Photo: Bing AI

October 13, 2023

- Risk aversion sentiment ticking higher.

- WTI oil grinding out gains.

- USD consolidating yesterday’s gains-AUD worst performer.

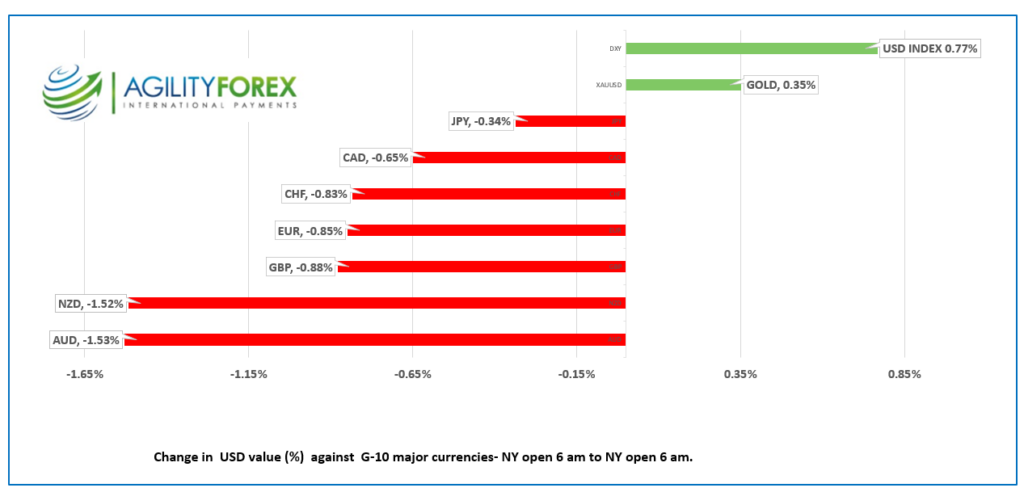

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3670-74, range 1.3660-1.36695, close 1.3693

USDCAD rallied after the US CPI data, breaking the week-long downtrend and triggered stop-loss demand, which drove prices to 1.3701. USDCAD consolidated the gains in a narrow 1.3660-1.3695 range overnight.

Traders have turned their attention to next week’s Bank of Canada Business Outlook Survey and the September CPI data for clues as to whether the BoC will raise rates on October 25.

WTI oil prices are jumped from $82.62/barrel to $85.62 yesterday then extended the gains to $86.30/b in NY today. The rally from geopolitical tensions got an added boost after the US imposed sanction on two shipping companies carrying Russian oil.

USDCAD Technicals

The intraday USDCAD technicals flipped to bullish with the break above 1.3605 and the move above 1.3660 suggests a short-term bottom is in place at 1.3570. A new intraday uptrend is intact above 1.3650, looking for break above 1.3705 to target 1.3760. A decisive break below 1.3640 suggests more 1.3570-1.3700 consolidation.

For today, USDCAD support is at 1.3650 and 1.3510. Resistance is at 1.3710 and 1.3760. Todays Range 1.3650-1.3740

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

It’s Friday the 13th, and global markets may be in for a similar experience as the counselors at Camp Crystal.

The FX reaction to yesterday’s US CPI, which was just a tick above expectations started with a trickle then became a torrent. When the dust settled, the US dollar index surged over 0.9%, rising from 105.42 to 106.36 by the end of the day.

Source: Investing.com

The reaction appears extremely overdone as the CPI results were either lower or unchanged from August. It’s not. Analysts focused on “Super-Core Inflation,” which excludes energy and shelter, and that index rose 0.6% m/m.

The problem was that markets expected a lower reading to confirm its view that US rates had peaked, and inflation would continue to grind lower toward the Fed’s 2.0% target. And they were positioned for such an event.

The spike in the US 10-year Treasury yield from 4.54% to 4.71% knocked the S&P 500 down 0.62% but yields have since dropped to 4.606% in NY.

Things didn’t improve overnight. Risk aversion soured further after Israel ordered all civilians in Gaza to evacuate within 24 hours, sparking outrage from those who believe beheading babies is a valid method to voice grievances.

Gold (XAUUSD) broke above $1900.00 for the first time in nearly a month due to the rise in geopolitical tensions which has overshadowed Fed rate hike fears.

Markets are also unnerved by US political dysfunction and the rising risk of a debt default next month, along with inflationary risks from another jump in oil prices. However, JPMorgan Chase announced better than expected third-quarter revenue, which may improve the mood.

EURUSD traded negatively in a 1.0514-1.0558 range as traders focus on diverging Fed and ECB interest rate paths and elevated geopolitical risks. The intraday technicals are bearish following the move below 1.0550 and are targeting 1.0450.

GBPUSD is tracking EURUSD and dropped to 1.2161 from 1.2226. Traders are hoping GBPUSD finds some support from speculation that the BoE may need to raise rates in the face of inflation risks from higher natural gas prices and the “higher for longer” US interest rate outlook.

USDJPY traded in a narrow 149.56-149.83 range as support from higher US Treasury yields met resistance from fears of BoJ FX intervention.

AUDUSD was the worst-performing G-10 currency due to the hawkishly revised US rate outlook and fears of slowing growth in China.

The US Michigan Consumer Sentiment report is due today.

FX high, low, open

Source: Investing.com

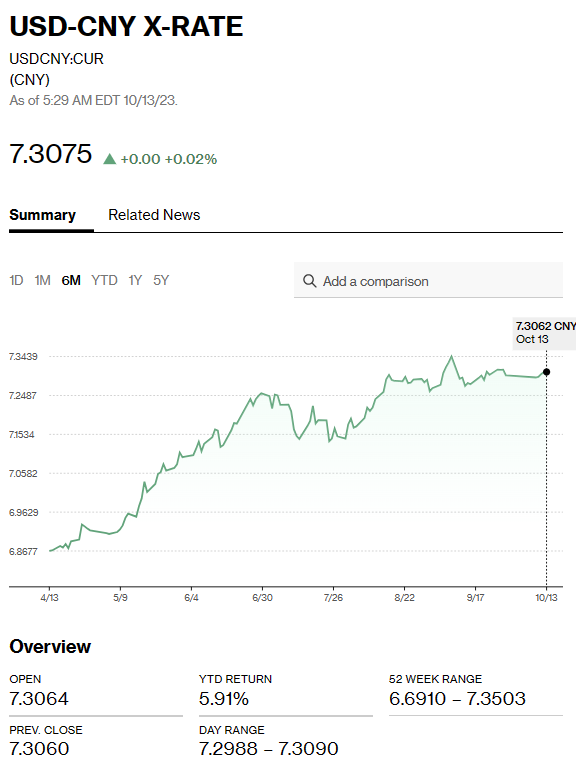

China Snapshot

Bank of China Fix: today 7.1775, expected 7.3179, previous 7.1776.

Shanghai Shenzhen CSI 300 fell 1.05% to 3663.41.

September CPI rises 0.2% m/m vs 0.3% in August and 0% y/y vs 0.1% previously. Producer Price index dropped 2.5% (forecast -2.4%)

September Trade surplus increases to $77.71 billion from $68.36 billion.

Chart: USDCNY

Source: Bloomberg