Photo: Bing AI

October 16, 2023

- Geopolitical tensions cast a pall over markets.

- Plenty of key regional data this week.

- USD slips marginally compared to Friday’s open.

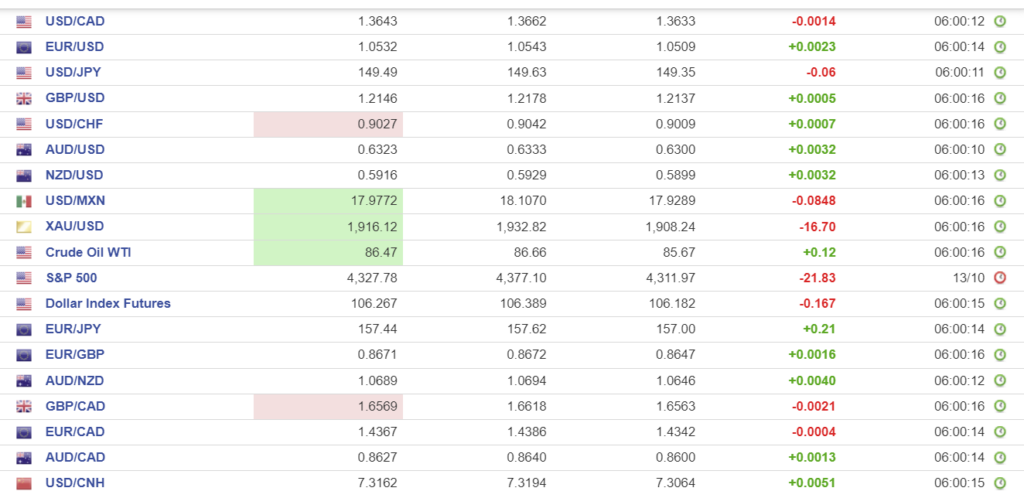

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open: 1.3641-45, range 1.3616-1.3662, close 1.3659

It’s a big week for USDCAD traders. The Bank of Canada Business Outlook Survey is today, the September inflation report and August Retail Sales are released Wednesday and Friday, respectively. The BoC monetary policy meeting is on the following Wednesday (October 25). The data will be front and center when the policymakers gather.

On Friday Governor Tiff Macklem said “What I expect it’ll focus on is, do we stay with a policy rate of five per cent and let past interest rate increases work through the economy and relieve price pressures or is the weight of the evidence of all those economic indicators, when you put them together, is it telling us that more action is needed to restore price stability.” Most economists believe the BoC will go with the first view and leave rates unchanged.

However, the Canadian data may be overshadowed by developments in Gaza.

WTI oil is at the top of its $85.67-$86.94/b range supported by the risk of supply disruptions.

Statistics Canada wrote: “Canadian manufacturing sales rose 0.7% to $72.4 billion in August on higher sales in 9 of 21 subsectors, led by the petroleum and coal (+10.5%). Wholesale sales (excluding petroleum, petroleum products, and other hydrocarbons and excluding oilseed and grain) increased 2.3% to $83.0 billion in August.

USDCAD Technicals

The intraday USDCAD technicals are bullish with the October rally intact above 1.3610 with a break above 1.3670 suggesting a retest of 1.3750. A decisive break below the 1.3540-1.3560 area shifts the focus to 1.3410.

For today, USDCAD support is at 1.3610 and 1.3580. Resistance is at 1.3650 and 1.3690. Todays Range 1.3610-1.3660

Chart: USDCAD 4 hour

Source: Investing.com

G-10 FX recap

There is a lot of regional data released this week, but the wholly justified wrath of Israel against Hamas and its Palestinian supporters may overshadow the economics.

Fed Chair Jerome Powell speaks to the Economic Club of NY on Thursday, and his remarks are expected to be a preview of the FOMC decision on November 1. Many of his colleagues have been suggesting that rates may have risen high enough to tame inflation, so the Fed can afford to be patient. Traders are hoping that Powell sings from the same song sheet.

Asian equity indexes closed in the red. Japan’s Nikkei 225 index dropped 2.03%, while Australia’s ASX 200 lost 0.36%. The UK FTSE 100 index has gained 0.37%, while the other major European bourses are flat to negative. Gold prices chopped about in a $1908.24-$1932.82 range, while US 10-year Treasury yield climbed to 4.693% from 4.629% at Friday’s close.

EURUSD bounced around in a 1.0509-1.0543 range, garnering a bit of support from somewhat hawkish comments by ECB policymakers which were largely overshadowed by geopolitical developments. EURUSD technicals are bearish below 1.0600, looking for a break below 1.0450 to extend losses to the 1.0200 area.

GBPUSD traded in a 1.2137-1.2178 range, with prices pressured by concerns that US rates could rise further while UK rates will remain unchanged. Later, GBPUSD saw a bit of strength after BoE Chief Economist Huw Pill said about inflation; “It is important that we do not declare victory prematurely, just because movements which are relatively mechanical in headline inflation are working their way through.” Traders are looking ahead to wage data on Tuesday and inflation news on Wednesday.

USDJPY drifted aimlessly in a 149.35-149.63 range. Prices were supported by rising US Treasury yields, but fear of BoJ intervention limited gains.

AUDUSD traded in a 0.6300-0.6333 range, garnering some support from news Australians rejected a proposal to alter the constitution to recognize aboriginal rights. The vote was championed by a leftist Prime Minister Anthony Albanese, and its failure is seen as a rejection of “wokeness.”

FX high, low, open

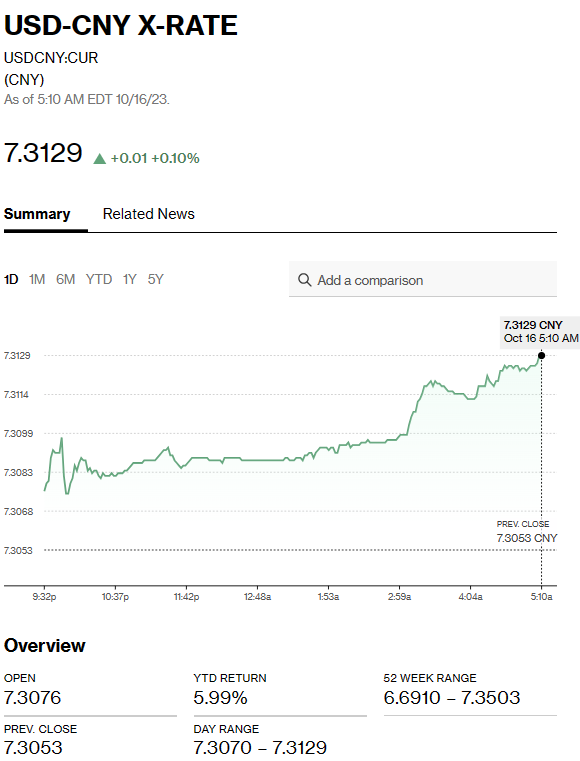

China Snapshot

Bank of China Fix: today 7.1798, expected 7.3121, previous 7.1775.

Shanghai Shenzhen CSI 300 fell 1.00% to 3626.60.

PBoC leaves 1 year MLF rate unchanged at 2.5% but injects $39.6 billion into financial system through its medium-term facility, its largest injection since 2020. A PBoC spokesperson said, “The additional liquidity injection aims to maintain stable interbank liquidity conditions amid rising LGB debt swap bond issuance, as well as stronger liquidity demand during tax payment times.”

Chart: USDCNY

Source: Bloomberg