September 17, 2024

- Canadian inflation cools more than expected.

- US Retail Sales not as weak as hoped .

- US dollar trades sideways overnight and opens mixed.

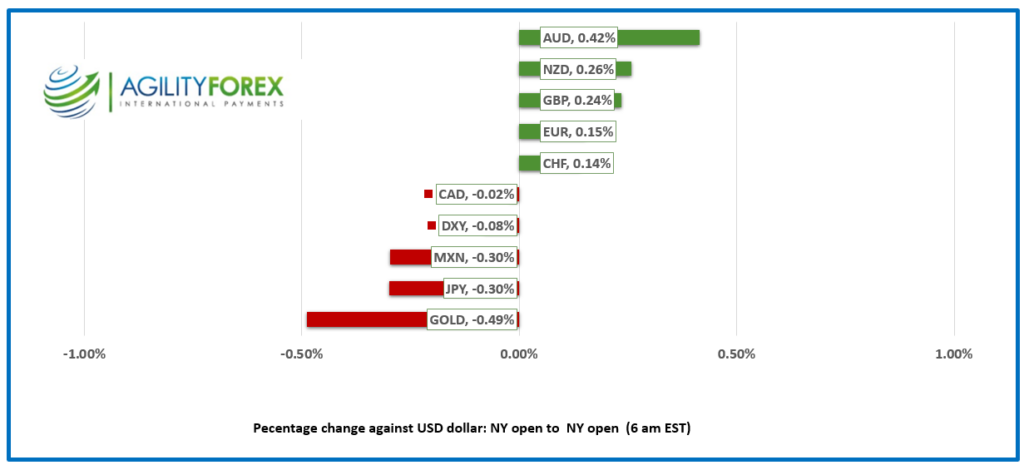

FX at a Glance

Source: IFXA/RP

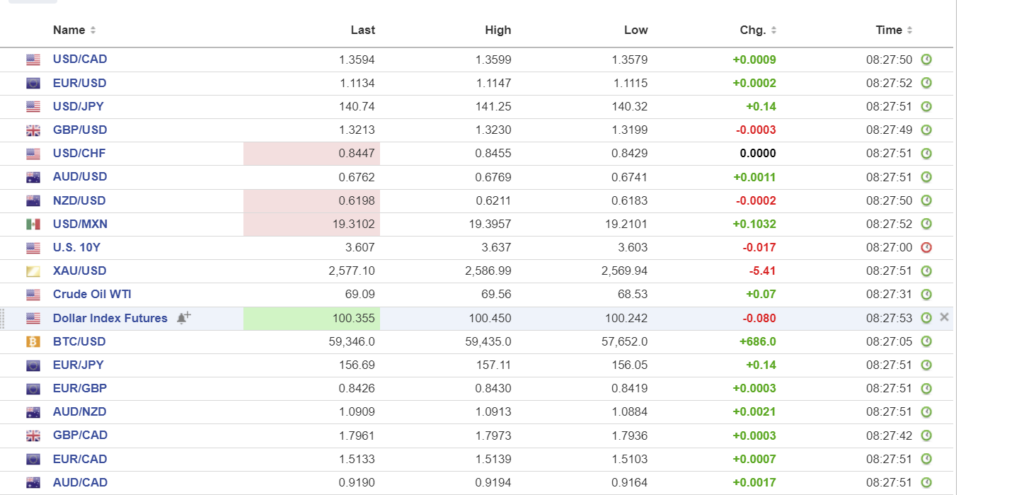

USDCAD open 1.3584, overnight range 1.3579-1.3599, previous close 1.3588

USDCAD popped to 1.3613 from 1.3594 after Canadian inflation cooled far more than anticipated. Statistics Canada wrote: “CPI rose 2.0% on a year-over-year basis in August, increasing at the slowest pace since February 2021, and down from a 2.5% gain in July 2024. Falling gas prices were a major reason for the drop.

Today’s inflation numbers support Bank of Canada Governor Macklem weekend comment that “Trade disruptions may mean larger deviations of inflation from the 2% target.” There is still a lot of data between now and the next monetary policy meeting on October 23 so today’s data is diminished in importance.

The Trudeau Liberals got further evidence that voters believe the are well-past their “best-before-date,” when they lost a Montreal riding to the Bloc-Quebecois. The news was bittersweet for Pierre Poilievre’s conservative party as their candidate on got 11.6% of the vote.

WTI oil prices are trading in a 68.53-69.56 range and supported by the improved risk sentiment tone.

USDCAD technicals

The intraday USDCAD technical are bullish above 1.3560, looking for a break above 1.3630 to extend gains to 1.3690. A move below 1.3560 would extend losses to 1.3520, then 1.3480.

The monthly chart shows USDCAD trapped in a 1.3110-1.3980 range since October 2022 but with an uptrend line from June 2021 guiding prices higher while above 1.3405.

For today, USDCAD support is at 1.3550 and 1.3510. Resistance is at 1.3620 and 1.3650.

Today’s Range 1.3560-1.3640

Chart: USDCAD monthly

Source: Investing.com

Retail Sales In-line with Forecasts

Today’s US Retail Sales did nothing to resolve the 25 or 50 bp rate cut debate. The results failed to show that the economy slowed in any material way, rising 0.1% m/m in August while July’s numbers were revised higher to 1.1% from 1.0%.

The First Cut is the Murkiest

Traders are pushing for the Fed to start the easing cycle with an attention-getting 50 bp cut as policymakers’ attention shifts to the job market from inflation. Traders boosted the odds of a rate 50 bp move from 59% yesterday morning to 67% today in what could be seen as bond traders bullying policymakers. The 10-year Treasury yield of 3.62% was last seen in May 2023.

Equity Markets are Mixed to Higher

Asian equity indexes closed on a mixed tone while mainland Chinese markets remained closed for a holiday. Japan’s Topix fell 0.60% due to yen strength while Australia’s ASX 200 climbed 0.24%. The French CAC 40 index has risen 0.83% while the UK FTSE 100 and German DAX are up 78%. S&P 500 futures are up 0.27%.

EURUSD

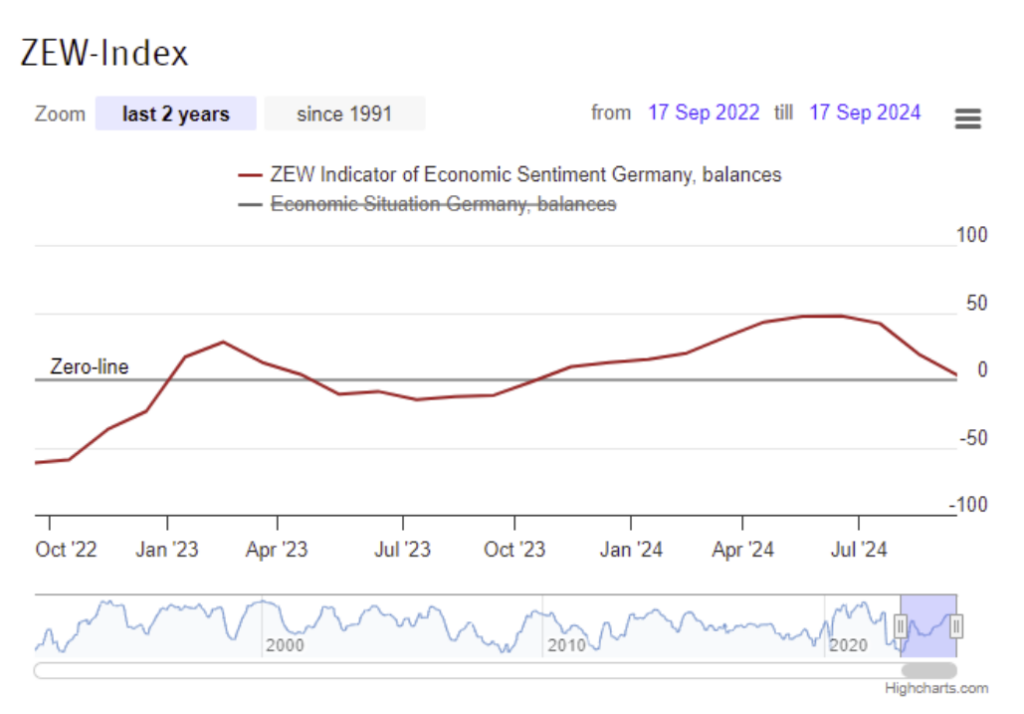

EURUSD is just above the middle of its 1.1115-1.1147 range in early NY. Prices retreated from the peak on the heels of another weak ZEW survey. The statement said: “The ZEW Indicator of Economic Sentiment for Germany recorded yet another considerable decline in the September 2024 survey. At 3.6 points, it is 15.6 points below the August value. The optimism in economic expectations that has been evident since November 2023 has thus almost completely dwindled. The assessment of the economic situation in Germany has also continued to worsen. The corresponding indicator fell 7.2 points to a new value of minus 84.5 points. The assessment of the current economic situation is thus at its lowest since May 2020.”

GBPUSD

GBPUSD is feeling frisky, rising from 1.3199 to 1.3230 due to the prospect of the Fed cutting rates by 50 bps while the Bank of England leaves its benchmark rate unchanged. Traders have ignored a report from academics at Aston Business School which claims Brexit has resulted in a 27% drop in UK exports and imports with the EU. The UK Guardian reported that “The study highlights that the negative impacts of the TCA have intensified over time, with 2023 showing more pronounced trade declines than previous years. This suggests that the transition in UK-EU trade relations post-Brexit is not merely a short-term disruption but reflects deeper structural changes likely to persist.”

USDJPY

USDJPY traded sideways in a 140.32-141.25 range and is trading in NY at 140.59. Japan’s Finance Minister Shunichi Suzuki nattered on about currencies reflecting fundamentals while saying sharp fluctuations are undesirable. Nothing new there. The BoJ is widely expected to leave its rates unchanged at Friday’s meeting, but fear of a rapidly strengthening yen will temper hawkish comments, especially after a 50 bp Fed rate cut.

AUDUSD and NZDUSD

AUDUSD inched higher, rising from 0.6741 to 0.6769 on the back of the rising odds for a 50 bp Fed rate cut. However, ongoing China economic growth concerns will continue to act as a drag. NZDUSD traded firmer in a 0.6183-0.6211 range due to improved risk sentiment and “jumbo” Fed rate cut speculation.

USDMXN

USDMXN traded firmer in a 19.2101-19.2824 range and is near the top of that band in early NY trading. Traders are on hold ahead of the Fed decision on Wednesday. A 50 bp Fed cut suggests USDMXN would drop to 18.1950 due to widening MXN/US interest rate differentials in favor of MXN.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: closed

Shanghai Shenzhen closed

Chinese Markets closed

Chart: USDCNY and USDCNH

Source: Investing.com