Photo:Bing Image Creator

August 18, 2023

- The 10-year Treasury yield retreats but remain elevated.

- Contagion fears from China’s economic malaise sours risk sentiment.

- USD dollar remains robust on safe-haven demand.

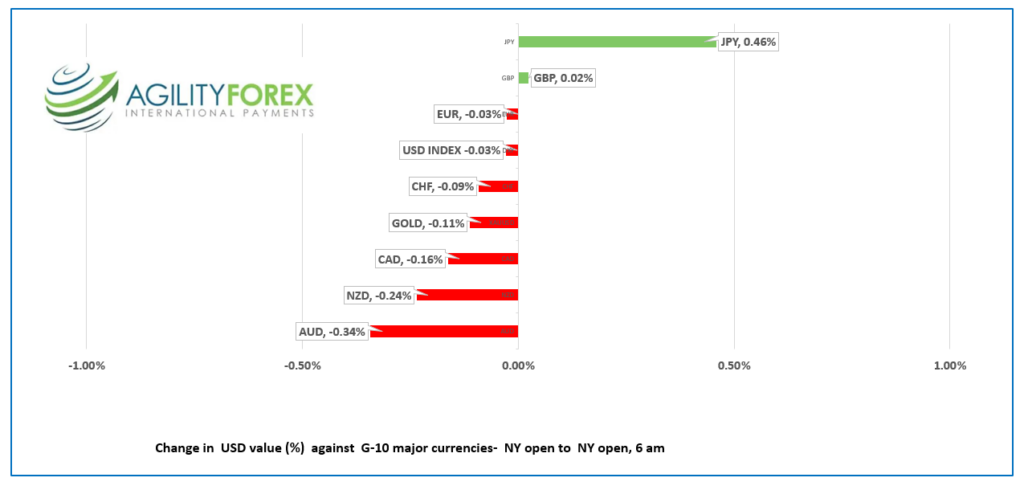

FX at a Glance

Source: IFXA/R

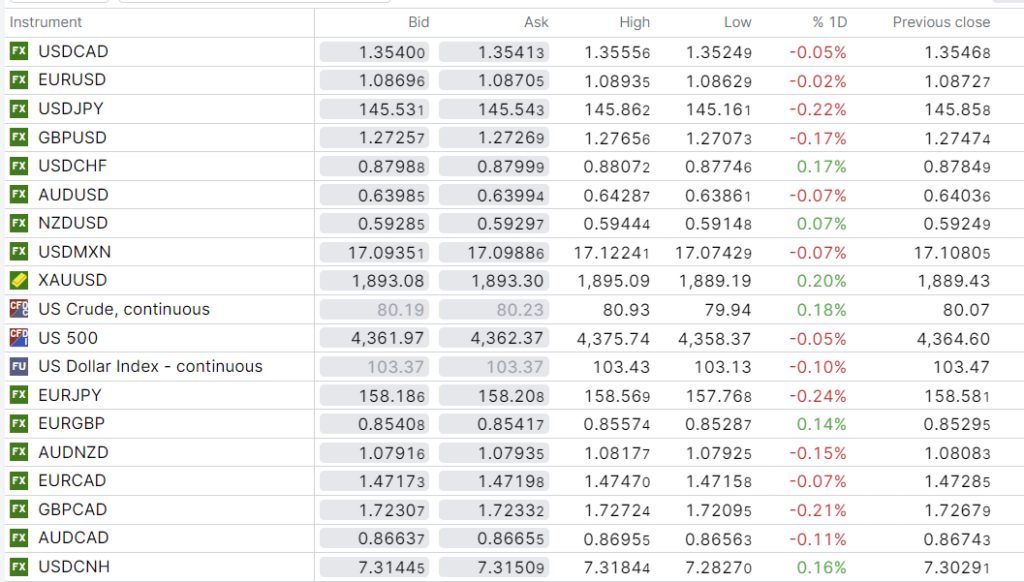

USDCAD Snapshot: open: 1.3538-42, overnight range: 1.3525-1.3574, close 1.3547.

USDCAD failed in its second attempt to crack resistance in the 1.3560-1.3580 area. Perhaps, the third time is the charm. The currency pair remains well-supported by negative risk sentiment underpinning the greenback and weighing on S&P 500 prices. The risk of a Bank of Canada rate hike on September 6 is acting as a drag on gains.

WTI oil prices are steady in a $79.65-$80.93 range. Prices are supported by the Saudi Arabian production cuts previously announced and by IEA and EIA forecasts of tight supply into year end. However, China’s economic woes suggest less demand is outweighing supply issues today.

Canada Raw Materials Prices rose 3.5% m/m in July while the Industrial Price Index data rose 0.4% (forecast -2.3%) which also supports a BoC rate hike.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3505, looking for a break above 1.3580 to extend gains to 1.3660.

Longer term, USDCAD has been climbing steadily since bottoming out at 0.9420 in July 2011. The uptrend line has survived several tests and comes into play at 1.2540 (weekly chart), a level guarded by strong support in the 1.2960 area. A break above 1.4000 puts 1.4700 in play.

For today, USDCAD support is at 1.3520 and 1.3480. Resistance is at 1.3580 and 1.3660. Today’s range 1.3530-1.3630.

Chart: USDCAD daily

Source: Saxo Bank

G-10 FX recap

Blame it on bond traders. Rising Treasury yields have roiled markets, sinking equities and boosting the US dollar. This suggests that the bond traders did not get the memo about a US recession necessitating rate cuts. A popular theory to explain the higher yields is that the strong domestic economy means the US will avoid a recession, allowing the Fed to keep rates higher for longer. The US 10-year Treasury yield was 4.304% at the close and is currently 4.262%.

China is doing its part to upset global markets. The inept mandarins in Beijing have bungled the post-pandemic economic recovery so badly that they are refusing to release key economic data. This is really no big deal, as the official numbers were mostly fantasy anyway. Yesterday’s news that China property developer Evergrande filed for Chapter 15 bankruptcy exacerbated negative risk sentiment.

Moving to Eastern Europe, Belarus President Alexander Lukashenko said he would use tactical nuclear weapons in the event of aggression.

The major Asian equity indexes followed Wall Street’s lead and closed with losses, except for Australia’s ASX 200, which was flat. The Hong Kong Hang Seng index was the biggest loser, falling 2.05%. European bourses opened softly and are trading lower, led by a 0.68% drop in the UK FTSE 100 index.

S&P 500 futures are down 0.56%.

EURUSD drifted in a 1.045-1.0894 range with the low occurring in NY. The intraday technicals are bearish while prices are below 1.0900. Eurozone economic data was not an issue. July Harmonized Consumer Prices (HICP) were 5.3% y/y, while Core-HICP was 5.5% as expected.

GBPUSD traded negatively, falling from 1.2766 in Asia to 1.2690, then bouncing to 1.2701 in NY. The currency suffered from broad US dollar strength and from disappointment after July Retail Sales fell more than expected (actual -3.2% y/y vs forecast -2.1% and -1.6% in June). Analysts are suggesting that the drop in sales was due to a mix of hot temperatures and rainy weather.

USDJPY traded in a 145.16-145.86 range, with prices undermined by the fall in the US 10-year Treasury yield, alongside a bit of pre-weekend profit-taking.

AUDUSD is on the defensive, trading in a 0.6379-0.6429 range due to China’s economic woes and broad-based US dollar strength. Additionally, the currency is being punished by the belief that the RBA rate hike cycle is over.

The US data calendar is empty.

Top of Form

FX high, low, close

Source: Saxo Bank

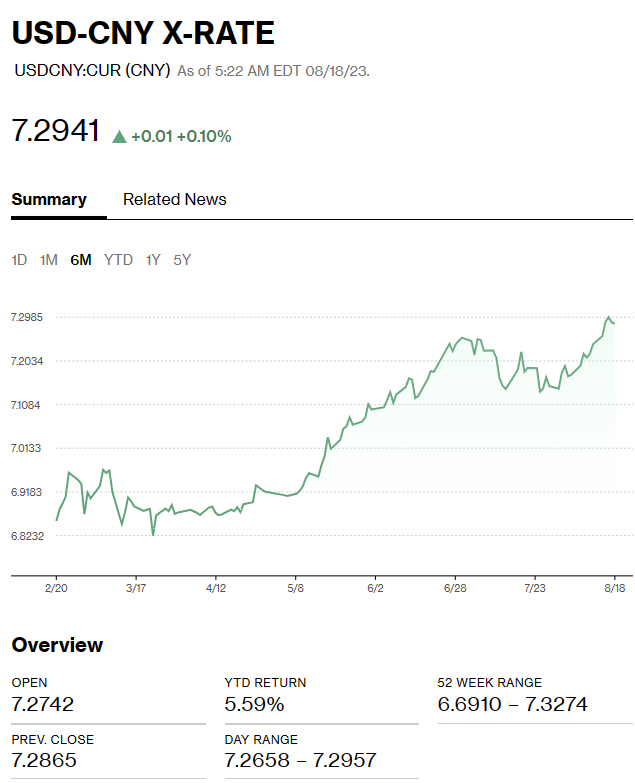

China Snapshot

Bank of China Fix: today 7.2006 , expected 7.3065, previous 7.2076.

Shanghai Shenzhen CSI 300 fell 1.29% to 3784.00.

PboC pushes back against rising USDCNY by fixing yuan 1059 below market expectations.

Chart: USDCNY 1 month

Source: Bloomberg