Photo: Bing Image Creator

November 2, 2023

- Markets think the Fed is done hiking rates.

- US 10-year Treasury yield plummets 22bps since Tuesday.

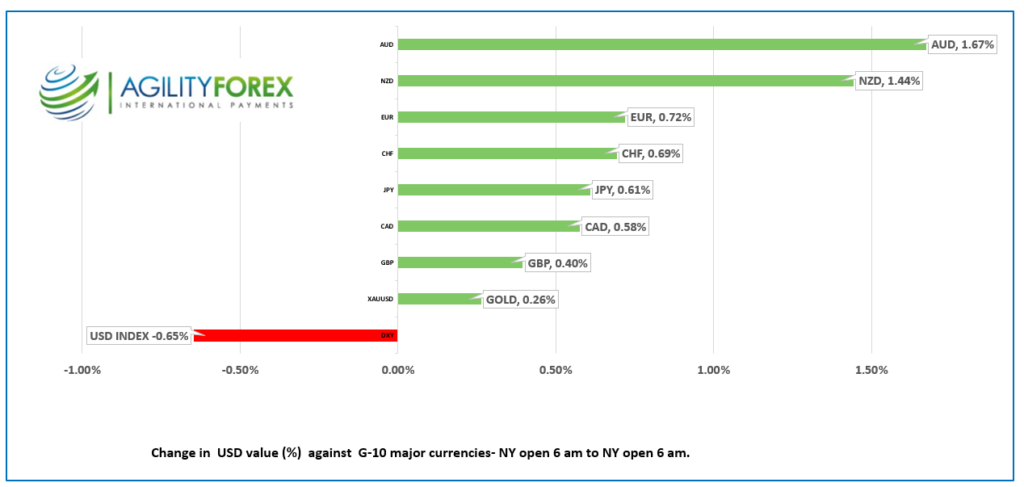

- US dollar falls against G-10 majors-AUD rises 1.67%.

FX at a Glance

Source: IFXA/RP

USDCAD Snapshot: open 1.3805-09, overnight range 1.3806-1.3861, close 1.3858

USD/CAD dropped following the FOMC meeting and the collapse in the 10-year US Treasury yield. Whether the losses are sustainable is up for debate. Fed Chair Powell sounded a tad wishy-washy when he warned that rates could still go higher while also saying financial conditions had tightened. Traders asked, “What’s it gonna be?” as breathlessly as the girl in Meat Loaf’s “Paradise by the Dashboard Light.” The outcome was the same for the girl and those short equities or long dollars.

WTI oil prices got a bit of support from the falling dollar and improved global risk sentiment, but not enough to provide the Canadian dollar with much additional support. WTI traded in a $80.72-$82.08 range overnight.

Traders are looking ahead to Friday’s Canadian and US employment reports. US non-farm payrolls are expected to rise by 180,000 jobs (September 336,000), while Canada is expected to gain 22,500 (September 63,800). If the US results are anywhere close to September’s reading, markets will be back to expecting another Fed rate hike.

USDCAD Technicals:

The hourly USDCAD technicals are bearish while trading below 1.3850 and looking for a move below 1.3805 to extend losses to 1.3770. A break above 1.3860 negates the downtrend and shifts the focus to 1.3900 then 1.4000.

The daily technicals tell a different story. The USDCAD drop from 1.3900 is merely a correction in side the uptrend channel (1.3550-1.3910) from the middle of July . The bottom of the channel is protected by the uptrend line from the beginning of October at 1.3760 and support from previous resistance in the 1.3780-90 area.

For today, USDCAD support at 1.3780 and 1.3740. Resistance at 1.3860 and 1.3900. Today’s expected trading range is 1.3830-1.3930.

Chart: USDCAD daily

Source: Investing.com

G-10 FX recap

Traders are reacting as if Fed Chair Jerome Powell announced an end to the current rate-hiking cycle. He didn’t, but those parsing the statement and his answers during the press conference have concluded that even if the Fat Lady isn’t singing, she is on the stage.

Mr. Powell wore a hawkish face when he said, “Evidence of growth persistently above potential, or that tightness in the labor market is no longer easing, could put further progress on inflation at risk and could warrant further tightening of monetary policy.”

Traders didn’t care. They paid particular attention to the addition of the word “financial” in the line in the statement that read, “Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation.” To them, that meant that the surge in Treasury yields over the past few months greatly reduced the need for further Fed action.

The “Fed-on-hold” camp got more support this morning after weekly US jobless claims rose by 5,000 to 217,000, topping the forecast and last week’s upwardly revised 212,000 result.

It was “risk-on, rally time” for global equities overnight, while the US dollar went into a tailspin. The Russian war in Ukraine, Israel’s war on Hamas, and rising US tensions with Iran were forgotten. Who cares about death and destruction when there is money to be made?

Asian equities indexes closed higher, with Japan’s Nikkei 225 index gaining 1.10% and Australia’s ASX 200 rising 0.90%. European equities followed suit, led by a 1.93% rise in the French CAC 40 index and a 1.21% jump in the UK FTSE 100 index. S&P 500 futures are up 0.68%, and the US 10-year Treasury yield sits at 4.703%, (as of 5:40 am PDT).

EURUSD rallied in the wake of the FOMC announcement and is at the top of its 1.0567-1.0659 range in early NY trading. The prospect that the Fed has finished raising rates overshadowed another poor Eurozone Manufacturing PMI report (actual 43.1 vs. 43 previously and expected). The HCOB statement said, “The slump in the eurozone’s manufacturing sector remained substantial at the start of the fourth quarter, with steep and accelerated contractions in new orders, purchasing activity, and backlogs contributing to another considerable fall in factory production. Nevertheless, the rally is just a correction, as the downtrend channel from July 27 is intact while prices are below 1.0670.”

GBPUSD traded in a 1.2138-1.2197 range ahead of the Bank of England decision., then rallied to 1.2226 afterwards. The BoE left rates unchanged as expected. Governor Adnrew Bailey justified the inaction saying “Higher interest rates are working, and inflation is falling. But we need to see inflation continuing to fall all the way to our 2% target.

USDJPY traded defensively in a 150.03-150.97 range with selling pressure stemming from lower US Treasury yields and broad US dollar weakness.

AUDUSD rallied from 0.6389 to 0.6447 due to hopes that an end to rising Fed rates will lead to improved global growth and higher demand for commodities. Traders ignored the drop in the Australian trade surplus to AUD 6.78 billion from AUD 10.161 billion in August.

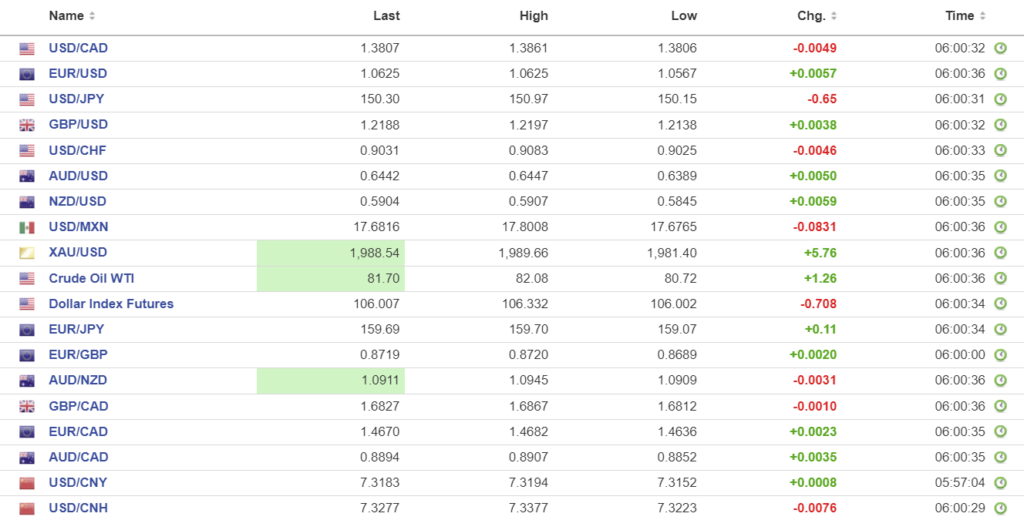

FX high, low, open

Source: Investing.com

China Snapshot

PBoC fix: today 7.1797, expected 7.3055, previous 7.1778

Shanghai Shenzhen CSI 300 fell 0.47% to 3554.19.

Chart: USDCNY (onshore) vs USDCNH (offshore) hourly

Source: Investing.com