By Michael O’Neill

Things are looking up for Canadians because interest rates are going down. The Bank of Canada cut its benchmark rate by 25 bps to 4.5% as was widely expected. Governor Tiff Macklem announced emphatically that “further rate cuts are coming,” mainly due to significant supply in the economy which is driving inflation down. He said that significant slack was a big part of today’s decision to trim rates.

When asked if rates would drop to 3.75% by year-end, Macklem dodged the question with the finesse of Elaine Benes in Seinfeld’s “The Little Kicks” episode. The short answer is “probably.” The long answer: “we will make decisions one meeting at a time.” That’s drivel masquerading as insight. Of course, they will make decisions one meeting at a time; otherwise, there’d be no need for meetings.

Monetary Policy Report Tea Leaves

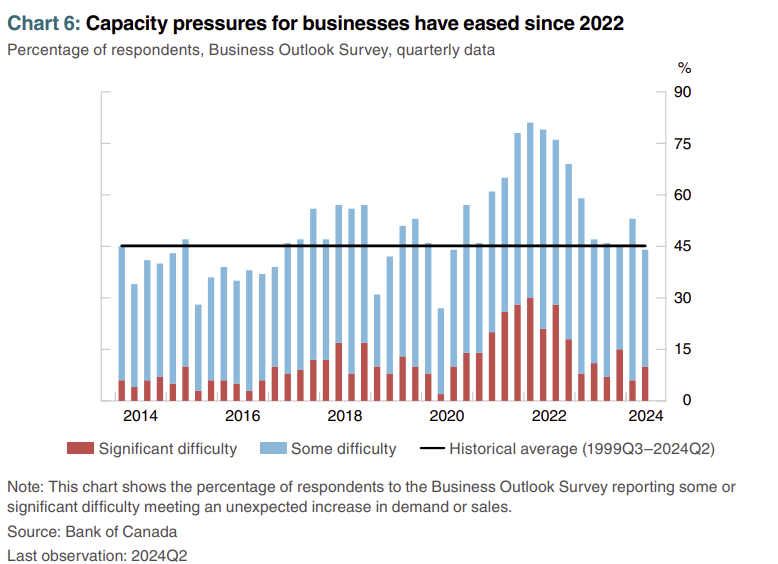

As usual, the MPR is replete with pretty charts and graphs, and for this report, the most important pictorial is the one showing excess supply. That’s because Macklem cited excess supply, as the key justification for cutting rates. It is also a measure that is extremely hard to quantify which gives policymakers lots of wiggle room.

Excess capacity involves constantly evolving economic conditions, making it an extremely fluid measure. Many indicators that measure capacity are lagging indicators, not current ones, increasing the risk of inaccurate real-time measurements. Additionally, the BoC has previously blamed forecasting errors on poor models, and many key variables used to estimate excess supply are mere guesses.

Source: BoC MPR

Breathing Easy

The BoC is in rate-cutting mode, and barring any nasty economic or geopolitical surprises, rates are heading lower. It isn’t a stretch to believe the overnight rate will be 4.00% by year-end, as many economists have already predicted, but 3.75% is not out of the question.

Rate Cut Rationale

One of the key reasons is that the BoC doesn’t really have a lot of choices. Canadian homeowners have $400 billion in mortgages renewing in 2025 and another $1.0 trillion renewing in 2026. Many of them were new homebuyers paying top dollar for scarce housing. Tiff Macklem encouraged them. In November 2020, he told the House of Commons Standing Committee on Finance that borrowing costs would remain “very low for a long time.” He specifically mentioned that the Bank of Canada expected the policy interest rate to stay at its effective lower bound of 0.25% until economic slack is absorbed and the 2% inflation target is sustainably achieved. This projection extended into 2023, based on the Bank’s outlook at the time.

Failing to act and cut rates could have devastating consequences for the domestic economy and re-election prospects for many, if not all, Members of Parliament.

The Monetary Policy Report is to economists what a celebrity scandal is to the internet. The rest of the country just wants to know where interest rates and the Canadian dollar are going.

Plucking the Loonie’s Feathers

Falling interest rates won’t do the Canadian dollar any favours, especially if they drop further than US interest rates, although that relationship is imperfect. Generally, foreign investment flows into G-10 countries with higher yields. The current CAD/US interest rate spread is 100 bps (as of July 14 – BoC overnight rate 4.5%, Fed Funds 5.50%). In days of yore, the Canadian dollar was viewed as a petro-currency and would attract energy investment flows, acting as a cushion if Canadian interest rates were lower than the US. But that well has blown. Canada’s Environment Minister Steven Guilbeault and Prime Minister Trudeau have seen to that.

“It’s the Economy, Stupid”

The economy is another issue. Macklem is cutting rates because the economy is sluggish. Meanwhile, the Fed is expected to cut rates in September, and the US economy remains robust. Canada’s uncontrolled immigration is driving the rental market to its breaking point and overburdening an already strained health system, making a mockery of the BoC’s forecast for 2.25% GDP growth in 2025. The Canadian dollar used to benefit from being America’s largest trading partner, but that advantage has eroded, partly because Mexico has usurped Canada’s position.

The Loonie as a Global Citizen

The Canadian dollar is only a minor currency in the world of global Foreign Exchange despite being the seventh most active currency. The devil is in the details. The Canadian Foreign Exchange Committee released its April 24 FX volume survey. The monthly Canadian dollar turnover of spot, forwards, and swaps totaled about $3.9 trillion or $178.3 billion per day. When your favourite bank clips you just 0.0001 on your USDCAD transaction, you are contributing to the roughly $17.8 million of daily profit generated by the global banking fraternity.

More importantly, the US dollar is on one side of 88% of all the daily FX turnover which in April 2022 amounted to $7.5 trillion. Knowing that, it is easy to understand why, when the US dollar rises, most times, the rest of the G-10 currencies fall and vice versa.

This relationship may not hold for the Canadian dollar, which may weaken during bouts of US strength and during bouts of US weakness, as greenback issues often prompt a “Sell North America” mindset.

Canadian rates may be heading lower, but it is the Loonie that will be skydiving.