July 15, 2024

- President Trump-the Sequel Inevitable.

- Fed Chair Powell speaks at 12:30 pm EDT.

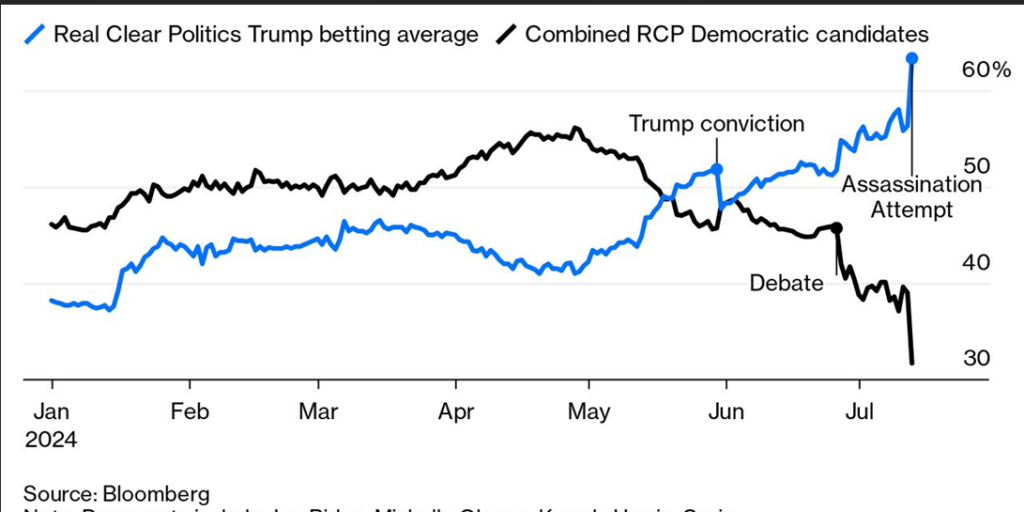

- US dollar sinks as Trump’s presidential odds rise.

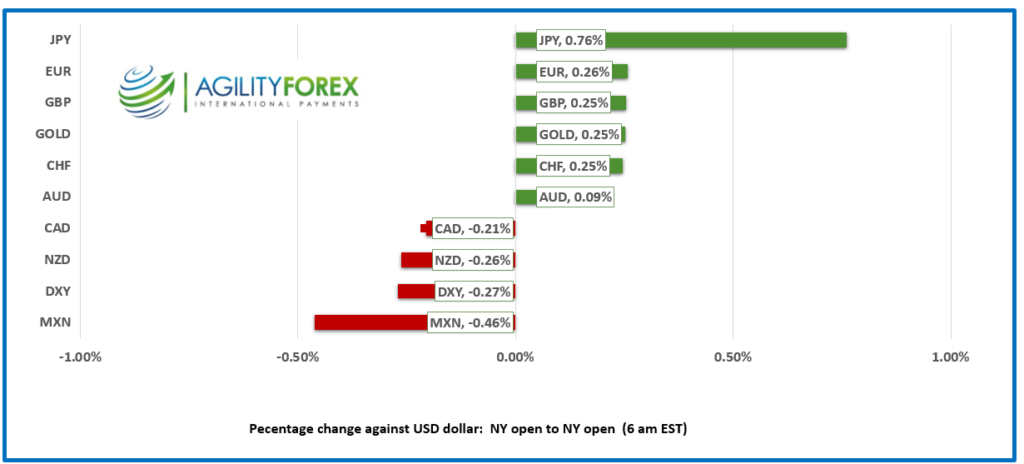

FX at a Glance

Source: IFXA/RP

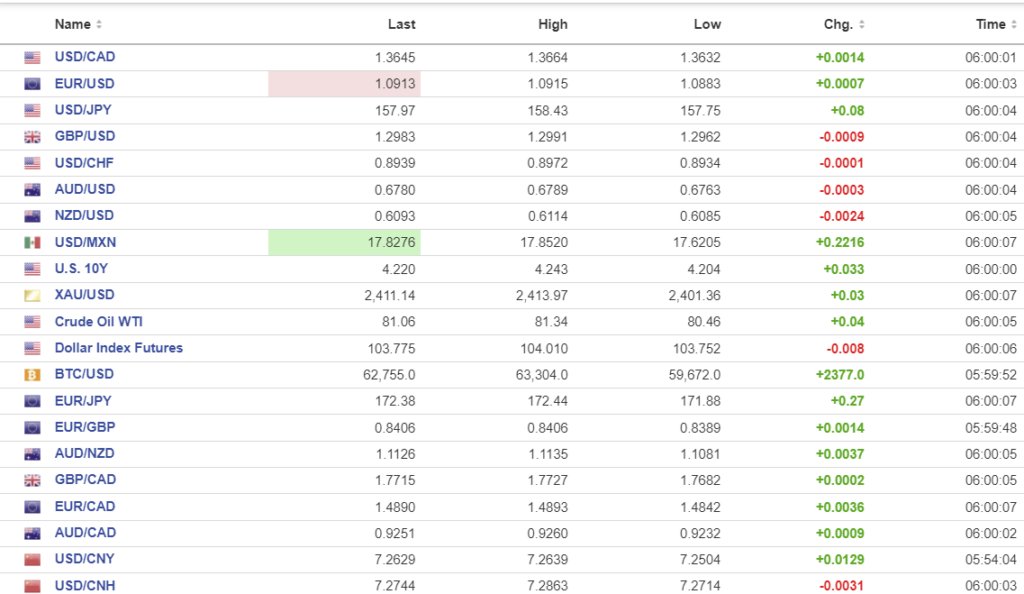

USDCAD open 1.3645, overnight range 1.3636-1.3664, previous close 1.3639

USDCAD is starting the week on a defensive note, in part because Donald Trump’s dislike of Justin Trudeau may translate into renewed trade sanctions when Trump returns to the White House.

It is a big week for Canadian data beginning with today’s release of the Bank of Canada’s Business Outlook Survey (BOS), followed by the June inflation data on Tuesday. Traders will be paying close attention to the inflation expectations component in the BOS. Even so, Tuesday’s BOC Core CPI measures are what count.

WTI oil retreated from 82.34 at the end of day on Friday to 80.46 overnight as the combination of soft Chinese data and Trump’s improved re-election prospects weighed on prices.

USDCAD Technicals

USDCAD technicals are neutral inside a 1.3590-1.3660 range with a modest bearish bias due to elevated short USDCAD positioning.

The longer term technicals are unchanged. The mid-April downtrend remains intact while below 1.3730 but there is plenty of support in the 1.3590 and 1.3540-60 area.

For today USDCAD support is at 1.3610 and 1.3590. Resistance is at 1.3660 and 1.3690. Today’s range is 1.3610-1.3680

Chart: USDCAD Daily

Source: DailyFX

“Why Didn’t My Campaign Think of That?”

It can’t be that easy, can it? That path to the White House is simply the trajectory of a .223 Remmington calibre round fired from an AR style rifle. A convicted felon, a businessman who made a fortune while bankrupting 6 companies between 1991 and 2009, and a man found liable for sexual abuse and defamation is the odds-on favourite to win the 2024 US election because of a 20-year kid with a lousy aim.

Source: John Arthurs Bloomberg

Clouds and Silver Linings

Thomas Matthew Crooks had a bad day seconds after he attempted to assassinate Donald Trump, but the same cannot be said for US dollar bears and Wall Street Bulls. The US dollar rallied initially but then gave back all the gains by the time NY markets opened, and S&P 500 futures rallied 0.41% as traders anticipate another four years of tax cuts, deregulation, infrastructure spending, and improved economic growth.

The news helped the Australian ASX 200 gain 0.73% despite disappointing Chinese data. Japanese markets were closed for the Marine Day holiday. European bourses are in the red due to caution ahead of German ZEW data on Tuesday and Thursday’s ECB meeting. The US 10-year Treasury yield climbed from 4.186% at Friday’s close to 4.241% before easing to 4.225% in early NY trading.

“Can We Talk?”

Fed Chair Powell and San Francisco Fed President Mary Daly headline are the star attractions in an otherwise dull US data day. Friday’s US PPI data was hotter than expected, but according to Bank of America economists, the components that impact the PCE report were softer. Meanwhile, the University of Michigan Survey indicated weak consumer sentiment. Those data points may help put a rosier bias to Powell’s interest rate outlook.

EURUSD

EURUSD traded in a 1.0883-1.0920 range with the bottom seen in early Asia trading. Today’s focus will be on the 10:00 am NY option expiry window when $6.2 billion of 1.0895-1.0900 strikes mature with another $3.8 billion of 1.0910-30 strikes rolling off as well. Thursday’s ECB meeting is expected to be rather tame.

GBPUSD

GBPUSD traded in a 1.2962-1.2991 range against a backdrop of uncontrolled sobbing after another Euro Cup final loss. The game was a mirror of the UK election. The Three Lions played conservatively while Spain played the role of Labour.

USDJPY

USDJPY was steady in a 157.75-158.43 range with Japanese markets closed for a holiday. Higher US Treasury yields underpinned prices but the fear of BoJ intervention limited gains.

AUDUSD and NZDUSD

AUDUSD traded in a 0.6763-0.6789 range in quiet trading with US dollar selling pressure offset by soft Chinese economic growth data. NZDUSD traded in a 0.6085-0.6114 range with gains hampered by soft Business Services data.

USDMXN

USDMXN rallied from 17.6205 to 17.8520 after the steep rise in Donald Trump’s re-election odds. Mr. Trump is not known for being a fan of Mexico thanks to his penchant for tariffs and demand for Mexico to pay for a wall between the two countries.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1315 vs exp. 7.2514 (prev. 7.1339)

Shanghai Shenzhen CSI 300 rose 0.11% to 3476.25.

Q2 GDP 4.70% y/y (forecast 5.1%, previous 5.3%, June Industrial Production5.3% (forecast 5.0%, previous 5.6%),June Retail Sales 2.0% y/y (forecast 3.3%, May 3.7%).

PBoC left 1-year Medium-Term Lending Facility (MLF) unchanged at 2.5%, as expected.

Chart: USDCNY and USDCNH

Source: Investing.com