September 12, 2024

- ECB cuts rate 25 bps, as expected.

- FOMC tainted by Atlanta Fed Bostic’s lack of credibility.

- US dollar directionless-MXN outperforms.

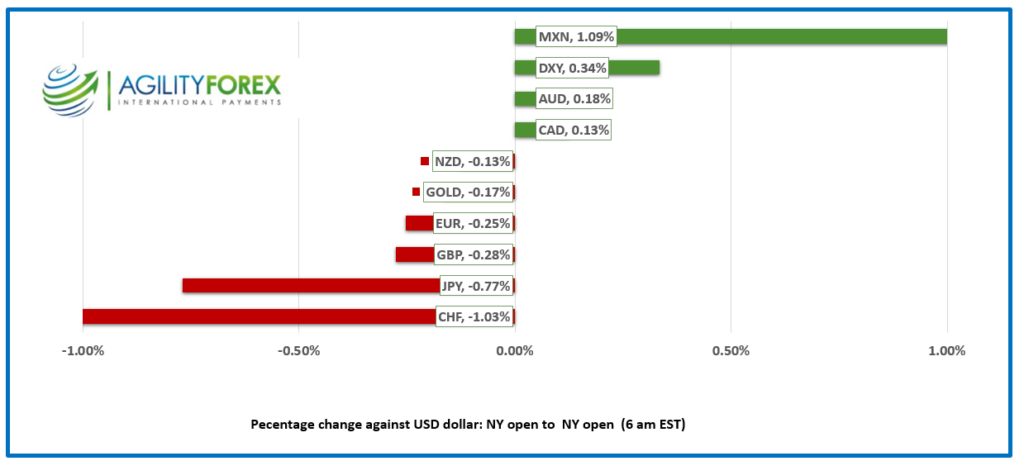

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3571, overnight range 1.3564-1.3586, previous close 1.3578

USDCAD popped following yesterday’s US CPI data and hit 1.3625 before completely reversing the move. Rising US equity markets fueled the sell-off because whether or not the Fed cuts 50 bps at next week’s meeting is irrelevant as long as traders believe policymakers will lower rates by 250 bps by the end of 2025. The CAD/US 10-year spread narrowed which if it continues should limit USDCAD downside.

USDCAD may see a lot of volatility around the 10: am option expiry window if it is near the 1.3590 area which is the strike price of a $1.4 billion opiton that expires.

WTI oil prices are steady in a 67.25-68.66 range. Prices are underpinned in the short term because of Hurricane Francine shutting down a sizeable chunk of Gulf Sea production. However yesterday’s API report of a 0.83 million barrel increase in US crude inventories combined with ongoing concerns about Chinese demand will limit gains.

There are no notable Canadian economic reports today.

USDCAD technicals

The intraday USDCAD technicals are bearish below 1.3610 and looking for a retest of 1.3540. A move above 1.3610 targets 1.3650.

The four hour chart shows a bullish flag pattern suggesting and upside risk to 1.3650, while prices are above 1.3560. A move below 1.3560 suggests further losses to 1.3510, then 1.3460.

For today, USDCAD support is at 1.3560 and 1.3510. Resistance is at 1.3610 and 1.3650.

Today’s Range 1.3530-1.3630

Chart: USDCAD daily

Source: Investing.com

Forward Non-Guidance

The ECB cut rates today by 25 bps to 3.5%, which has been widely expected ever since they cut rates in June. The statement said that “Staff see headline inflation averaging 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, as in the June projections.” The statement warned that inflation will rise in the latter part of the year because previous sharp falls in energy prices drop out.

“We Are Never Ever Getting Back Together”

The Kamala Harris campaign got a major lift from Taylor Swift, a one-woman economic juggernaut who boosted GDP in every country she performed in, when she told her 242 million followers she’d be voting for Harris. Naturally, Ms. Harris was thrilled, but she might want to manage expectations. Swift, who’s on her 12th relationship since 2008, has penned plenty of breakup anthems along the way. Chances are that this political love affair will end with Harris finding out on the radio.

Upcoming Fed Meeting Comes Back in Focus

Yesterday’s US inflation data was enough to lower the odds of a 50 bp rate cut next week to just 15%, after core CPI rose 0.3% m/m. Todays data didn’t change that view. PPI data was mixed-the August index rose 0.2% m/m ( forecast 0.1%) while the year over year result dropped to 1.7% from 1.8. Weekly jobless claims were ho-hum, at 230,000, exactly as predicted.

Tainted Love

The US Supreme Court was always regarded as a bastion of integrity. That changed when Justice Clarence Thomas was found to be taking undisclosed luxury gifts and benefits from a wealthy individual who actually had business in front of the Supreme Court. He suffered no consequences. Yesterday, the Fed’s Office of the Inspector General released a report dated September 4, stating that Atlanta Fed Governor and FOMC voting member Raphael Bostic’s investment manager made 154 trades on behalf of Bostic between March 2018 and March 2023 in violation of the Fed’s blackout rules. He pleaded innocent, saying the trades were unknown to him. Yea, sure. How likely its it that he never looked at his account statements in five years?

EURUSD

EURUSD is in wait-and-see mode, trading in a 1.1005-1.1024 range. The single currency came under pressure when yesterday’s US inflation numbers all but eliminated the risk of a 50-point Fed rate cut.

GBPUSD

GBPUSD drifted in a 1.3032-1.3060 range, with prices weighed down by yesterday’s soft UK data, including GDP, which was flat in July, and weaker Manufacturing and Industrial Production data. Traders are cautious ahead of the ECB and next week’s Fed meeting.

USDJPY

USDJPY traded with a bit of a bid in a 142.24-143.04 range, despite more hawkish comments from Bank of Japan officials. Naoki Tamura stated, “It’s necessary to push up our short-term policy rate at least to around 1%” to sustainably achieve the BOJ’s price goal. However, it was the rebound in the US 10-year Treasury yield from 3.61% yesterday to 3.679% today that underpinned prices.

AUDUSD and NZDUSD

AUDUSD traded higher in a 0.6656-0.6695 range on the back of improved risk sentiment sparked by the big jump in the Nasdaq and S&P 500 yesterday and a 1.10% gain in Australia’s ASX 200. NZDUSD rose from 0.6128 to 0.6159 due to the better risk environment. New Zealand Retail Sales rose 0.2% in August but were down 2.9% y/y.

USDMXN

USDMXN dropped to 19.7187 from 19.8477 due to improved risk sentiment and because traders appeared to be “over” judicial reform concerns. In addition, USDMXN demand from carry trade unwinding has faded. Prices saw additional selling pressure after Citibank analysts suggested “negative sentiment may have peaked.”

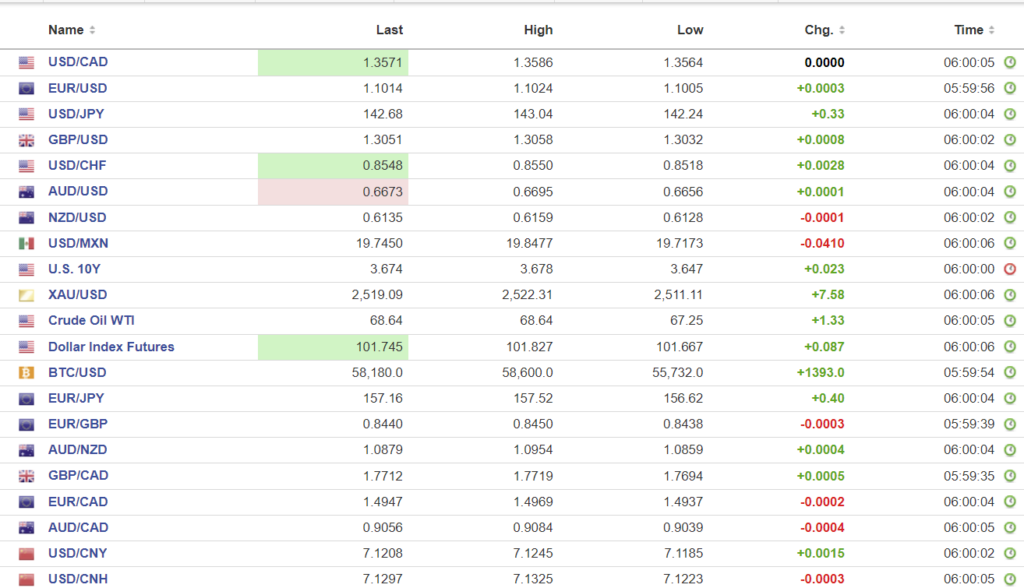

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1214 vs (prev. 7.1182).

Shanghai Shenzhen CSI 300 fell 0.43% to 3172.47

A little know part of President Xi Jinping’s economic strategy is to arrest some bankers and cease the passports of others, because nothing encourages economic growth like eroding confidence in the domestic $1.7 trillion brokerage business.

Chart: USDCNY and USDCNH

Source: Investing.com