Picture: DALL-E

November 13, 2023

- Canadian Banks are closed today.

- US inflation data due Tuesday-forecast unchanged at 4.1% y/y

- US dollar opens mixed from Friday-AUD outperforms.

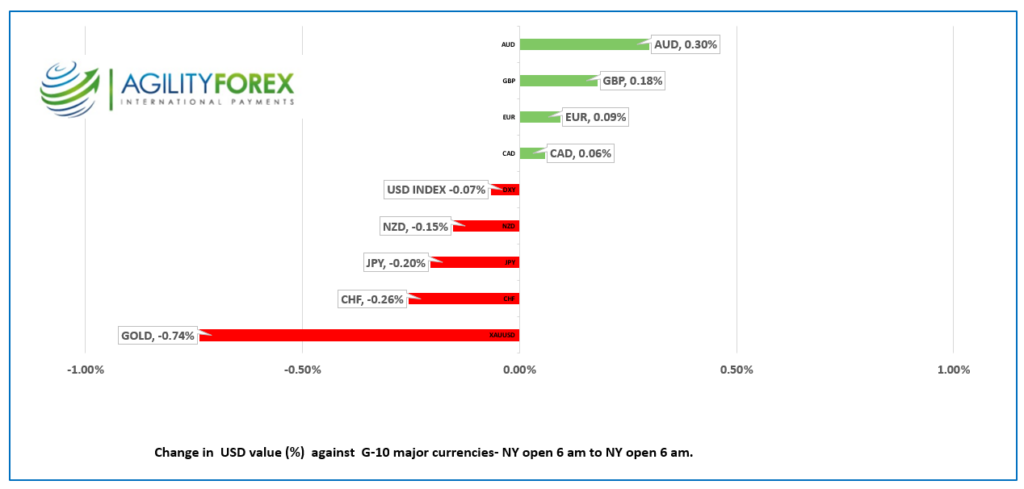

FX at a Glance

Source: IFXA/RP

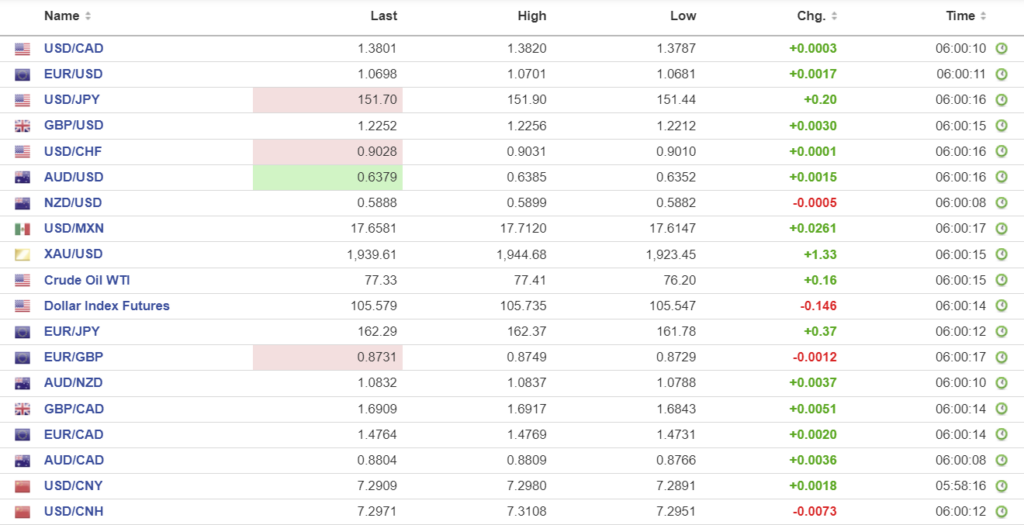

USDCAD Snapshot: open 1.3799-04, overnight range 1.3787-1.3832, close 1.3803

USDCAD went nowhere overnight, and it should have a similar fate today. That’s because Canadian banks are closed due to Remembrance Day (which fell on Saturday) and key market-moving US data (CPI) is due tomorrow.

USDCAD is also underpinned because Fed Chair Jerome Powell suggested interest rate could still rise, while traders are pricing in Bank of Canada rate cuts as early as April 2024.

Oil prices are not doing the Canadian dollar any favours. WTI oil prices have declined steadily since October 20. Prices have bounced from $75.31 on Friday to $77.33 today, but the downtrend remains intact. Prices are under pressure after reports that Chinese refiners requested lower volumes and fears that US gasoline demand will drop to its lowest level in 20 year. However, concerns of supply disruptions from the middle East is limiting losses.

USDCAD Technicals:

The intraday technicals are bullish above 1.3770, looking for a break above 1.3850 to extend gains to 1.3900, then 1.4000. A break below 1.3780 targets 1.3720.

Longer-term, the uptrend channel from July continues to guide prices higher inside a 1.3600-1.4000 band, with prices currently just above the mid-point.

For today, USDCAD support is at 1.3780 and 1.3750. Resistance is at 1.3850 and 1.3880. Today’s expected trading range is 1.3770-1.3850.

Chart: USDCAD and WTI oil daily

Source: Daily FX

G-10 FX recap

It’s a mundane Monday, and the lull in the financial markets isn’t going anywhere soon. Those poised for a repeat of Friday’s equity rally on Wall Street may find themselves disappointed, given today’s scarcity of actionable data and the cautious sentiment prevailing ahead of key events: Tuesday’s pivotal US inflation report and the high-stakes Biden-Jinping meeting on Wednesday.

Last Friday, Wall Street concluded with notable gains, defying the gravity of Fed Chair Jerome Powell’s previous day’s warning about potential further hikes in US interest rates. It seemed as if traders shrugged off Powell’s caution, propelling the S&P 500 up by 1.56% and the Dow Jones Industrial Average by 1.15%, buoyed by the dovish undertones from Federal Reserve officials Daly and Bostic.

In their 2024 financial forecast, Morgan Stanley projects the Federal Reserve’s initial rate reduction in June 2024, with subsequent decreases leading to a 2.375% rate by December 2025. Meanwhile, Goldman Sachs anticipates the first rate cut in Q4 2024, forecasting a dip to 3.5% by mid-2026.

On the political front, the US government teeters on the brink of another shutdown unless bipartisan agreement is reached on funding to sustain operations into the next year.

Asian equity indexes concluded mixed, with the exception of Hong Kong’s Hang Seng, which saw a 1.30% uplift, possibly fueled by optimism surrounding the forthcoming Biden-Xi Jinping summit and its potential to ease US-China tensions. European markets painted a positive picture, led by a 0.66% rise in the UK’s FTSE. In contrast, S&P 500 futures dipped slightly by 0.17%, with the US 10-year Treasury yield holding steady at 4.632%.

In currency markets, EURUSD maintained a quiet stance, fluctuating in a 1.0681-1.0701 range. The 1.0660 support level might be tested if upcoming comments from ECB officials don’t alter the market’s anticipation of three rate cuts in 2024.

GBPUSD hovered near the upper boundary of its 1.2212-1.2256 spectrum. Despite a 1.7% month-over-month drop in UK house prices this November and a 1.3% year-over-year decline, GBPUSD dynamics are likely to be influenced more by Tuesday’s upcoming employment and average earnings data, though the US inflation report is expected to be a major directional driver.

USDJPY inched higher within a 151.44-151.90 band, underpinned by weaker-than-anticipated Producer Price Index data and stable US Treasury yields.

AUDUSD saw a modest ascent in the 0.6352-0.6385 range, gaining some traction from comments by RBA Assistant Governor Marion Koler. Her statements hinted at a protracted battle with inflation, suggesting further rate hikes could be on the horizon.

The US economic calendar remains devoid of major releases today.

FX high, low, open

Source: Investing.com

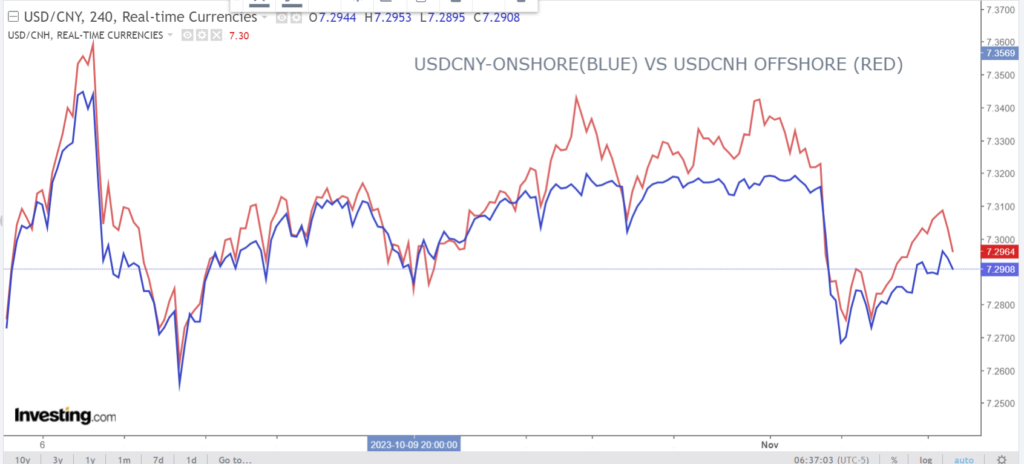

China Snapshot

PBoC fix: today 7.1769, expected 7.2889, previous 7.1771.

Shanghai Shenzhen CSI 300 fell 0.20% to 3579.41.

Chart: USDCNY (onshore) vs USDCNH (offshore) 3 months

Source: Investing.com