Photo: Bing AI

October 19, 2023

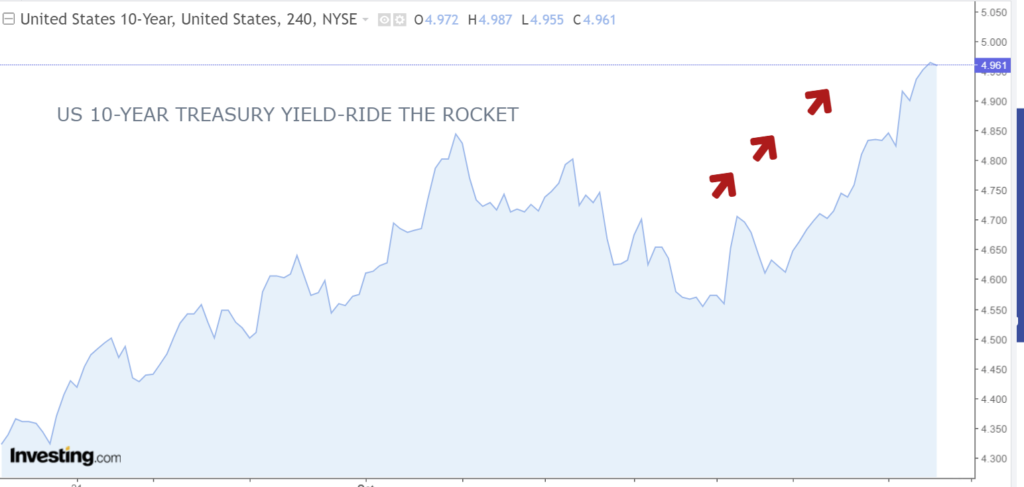

- US 10-year Treasury yield flirting with 5.00%

- Fed Chair Powell speaks to NY Economic Club at noon.

- US dollar climbs with rise in Treasury yields.

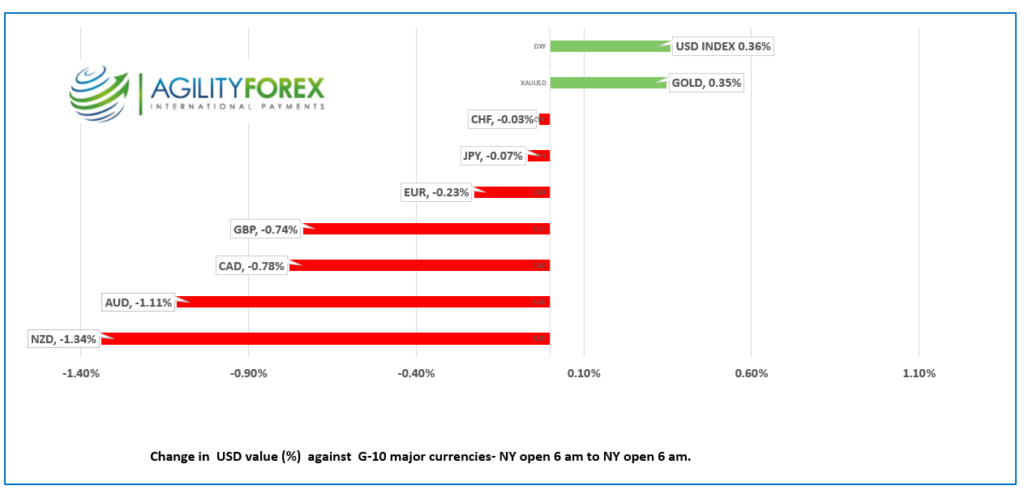

FX at a Glance

Source: IFXA/RP

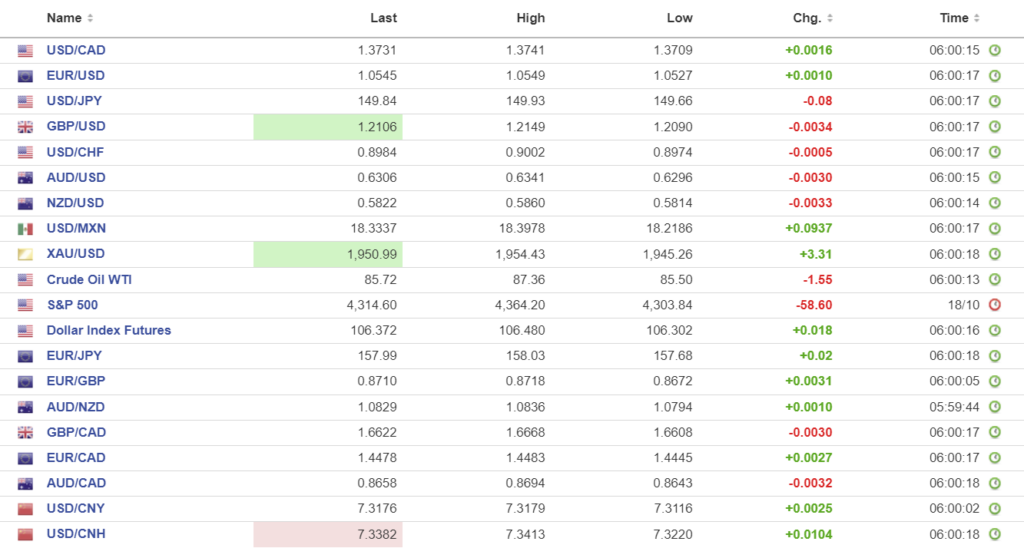

USDCAD Snapshot: open: 1.3729-33, overnight range 1.3709-1.3741, close 1.3717

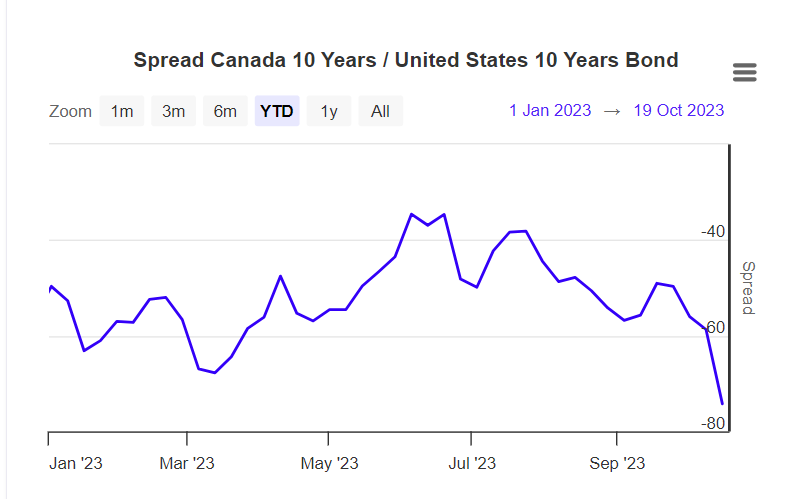

USDCAD rallied on the back of broad-based US dollar strength yesterday and consolidated the gains overnight. The rally stemmed from the surge in US Treasury yields as bond traders settle in for a prolonged period of higher US interest rates. The Canada 10-year/US 10-year yield spread is at its most negative level this year, which is providing additional fuel to the USDCAD rally.

Source: WorldGovernmentBonds.com

Higher oil prices are only a minor drag on USDCAD gains, serving to allow the Loonie to outperform against AUD and NZD, but that’s all. WTI traded in a $85.50-$87.36/b range as traders assess the risk of higher interest rates choking oil demand against a widening of the Israel-Hams war disrupting supplies.

The Canadian Raw Material Price Index rose 3.5% (forecast 2.3%) and the Industrial Product Price index rose 0.4% (forecast 0.3%) which suggests inflation may be stickier than anticipated.

USDCAD Technicals

The USDCAD technicals are bullish with the break above 1.3650 kicking off a new leg higher. The break above 1.3705 suggests a short term bottom is in place at 1.3650. A break above the October peak of 1.3780 suggests further gains to 1.3990.

Longer term, a decisive break above 1.4000 puts the Covid-peak of 1.4650 in play.

For today, USDCAD support is at 1.3700 and 1.3660. Resistance is at 1.3750 and 1.3790. Todays Range 1.3690-1.3790

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

The US Treasury yield raced higher yesterday, rising from 4.817% to close at 4.902%, then climbed further overnight, reaching 4.978% just before the NY open. That rally knocked Wall Street for a loop, with the S&P 500 index closing down 1.34%. Asia equity markets followed Wall Street’s lead, and Japan’s Nikkei 225 index fell 1.91%, while Australia’s ASX index dropped 1.36%.

European bourses are in the red, with the UK FTSE 100 index down 0.74%. S&P 500 futures are close to flat.

Yesterday, a flock of Fed officials commented on inflation and interest rates. The remarks from Michelle Bowman express concern about inflation still being too high and a strong focus on returning it to 2%, suggesting a hawkish tone. Christopher Waller, on the other hand, takes a more neutral stance by suggesting that it’s too soon to determine if more policy rate action is needed, and they can wait and watch before making definitive moves. NY Fed President John Williams acknowledges progress in reducing inflation but said rates need to remain restrictive for some time.

Today’s speeches by Chicago Fed President Austan Goolsbee, Vice Chair Philip Jefferson, Atlanta Fed President Raphael Bostic, and Philadelphia Fed President Patrick Harker will be overshadowed by Fed Chair Powell’s comments at noon.

Today, the weekly jobless claims data fell by 13,000 (actual 198,000, forecast 212,000) and once again suggested that the job market is more resilient than expected.

EURUSD is at the top of its 1.0527-1.0574 range despite a lack of support from Eurozone economic data. Traders do not seem to be overly concerned about hawkish comments from Mr. Powell today. EURUSD is bearish below 1.0600.

GBPUSD traded in a 1.2090-1.2149 range, weighed down by the risk of higher US interest rates in the face of a Bank of England on hold.

USDJPY traded stubbornly in a 149.66-149.93 range despite the surge in US 10-year Treasury yields because traders want to avoid the wrath of the Bank of Japan and Ministry of Finance.

AUDUSD traded lower, falling from 0.6341 to 0.6296 due to broad US dollar strength and a mixed unemployment report. Australia gained 6,700 new jobs, which was well below the forecast for a 20,000 increase, but the unemployment rate dipped to 3.6% from 3.7%.

Chart of the Day-US 10-year Treasury yield

Source: Investing.com

FX high, low, open

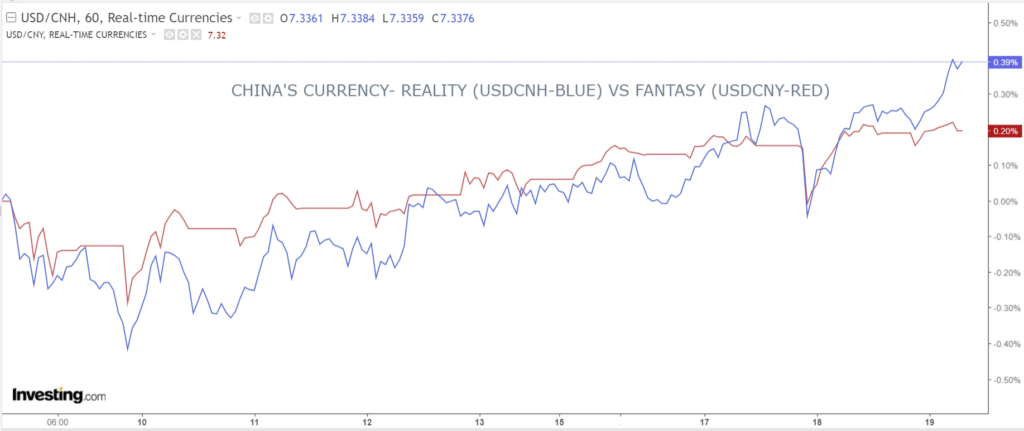

China Snapshot

PBoC fix: today 7.1795, expected 7.3226, previous 7.1795.

Shanghai Shenzhen CSI 300 fell 2.13% to 3533.54.

To look at the PBoC USDCNY rate fixings for the past three weeks, one can be forgiven for thinking that in terms of the yuan, “all is calm, all is bright.” Like all official Chinese data, the fix has little bearing on reality.

Chart: USDCNY (onshore) vs USDCNH (offshore)

Source: Bloomberg