By Michael O’Neill

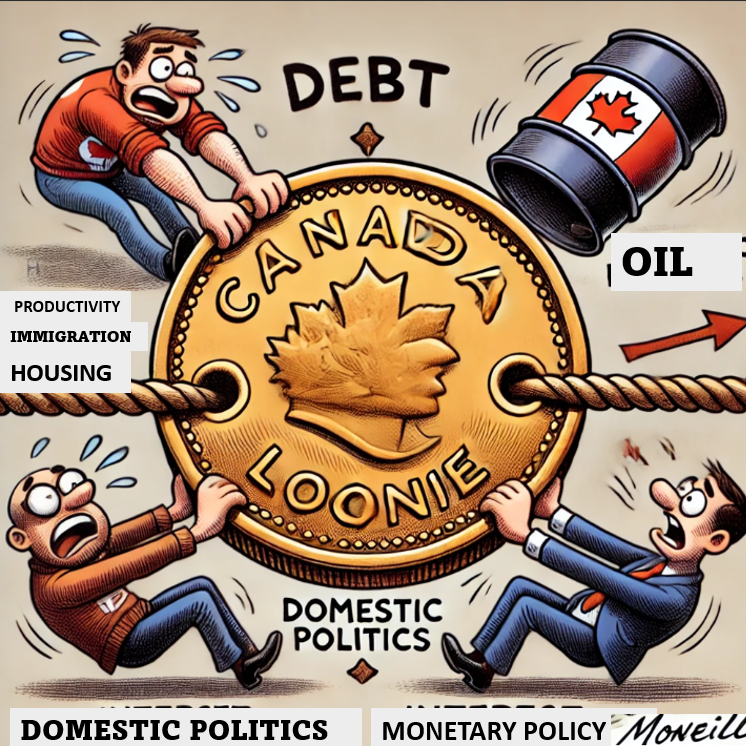

The Canadian dollar is living on a prayer, ensnared in a web of competing forces that are steadily eroding its buying power.

FOMC in the Driver’s Seat

At the forefront of this struggle is the size and pace of the upcoming Federal Open Market Committee (FOMC) interest rate cuts. Traders had worked themselves into a frenzy, expecting August inflation data to have cooled more than anticipated, giving the Fed an excuse to cut rates by 50 bps next week. Alas, it didn’t pan out. The CPI increased by 0.2% m/m, unchanged from July, with details—especially services and housing components—showing unexpected firmness. This uptick in core CPI to 0.3% from 0.2% suggests the Fed will likely opt for a modest 25 bps cut instead. Yet, hopes for a 50 bps cut haven’t vanished—they’ve just been deferred to the November 7 meeting.

The Canadian dollar sank due to the prospect of narrowing CAD/US 2-year and 10-year bond yield spreads but the move didn’t last.

Canadian Recession Risks are a Reality

Economist David Rosenberg recently pointed out in the Financial Post that Canada is staring down a consumer debt crisis. Household debt-to-income sits at a staggering 177%, nearly 40% above historical peaks and the levels seen during the 2007 US credit bubble. On average, Canadians are allocating 15 cents of every dollar earned just to service debt. Picture a family of four in Vancouver with a combined income of $140,000 per year. They’d pay around $50,801 in taxes—federal, provincial, municipal, and GST—followed by another $21,000 in after-tax dollars to service their debt, leaving just $68,000 for everything else. That is, until a layoff hits.

Canada’s unemployment rate stands at 6.6%, but for new job-seekers, it’s effectively 50%. The labor market can’t keep up with the influx of new immigrants, and the only sector showing growth is the public sector. Rising unemployment leads to weaker consumer spending, exacerbating economic contraction and nudging the economy deeper into recession.

Political Dysfunction

Smug Canadian’s often ridicule the USA because of its intense political dynamics but since 2016, Canadian politics have become increasingly polarized. Justin Trudeau and Steven Guilbeault’s policies have increasingly alienated many Canadians, contributing to a significant decline in support for the Liberal government. Trudeau’s perceived disconnect from middle-class struggles, combined with controversial carbon tax hikes and energy policies championed by Guilbeault, have hit the pocketbooks of many, particularly in oil-dependent provinces. Their aggressive climate agenda, while appealing to some, is seen by many as out-of-touch with the economic realities of ordinary Canadians.

The Liberals were dealt a blow in the 2021 election, left with a minority government that wouldn’t have survived six months if Jagmeet Singh hadn’t entered into a supply and confidence agreement, effectively propping them up. That arrangement, which essentially granted Trudeau a de facto majority, ended in divorce on September 4. But despite the split, don’t expect much to change. Singh is eyeing a $2.5 million golden handshake if he hangs on until February 2025. and Trudeau—while not driven by monetary concerns—has little incentive to call an election given the dim career prospects awaiting a former drama teacher.

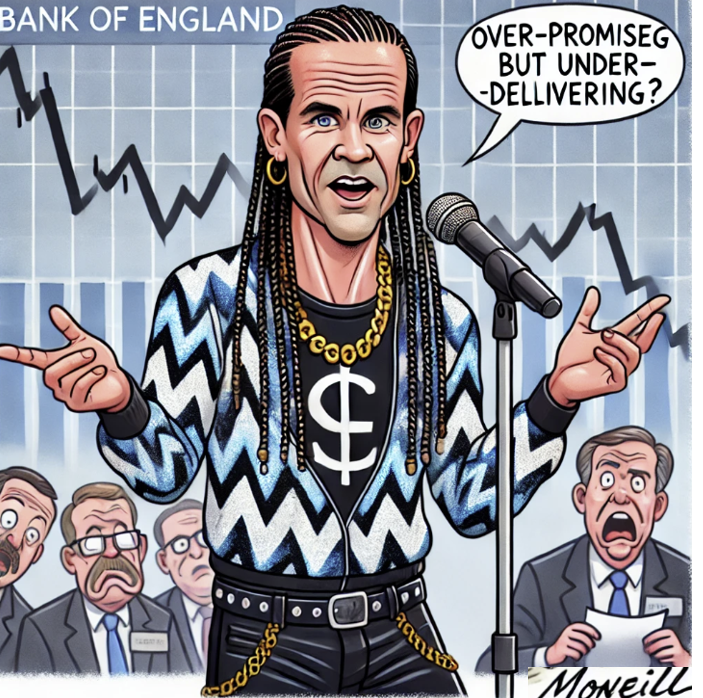

The ”Rock Star” is Really Milli Vanilli

Liberal backbenchers see the writing on the wall. For many, being a Member of Parliament is the highest-paying job they’ll ever land, and they’re not going down without a fight. As a result, some are actively courting Mark Carney, former Goldman Sachs Managing Director and ex-governor of both the Bank of Canada (BoC) and the Bank of England, as a potential savior.

Carney was praised for his leadership of the BoC during the global financial crisis, largely because Canadian banks fared far better than their US counterparts. But the credit belongs to former Finance Minister and Prime Minister Paul Martin, who vetoed bank mergers and kept Canada’s conservative banking structure intact. Carney’s role in shielding Canadian banks from global financial collapse was, at best, minimal. As Governor of the Bank of England, his inconsistent forward guidance, missed inflation targets, and sluggish economic results earned him low marks, leaving many markets frustrated with his leadership

.Racing in Reverse.

Canada’s productivity problem poses serious risks to its economic future. The Bank of Canada warned about this last March, and the situation hasn’t improved. Weak productivity hampers business growth, stifles wage increases, curtails innovation, and erodes global competitiveness. This leaves Canada more vulnerable to inflation, as companies are forced to raise prices to cover rising costs without a corresponding increase in output.

The U.S., by comparison, is sprinting ahead, with American workers consistently generating more output per hour than their Canadian counterparts. Without a meaningful push to boost productivity, Canada risks falling further behind, making it even harder to sustain economic growth and improve living standards.

The Canadian economy and Canadian dollar are living on a prayer and sooner or later the world is going to say “Amen.”