Photo: Bing AI

September 28, 2023

- Oil rally fans inflation flames.

- Risk of a US government shutdown on Oct 1.

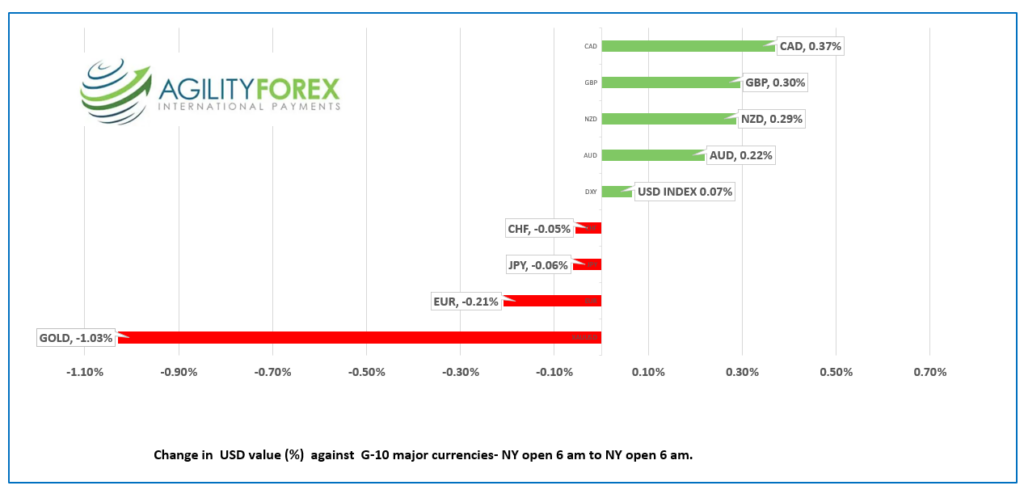

- US dollar opens mixed compared to the close. CAD outperforms.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3485-89, overnight range: 1.3476-1.3514, close 1.3498

USDCAD failed to break through resistance at 1.3550 yesterday and then road a wave of broad-based US dollar selling down to 1.3482 overnight. It’s tempting to suggest that the USDCAD losses were due to rising oil prices but if they had any impact, it was marginal. That’s because the Bank of Canada is wrestling with inflation, which rose, rather than declined in August. Higher oil prices just make the inflation file worse.

There isn’t any Canadian economic data today, leaving USDCAD direction to be determined by the US weekly jobless claims report, news about the looming US government shutdown, and comments from Fed officials.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3480 and looking for a break above 1.3550 to extend gains to 1.3600, then 1.3660. A break below 1.3480 targets 1.3420, then 1.3380.

Longer term the uptrend line on a weekly chart from April 2022, is intact while prices are above 1.3210.

For today, USDCAD support is at 1.3470 and 1.3440. Resistance is at 1.3510 and 1.3550. Todays Range 1.3460-1.3550.

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

They are dancing in the Saudi Arabian deserts under a deluge of US dollars as the Kingdom’s voluntary production cuts drive crude prices close to $100.00/b. The Saudis had announced these production reductions when WTI was trading at around $80.00 per barrel. However, even with reduced output, they are now raking in approximately an extra $1.65 billion each month compared to their earnings before the announcement.

WTI jumped to $95.03 overnight from a low of $90.42. The rally began after the Energy Information Administration (EIA) reported that US inventories shrank by 2.17 million barrels in the previous week, then gained momentum as soaring Treasury yields stoked risk aversion and raised concerns about its impact on inflation.

Traders were already jittery, thanks to Minneapolis Fed President Neel Kashkari saying that there was a 40% chance that the Fed would be forced to “meaningfully” hike rates to tame inflation.

Sentiment wasn’t helped by the increasing risk of another US government shutdown on October 1, and Moody’s warning of the rising risk of a debt downgrade.

US weekly jobless claims were 11,000 below the forecast but 2,000 higher than last week, which is insignificant and doesn’t give the Fed any reason not to raise rates November 1.

Most Asian equity markets closed in the red, led by a 1.54% plunge in Japan’s Nikkei 225 index; however, Australia’s ASX 200 squeaked out a tiny 0.8% gain. European bourses are mixed. The French CAC 40 is up 0.40%, the German Dax rose 0.22%, and the UK FTSE 100 is down 0.25%. S&P Futures are also flat. The US 10-year Treasury yield added to yesterdays gain and is sitting at 4.659%.

EURUSD suffered from broad US dollar strength and dropped to 1.0491 before rebounding to 1.0542 in early NY trading. The Eurozone Sentiment indicator (ESI) dipped to 93.3 from 93.6 in August. The results are further evidence that the economy is sluggish. In addition, the move below 1.0500 got EURUSD bears salivating and looking for further losses to 1.0400.

GBPUSD traded choppily but staged a rally from 1.2120 to 1.2220 in NY, due to a bout of profit-taking in tandem with the EURUSD rally. Even so, the GBPUSD technicals are targeting a drop to 1.2110 while prices are below 1.2240.

USDJPY traded cautiously in a 149.21-149.64 range, with the threat of BoJ intervention limiting upside moves while rising US Treasury yields provide support.

AUDUSD is at the top of its 0.6344-0.6395 range due to a mild bout of profit-taking. Australia Retail sales dipped to 0.2% m/m in August compared to the forecast for a 0.3% gain.

FX direction will be determined by US government shutdown news and Treasury yields.

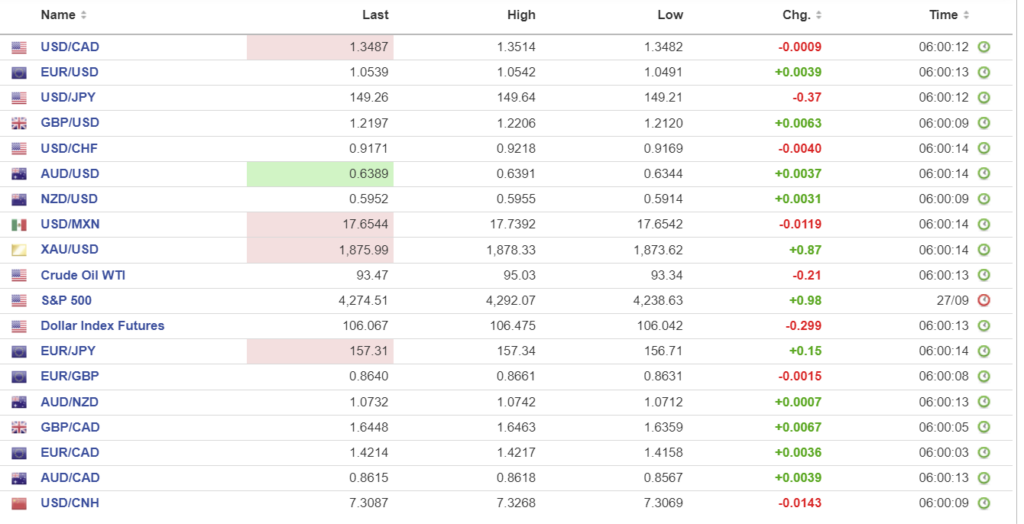

FX high, low, open

Source: Investing.com

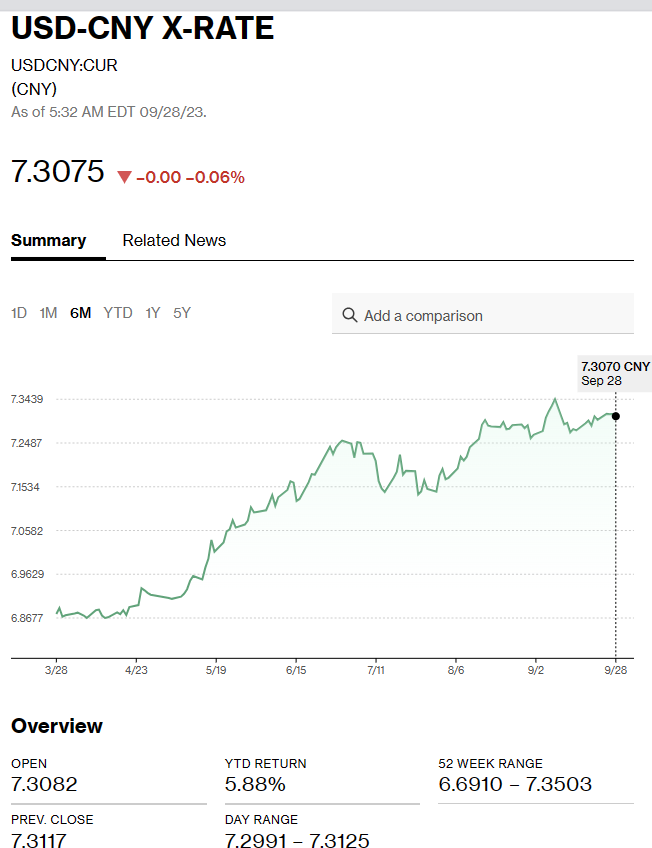

China Snapshot

Bank of China Fix: today unchanged at 7.1798, expected 7.3239, previous 7.1717.

Shanghai Shenzhen CSI 300 fell 0.30% to 3689.52.

Trading in shares of Chinese property developer Evergrande was suspended in Hong Kong.

Chart: USDCNY 1 month

Source: Bloomberg