June 20, 2024

- Swiss National Bank (SNB) cuts rates by 25 bps to 1.25%.

- Bank of England leaves rates unchanged.

- US dollar mostly from close, mixed form yesterday.

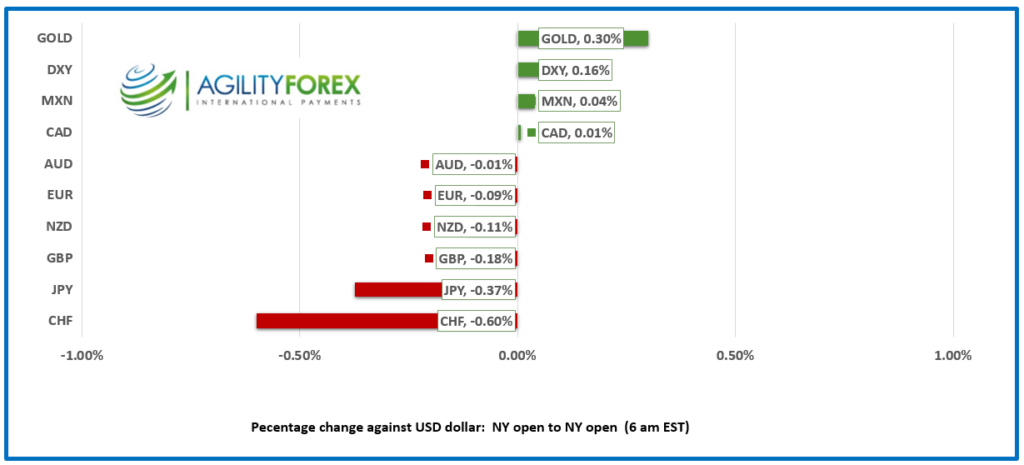

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3716, overnight range 1.3699-1.3721, close 1.3719

USDCAD traded sideways with a modestly bearish bias overnight in a rather quiet overnight session.

The Bank of Canada Summary of Deliberations proved to be a non-event for traders. The Summary noted that officials considered delaying a rate cut until July. If so, it would not have helped Governor Till Macklem’s credibility which is already in shambles due to wrong forecasts. Mr Macklem pretty much pre-announced a July move after the May meeting and he would have been hard pressed to change his mind. Policymakers decided to act because “While they recognized the risk that progress could stall – as it had in the United States – there was consensus that with four consecutive months of easing in core inflation and indicators suggesting continued downward momentum, there had been sufficient progress to warrant a first cut in the policy rate.” That sounds like the 2022 definition of transitory.

WTI oil prices are firm and trading in a 80.41-81.18 range supported by forecast for another drop in US crude inventories.

USDCAD Technicals

The intraday technicals are bearish below 1.3750 and looking for a break below minor support at 1.3690-1.3700 to extend losses to 1.3660. A move above 1.3750 negates the downtrend.

Longer term, the 1.3580-1.350 range continues to contain price action with a minor week-long downtrend guiding prices toward support in the 1.3690 zone.

For today, USDCAD support is in the 1.3680 and 1.3660. Resistance is at 1.3740 and 1.3780. Today’s range is 1.3680-1.3740

Chart: USDCAD daily

Source: DailyFX

Cruel Summer

Summer officially arrives in Toronto at 4:50 pm EDT and US dollar bears may be singing along to Taylor Swift’s most popular song on Spotify (streamed 2,207,318,786). Traders are hoping that the Fed cuts interest rates at a much faster pace than currently projected at last week’s FOMC meeting, which would ease US and G-7 interest rate differentials and drive the US dollar lower. That’s not happening. The US economy continues to grow faster than expected while inflation is sticky.

Today’s US economic reports were mixed. Initial jobless claims fell by 5,000 to 238,00 but the previous week’s result was revised higher. The Philadelphia Manufacturing Survey was mixed and housing starts fell by 1.27 million in May. FX markets barely budged on the news.

Wall Street Rally Relentless

Tech stocks are driving Wall Street indexes to record highs as traders bet that Fed achieves a soft landing. However, Asian equity traders took a breather and Japan’s Nikkei and Australia’s ASX 200 indices closed around flat. Chinese markets continued to slide. European bourses are higher, buoyed by the SNB rate cut with the German DAX up 0.50%. S&P 500 futures are perky and up 0.42%. The US 10-year yield is at 4.248% compared to Tuesday’s closing level of 4.216%.

EURUSD

EURUSD shuffled in a 1.0713-1.074 band in subdued trading due to concerns surrounding the outcome of the French election and from the EU Commission announcing the start of Excessive Deficit Procedures for France and Italy. Elsewhere the Swiss National bank cut its benchmark rate to 1.25% from 1.50% due to reduced inflation pressures.

GBPUSD

GBPUSD is trading defensively and is at the bottom of its 1.2678-1.2725 range with the low occurring following the Bank of England rate announcement. The BoE opted to leave rates unchanged as was widely expected but like last time, the decision was not unanimous. Policymakers Dave Ramsden and Swati Dhingra wanted to cut rates. Governor Bailey said he was pleased that inflation had returned to the 2.0% target, but he needed to be sure it would stay low. A key reason for the leaving monetary policy unchanged was that the BoE wanted to avoid influencing the July 4 election.

USDJPY

USDJPY is at the to of its overnight 157.93 0-158.51 range due to the US 10-year Treasury yield climbing to 4.261% from 4.217% at Tuesday’s close. USDJPY resistance has been weakened by reduced yen purchases from Japanese Life companies. Bloomberg reported that Life Co’s reduced their hedge ratios to the lowest level since 2011.

AUDUSD and NZDUSD

AUDUSD retreated from an overnight peak of 0.6680 to 0.6661 after this mornings US data supported the Fed’s view of just one rate cut in 2024 rather than the market which is pricing 2 rate cuts. AUDUSD support from the slightly bullish comments by RBA Governor Michele Bullock about rate hike risks, have faded.

NZDUSD traded choppily in a 0.6123-0.6148 range with the peak seen after the release of Q1 GDP. The NZ economy grew faster than expected in Q1 (0.3% y/y vs forecast 0.2% and 0.2% q/q forecast 0%). The positive sentiment from the result was fleeting due to broad US dollar strength.

USDMXN

USDMXN traded lower in a 18.3931-18.4655 range as fall-out from the recent election fades and traders refocus on Mexico and US interest rate differentials which make the peso look attractive to carry-traders.

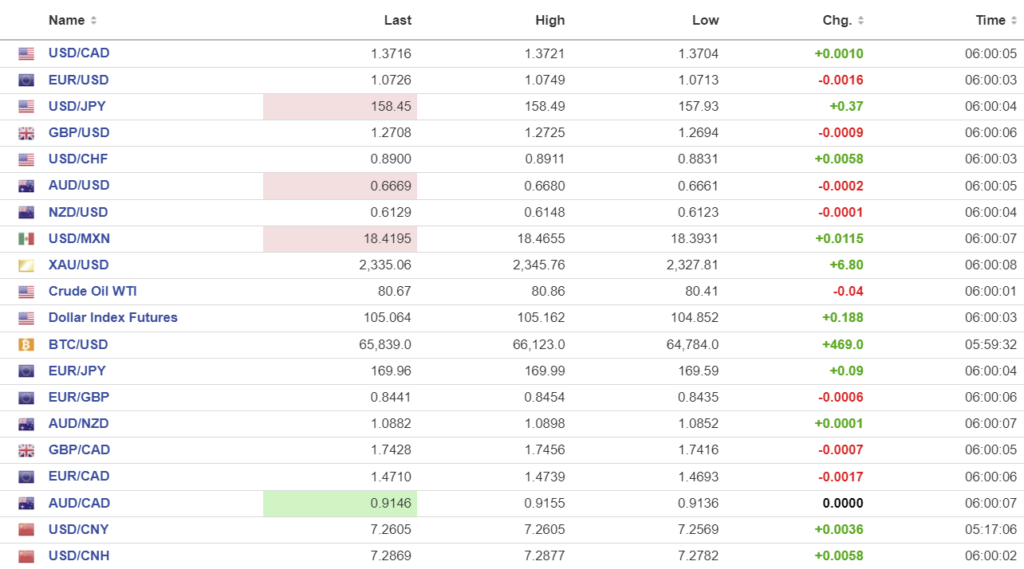

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1192 vs exp. 7.2653 (prev. 7.1159)

Shanghai Shenzhen CSI 300 fell 0.72% to 3503.28.

PBoC leaves interest rates unchanged. The one-year LPR is 3.45% and the over-five-year LPR is 3.95%. One shore yuan was little changed but offshore USDCNH climbed to its highest level this year on fears of unchanged US rates for longer.

Chart: USDCNY and USDCNH

Source: Investing.com