Photo: Bing Image Creator

September 12, 2023

- UK employment data sinks GBPUSD.

- German and ZEW data disappoints.

- US dollar grinds out small gains, CAD outperforms.

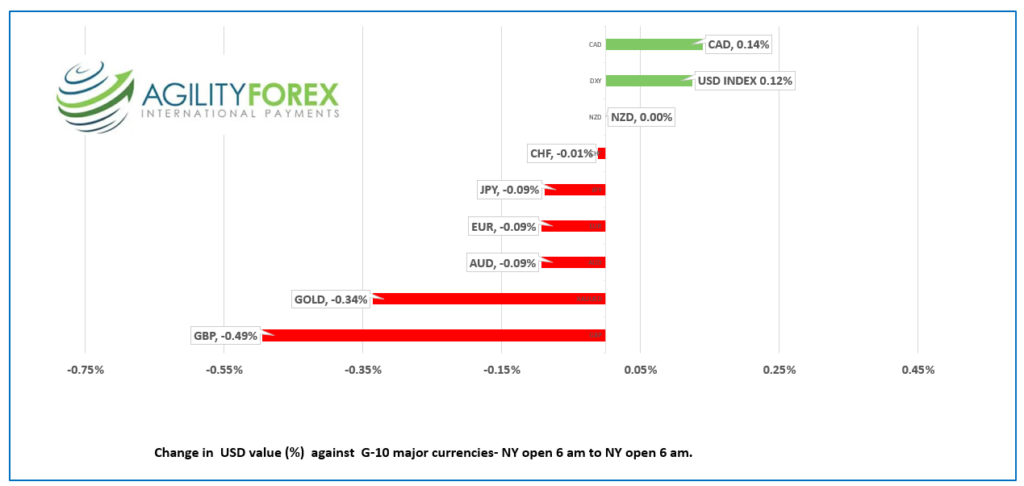

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3575-78, overnight range: 1.3559-1.3594, close 1.3576

USDCAD dipped yesterday on the heels of a general US dollar retreat against the G-10 majors. It consolidated those gains in an uneventful overnight session as traders bide their time until Wednesday’s US inflation report.

USDCAD is also being undermined by rising oil prices. WTI climbed from $87.22/b in Asia to $88.18/b in NY. Prices continue to be underpinned by the Opec and Russia production cuts but are getting an added lift from supply disruptions in Libya and hopes that the worst is over for the Chinese economy.

USDCAD direction will continue to be determined by external forces.

USDCAD Technicals

The intraday USDCAD technicals are bearish while trading below 1.3605 looking for a break below 1.3560 to target 1.3490, then 1.3460. A move above 1.3605 suggests further 1.35570-1.3660 consolidation until Wednesday’s US CPI data.

USDCAD chipped away at support in the 1.3570-80 area yesterday and touched 1.3561 before rallying back to 1.3594 overnight. The August uptrend line is tattered but not broken until a decsisive move below 1.3560. If that happens, the 1.3560-80 area will revert to resistance and USDCAD will probe support in the 1.3460 area.

For today, USDCAD support is at 1.3560 and 1.3510. Resistance is at 1.3610 and 1.36300. Today’s range 1.3540-1.3610

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

European and UK data took center stage in an otherwise uneventful overnight session, while the highlight of the US session will be the release of the monthly oil reports from OPEC.

North Korean nutbar Kim Jong-un took a slow train to Russia after hearing Vladimir Putin croon Randy Newman’s song, “You’ve Got a Friend in Me,” especially if you bring weapons and ammo that are not too crappy.

Asian equity indexes were uninspired and closed on a mixed note. Japan’s Nikkei 225 index gained 0.95%, while Australia’s ASX 200 rose 0.22%. Hong Kong’s Hang Seng Index lost 0.39%. European bourses are also mixed. The German Dax is down 0.20%, while the UK FTSE 100 index gained 0.62%. S&P 500 futures are down 0.23%.

EURUSD is near the bottom of its 1.0705-1.0768 overnight range. Prices are depressed due to soft German and ZEW data, providing more ammunition for the ECB to justify leaving rates unchanged at Thursday’s monetary policy meeting.

GBPUSD is on the back foot in a 1.2459-1.2530 range due to a weak UK employment report. The UK lost 207,000 jobs, which was offset by higher average hourly earnings, including a bonus (actual 8.5%, forecast 8.2%). The results muddied the waters for next week’s Bank of England meeting, although some analysts expect a dovish hike.

USDJPY traded in a 146.44-147.16 range. Traders are skittish, weighing threats of intervention from the Bank of Japan and Ministry of Finance against the risk of higher-than-expected US Core-CPI on Wednesday, driving up the US 10-year Treasury yield, which is at 4.28% in NY.

AUDUSD is on the defensive in a 0.6412-0.6442 band, partly due to weaker-than-expected consumer confidence data (Westpac Consumer Confidence actual -1.5% vs -0.4% in August).

The Canadian and US economic calendars are empty.

Top of Form

Top of Form

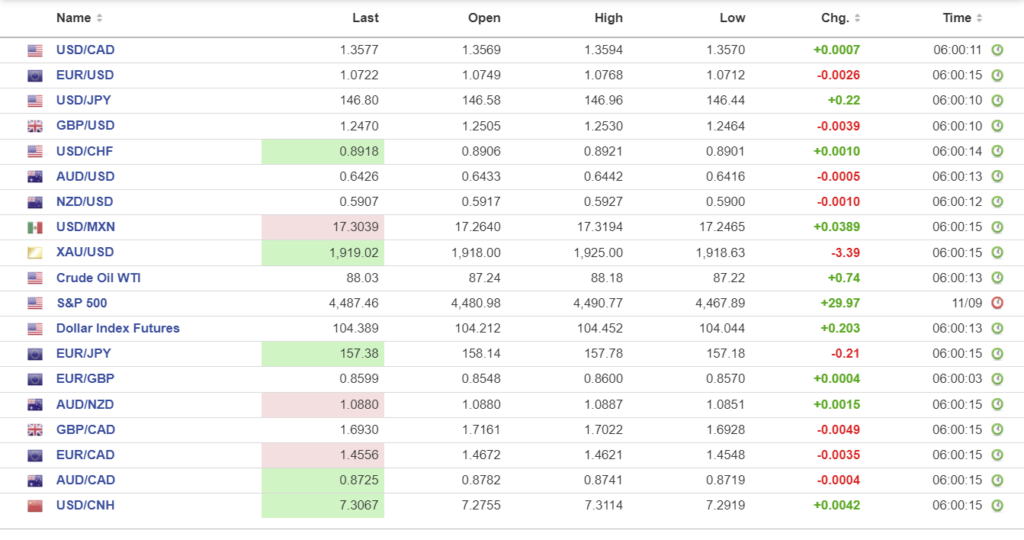

FX high, low, open

Source: Investing.com

China Snapshot

Bank of China Fix: today 7.1946, expected 7.2859, previous 7.2148.

Shanghai Shenzhen CSI 300 fell 0.18% to 3760.60.

China’s property developer woes eased somewhat after Country Garden Holdings managed to extend repayment on six yuan bonds for three years.

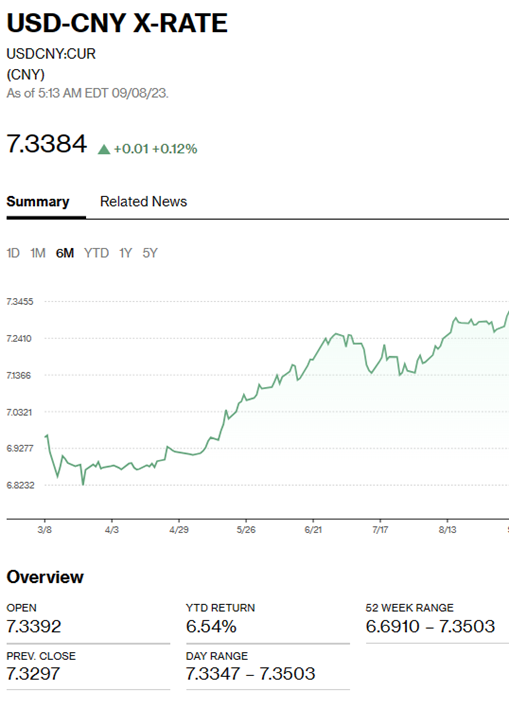

Chart: USDCNY 1 month

Source: Bloomberg