as to whether the BoC hikes rates in September or October.

But the prospect of higher Canadian rates didn’t translate into Canadian dollar support. Traders were spooked by Chinese growth concerns and the risk of “higher rates for longer” in the US which fueled a wave of risk aversion and USDCAD demand.

Oil prices continued their slide lower. WTI dropped to $80.54/b from $81.21/b overnight. The drop may have been worse but the American Petroleum Institutes news that crude inventories fell by 6.2 million barrels limited the downside.

Canada housing starts rose 2.8% from 235,819 units in June, according to Canada Mortgage and Housing Corporation (CMHC).

USDCAD Technicals

The USDCAD technicals are bullish above 1.3450 and looking for a decisive break above 1.3500 area to extend gains to 1.3580 then 1.3680. A break below 1.3450 targets 1.3380 but only a move below 1.3380 negates the risk for a rally to 1.3680.

USDCAD is in a steep uptrend from the beginning of the month which is guiding prices higher.

For today, USDCAD support is at 1.3450 and 1.3410. Resistance is at 1.3510 and 1.3550. Today’s range 1.3450-1.3550

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

“The US dollar is motoring along almost unimpeded as a slew of economic data underscores the resilience of the US economy and suggests the risk is to the upside for US interest rates. Yesterday’s retail sales report was the latest data with an upside surprise, rising 0.7% month-on-month compared to the 0.4% expected. There was more evidence of US economic strength today. US Building Permits rose 0.1 % (forecast -1.7%) while July Housing Starts rose 3.9% (forecast 2.7%)

Fed speak helped empower US dollar bulls. Minneapolis Fed President Neel Kashkari (voter) is debating whether the Fed has done enough to get inflation down to 2.0% or whether they need to do more. He said, “Are we done raising rates? I’m not ready to say that we’re done.”

The news knocked Wall Street lower and boosted the greenback. The US 10-year Treasury yield climbed from 4.15% to 4.23% but has since ticked lower and is at 4.18% in NY.

The minutes from the July 26 FOMC meeting are released this afternoon.

Asian equity indexes were slammed. Japan’s Nikkei 225 index closed down 1.46% while Australia’s ASX 200 index lost 1.50%. European bourses are more robust and are trading close to unchanged as of 6.40 am EDT. S&P 500 futures are flat.

EURUSD traded quietly in a 1.0899-1.0934 range. Eurozone Q2 GDP came in as expected at 0.3% quarter-on-quarter while Industrial Production rose 0.5% month-on-month compared to the downwardly revised 0.0% in May. The short-term EURUSD technicals are bearish below 1.0990.

GBPUSD rallied from 1.2688 to 1.2766 following the release of a slew of inflation measures. Headline CPI rose 6.8% year-on-year, down from 7.9% in June. Core-CPI was 6.9%, unchanged from June. The Producer Price Index was mixed while Retail Prices fell. The results do nothing to derail the Bank of England from its rate-hiking track as core inflation remains sticky. The GBPUSD technicals are bullish above 1.2570, looking for a break above 1.2820 to extend gains to 1.2900.

USDJPY was steady in a 145.31-145.72 band. Today’s Tankan Survey data complemented yesterday’s robust GDP report. Large Manufacturing sentiment rose to 12 from 3 in August.

AUDUSD underperformed against its Kiwi cousin and traded in a 0.6429-0.6480 range. The currency remains on the defensive due to concerns about China’s growth and general US dollar strength.

NZDUSD recouped Tuesday’s losses and rallied from 0.5932 to 0.5993 thanks to a “hawkish hold” from the Reserve Bank of New Zealand. The RBNZ surprised no one and left rates unchanged at 5.50% but the statement suggested the overnight cash rate (OCR) would need to remain restrictive for the foreseeable future. However, Governor Adrian Orr told reporters the statement was not forward guidance.”

Today’s US data includes Industrial Production, and Capacity Utilization.

Top of Form

FX high, low, close

Source: Saxo Bank

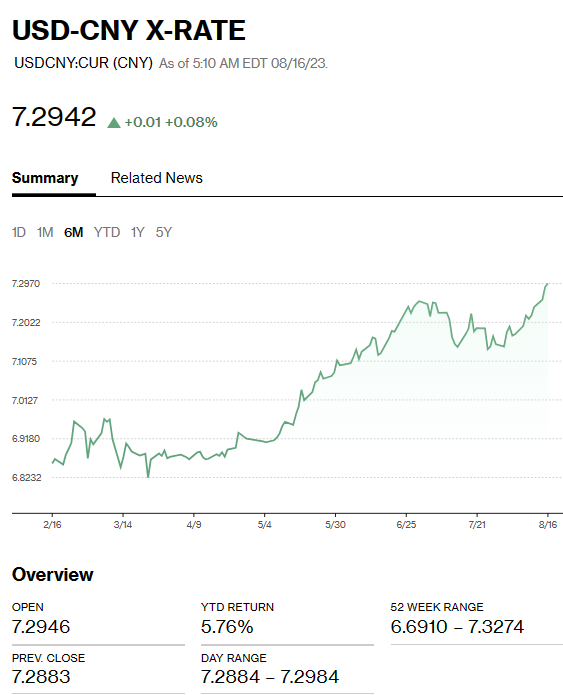

China Snapshot

Bank of China Fix: Today 7.1986 , expected 7.2878, previous 7.1768.

Shanghai Shenzhen CSI 300 fell 0.73% to 3818.33.

China stocks suffer and yuan sinks on continuing concerns over health of economy.

Chart: USDCNY 1 month

Source: Bloomberg