September 6, 2024

- S&P 500 futures recouping Friday’s losses-still a long way to go.

- Harris-Trump debate weighing on risk sentiment.

- US dollar extends Friday’s gains.

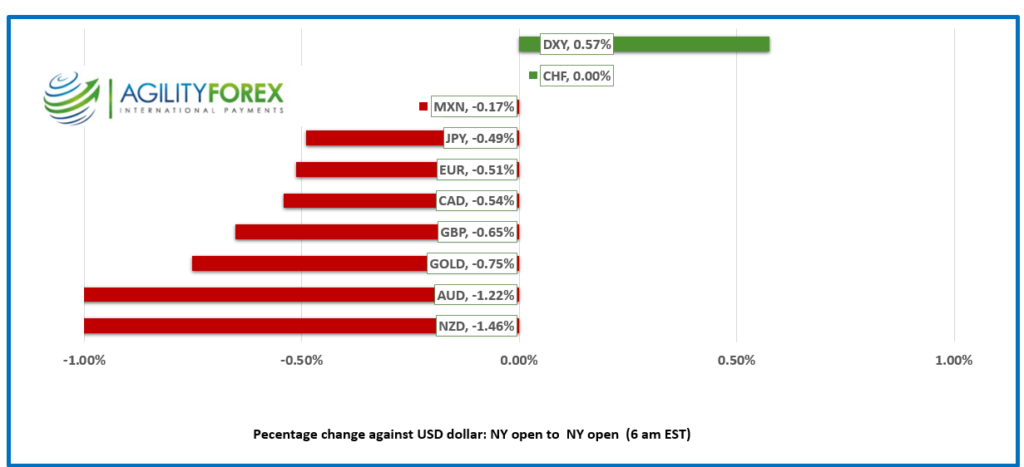

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3566, overnight range 1.3552-1.3573, previous close 1.3575

USDCAD rallied Friday and then consolidated the gains overnight. The Canadian employment data painted a picture of a very sluggish economy with unemployment rising to 6.6%, a level not seen in seven years (excluding the pandemic). Some economists are suggesting that the poor report could lead to the BoC cutting rates by 50 bps in October.

The US Nonfarm payrolls report was also weak, but not nearly as bad as some analysts expected. However, it did lead to a sharp drop in 50 bps rate cut odds at next week’s FOMC meeting.

That shift in sentiment powered the US dollar higher and USDCAD went along for the ride.

Oil prices traded in a 68.03-68.83 range. News that Opec would delay production increases was overshadowed by global economic growth concerns, which were exacerbated byt the weak inflation data from China overnight.

USDCAD technicals

The intraday USDCAD technicals flipped to bullish Friday with the move above 1.3520 and are looking for a break above 1.3590 to extend gains to 1.3650. A decisive break below the 1.3510-20 zone would shift the focus to 1.3450.

The August 27 uptrend remains intact above 1.3490 and Friday’s rally suggests that the drop to 1.3465 was an anomaly.

For today, USDCAD support is at 1.3530 and 1.3500. Resistance is at 1.3590 and 1.3620.

Today’s Range 1.3460

Chart: USDCAD 4 hour

Source: Centralcharts.com

Bluster, Bombast, Inflation and ECB

There is a lot going on this week and traders are approaching it with a degree of caution. Chinese data didn’t help as the latest inflation report underscored the weak economic growth. Overly optimistic traders are still licking their wounds after Friday’s US employment picture failed to live up to its pre-release hype and the odds for a 50bp Fed rate cut shrank to 25%. Traders will stay close to home at least until Wednesday’s US inflation data is released.

September is the beginning of meteorological fall and blustery winds are a hallmark of the season. They will reach hurricane status Tuesday night when Donny Trump debates Kamala Harris. It’s “must-watch” TV because if Trump fails in his presidential bid, he plans to revive the 2010 William Shatner sitcom “$#*! My Dad Says” and rename it “$#*! My Former President Says.”

Still Hopeful

Traders often see themselves as Alladin and the Fed as a genie, believing that their wishes are the Fed’s command. That describes the ongoing talk about 50 bp Fed rate cuts despite policymakers suggesting rate cuts would be gradual. The proof is in the equity market performance. Wall Street closed deep under water on Friday led by a 2.55% plunge in the Nasdaq. Asian markets fell as well but not nearly as sharply. Japan’s Topix lost 0.68%, the Hang Seng Index fell 1.42% and Australia’s ASX 200 dropped 0.32%. European traders are more positive and all the major indexes are in the green, led by a 0.76% rally in the UK FTSE 100. S&P 500 futures are climbing and have risen 0.72% today. The 10-year Treasury yield is steady at 3.75%.

EURUSD

EURUSD is trading defensively. The single currency peak at 1.1156 Friday and then dropped to 1.1064. It consolidated those losses in a 1.1037-1.1092 range overnight sits at the bottom of that band in NY. Mario Draghi’s report on EU competitiveness was a bit of a downer. Mr Draghi said, “For the first time since the Cold War we must genuinely fear for our self-preservation.” The report highlighted EU economic growth that persistently lagged that of the US over 20 years.

GBPUSD

GBPUSD is trading negatively in a 1.3073-1.3144 range with traders looking ahead to the UK employment report tomorrow. The data is unlikely to spark at BoE rate cut in September, but if it is weaker than expected, the prospect of an October rate cut could provide GBPUSD with some support.

USDJPY

USDJPY caught a bid and recouped all of Friday’s losses, rising from 141.96 to 143.78. the rally was fueled by downward revisions to economic growth Q2 GDP rise 0.7% q/q compared to 0.8% previously and 2.9% y/y compared to 3.1%. Those results may encourage the BoJ to rethink its rate hike plans.

AUDUSD and NZDUSD

AUDUSD is consolidating Friday’s losses in a 0.6647-0.6689 range due to both weak Chinese data and the hangover from Friday’s US employment report. NZDUSD traded in a similar fashion in a 0.6125-0.6187 range.

USDMXN

USDMXN traded in a 19.9018-20.0140 range and is at the bottom of that band in early NY trading. Mexican inflation drifted lower (actual 0.01%, forecast 0.9% m/m, Core inflation (actual; 0.22, forecast 0.23% m/m). Consumer confidence ticked higher rising, to 47.6 from 46.9. Mexican politics helped fuel the rally and concerns about fresh “Mexico bashing” when Trump debates Vice President Kamala Harris tomorrow. The USDMXN technicals are bullish in a 19.8230-20.5350 channel.

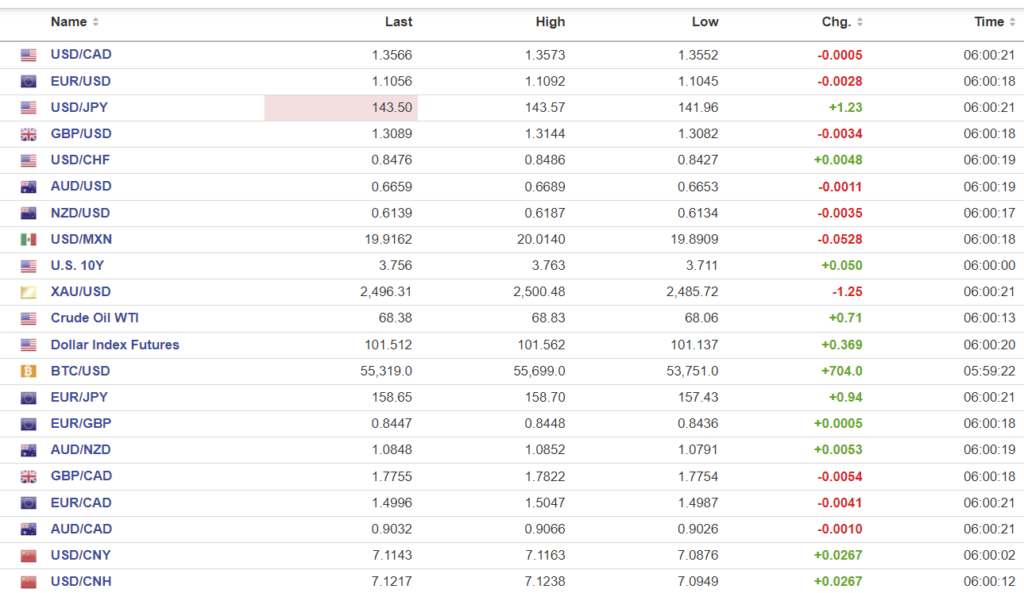

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.0989 (prev. 7.0925)

Shanghai Shenzhen CSI 300 fell 1.19% to 3192.95.

Deflation concerns continue. August CPI rose 0.4% m/m (forecast 0.5%, previously 0.5%) and 0.6% y/y (forecast 0.7%). PPI fell 1.8% y/y, forecast -1.4%).

Chart: USDCNY and USDCNH

Source: Investing.com