June 24, 2024

- BoC Governor Macklem speaking in Winnipeg.

- German Ifo data shows a struggling economy.

- US dollar opens lower compared to Friday’s close.

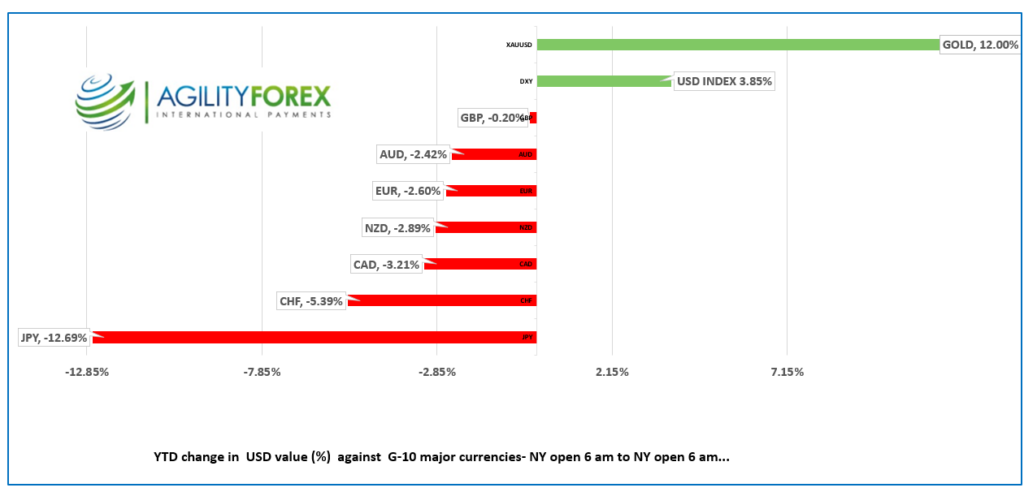

FX at a Glance-Year-To-Date

Source: IFXA/RP

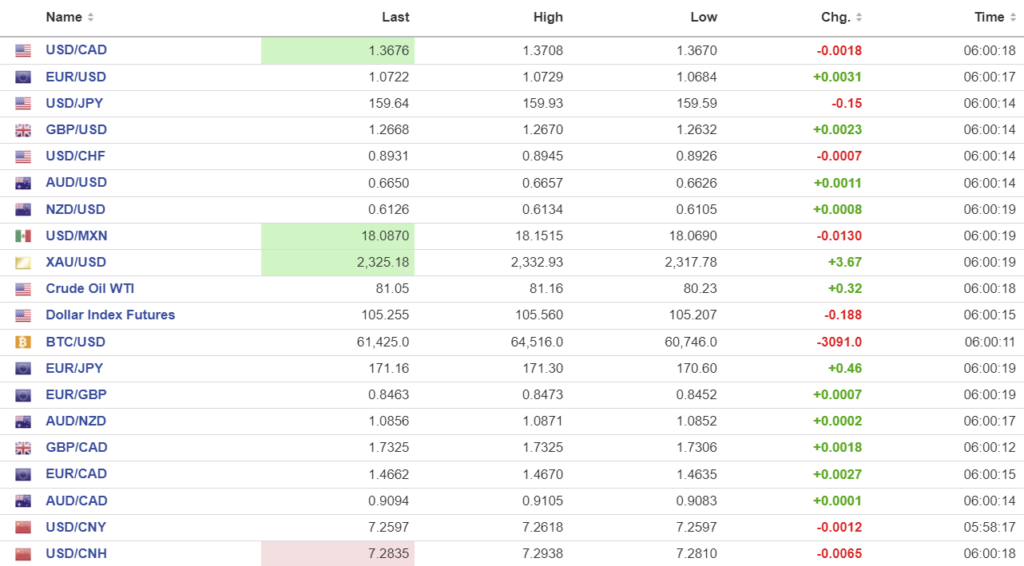

USDCAD open 1.3676, overnight range 1.3670-1.3708, close 1.3694

USDCAD is tracking broad US dollar sentiment (as usual) and has managed to give back all of Friday’s gains overnight. The US and Canadian economic calendar’s are empty today, but Canadian inflation data is on tap tomorrow. Friday is month, quarter and half-year end for portfolio managers which suggests increased FX volatility as the day approaches.

Bank of Canada Governor Tiff Macklem’s speech in Winnipeg at 11:45 am PDT today is titled “Workers, jobs, growth and inflation—Today and tomorrow.”

WTI oil prices ticked lower overnight, falling from 81.16 to 80.23 before climbing back to 80.97 in NY, after Iran denied cutting its Official Selling Price for crude to Asia customers. Prices are supported by increased missile attacks on Red Sea shipping by Yemen’s Houthi rebels.

USDCAD Technicals

The intraday technicals are bearish below 1.3720 and looking for a break below 1.3660 to extend losses to 1.3610. A move above 1.3620 shifts the target to 1.3790.

The USDCAD uptrend from the beginning of the year continues to contain downside moves while prices are above the 1.3630-1.3640 zone. That uptrend line resides just above congestion from 100-daay and 200-day moving averages at 1.3617 and 1.3583 respectively.

For today, USDCAD support is in the 1.3660nd 1.3620. Resistance is at 1.3720 and 1.3760. Today’s range is 1.3650-1.3720.

Chart: USDCAD 4 hour

Source: Investing.com

Greenback on Track to end H1 with Robust Gains.

The US dollar is heading into the end of the first half of 2024 with gains across the board. Divergent Fed and Bank of Japan interest rate outlooks drove JPY to a 12.7% loss, YTD, and that is despite the BoJ spending over $62 billion to slow the losses. The Swiss franc and Canadian dollar were the next two worst-performing currencies, losing 5.4% and 3.2%, respectively because the SNB and BoC cut rates.

Action-Packed Week in Store

The last week of June is packed with data, events, and geopolitical risk. Friday brings the key US PCE price index report, reportedly the Fed’s favorite measure of inflation. That’s followed by the French election on June 30, and Marine LePen’s National party is leading. Recent polls show that French citizens have the most confidence in Ms. Le Pen to steer the economy.

War Drums Pounding

Israel has Hezbollah on its mind. The IDF is close to its goal of eradicating Hamas and is turning its attention to Lebanon. Russia is extremely irked because shrapnel from US-provided weapons killed sunbathing Russian tourists on a beach in Crimea. Meanwhile, peace-loving China continues to harass nations that dispute its claim to the South China Seas.

EURUSD

EURUSD is a tad firmer, rising from 1.0684 to 1.0736 in NY despite another poor German Ifo report. June Business Climate was 88.6 (forecast 89.7, previous 89.3), Current Assessment 88.3 (forecast 88.4, previous 88.3) and Expectations 89 (forecast 91, previous 90.4).

GBPUSD

GBPUSD traded in a 1.2632-1.2672 range overnight and is at the top of that band in NY. Last week’s dovish Bank of England outlook continues to weigh on prices. The UK election is likely a non-event for sterling, but GBPUSD can see volatility from the French elections which may roil EURGBP. GBPUSD technicals are bearish below 1.2700.

USDJPY

USDJPY is reversing its Asia gains and has dropped from an overnight peak of 159.83 to 151.81 then rebounded to 159.51 in NY. The BoJ Summary of Opinions offered the usual “rates will rise if inflation rises as projected” while policymakers repeated that they are watching FX moves closely.

AUDUSD and NZDUSD

AUDUSD traded higher, rising from 0.6626 to 0.6657 in tandem with a weaker US dollar vs. the majors. Consumer confidence data is released Tuesday followed by the May inflation report. The currency pair is underpinned by contrasting central bank outlooks. The RBA is expected to be on hold until 2025 while the odds for a Fed rate cut in September have increased to 65%.

NZDUSD rallied from 0.6105 to 0.6135, mirroring Aussie moves with prices supported by NZDJPY demand. New Zealand’s trade deficit narrowed slightly to -$10.05B from -$10.22B.

USDMXN

USDMXN traded in a 18.0690-18.1515 range, then dropped to 18.0164 after the first half-month inflation data. Headline rose 0.21% (forecast 0.13% and previous -0.21% while Core rose 0.17% from 0.15% previously. USDMXN rebounded quickly and is trading at 18.0767 in NY.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

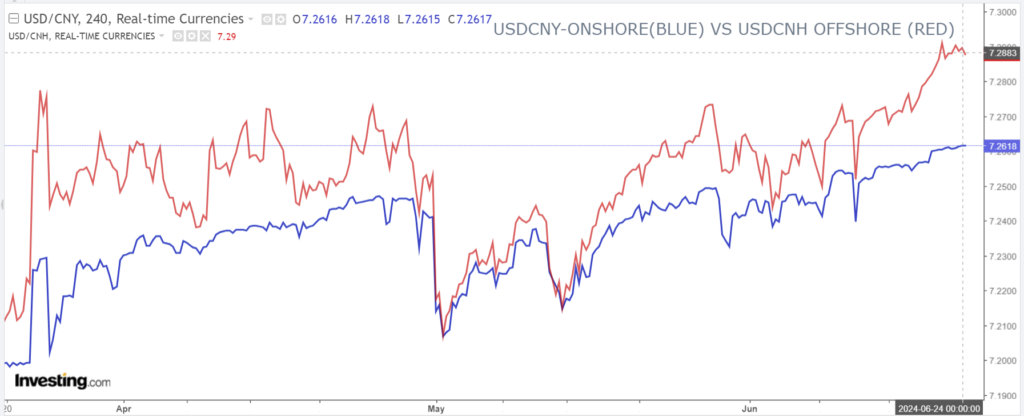

China Snapshot

PBoC fix: 7.1201 vs exp. 7.2647 (prev. 7.1196).

Shanghai Shenzhen CSI 300 fell 0.54% to 3476.81.

Chart: USDCNY and USDCNH

Source: Investing.com