By Michael O’Neill

The American economy is slowing while the Canadian economy is a basket case. There is no debate.

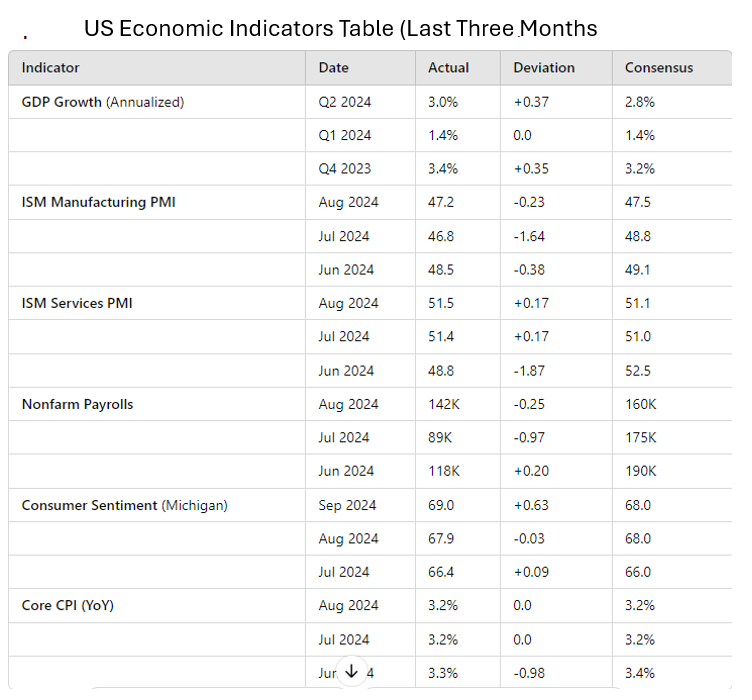

GDP Growth Steady

Let’s start with the U.S. GDP. The second quarter of 2024 saw a 3.0% rise—quite an improvement over the weak 1.4% in Q1. Despite the global uncertainties, the U.S. economy is holding up surprisingly well.

Services Boom Trumps Manufacturing Sector

One of those uncertainties is manufacturing. The ISM Manufacturing PPI was 47.2 in August, it’s clear that the industrial sector is in contraction mode—and it’s been that way for months. But that negative is more than offset by the ISM Services PMI which continues to show steady expansion and since services account for a bigger chunk of the U.S. economy, it more than offsets Manufacturing PMI.

Inflation Tamed

Inflation is under control with Core CPI at 3.2% in both July and August, slightly down from 3.3% in June. And that appears to be keeping consumers happy. Consumer sentiment has remained stable and hovered around 69 in September, a tad better than the 66.4 in July.

Employment Picture Murky

The employment market is the elephant in the room and now the focus of Fed policymakers.Nonfarm Payrolls show a marked slowdown in job creation. August saw only 142K jobs added, which is well below expectations. July was even worse at 89K.

Jerome “Mr Big” Powell

Fed Chair Jerome Powell looked at the same data and decided it was time for his Alan Greenspan performance. Mr Greenspan engineered a soft landing in 1995 that preceded an economic boom and Mr Powell is hoping that history repeats. Futures traders now expect that the September 18, 50 bp rate cut will be followed by another 75-100 bps of cuts by year end. The Fed’s dot-plot has 75 bps of cuts penciled in.

Tiff Not Taking Calls

Bank of Canada Governor Tiff Macklem wishes he was in the same boat as Mr Powell. He isn’t. His boat is filled with Gold Apollo pagers made by a Hungarian company and he fears being pinged.

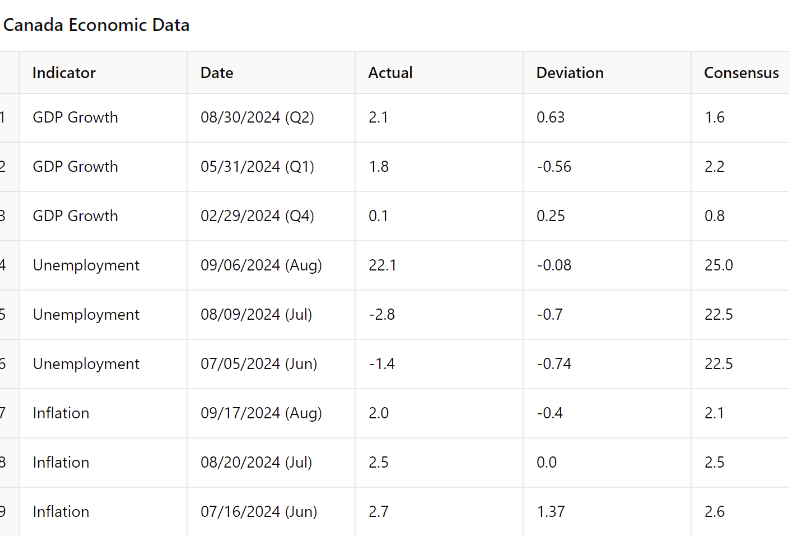

Calling the Canadian economy a basket case is unfair-to baskets. The Canadian economy is hanging on by a thread, and the latest GDP and employment reports make that crystal clear. At first glance, things are “peachy-keen—a 0.5% GDP growth in Q2 and a modest employment increase in August. But dig deeper, and the cracks are everywhere.

Growth Evaporating

Let’s start with GDP. Sure, it grew by 0.5%, but on a per capita basis, GDP actually fell for the fifth straight quarter. That means while the overall economy is expanding, it’s not enough to keep up with population growth. People are getting poorer, not richer. The headline number is masking an economy that’s running on fumes.

Employment Disaster

Then there is the job market. August saw an increase of 22,000 jobs. Unfortunately it was all part-time. Full-time employment fell by 44,000. Workers are being pushed into lower-quality, part-time roles, and it shows. The unemployment rate ticked up to 6.6%, its highest since May 2017 (excluding the pandemic), and it’s been steadily climbing since April. Youth unemployment hit 14.5%.

The Tweet That Keeps on Giving

The Trudeau government has made the problem worse. All it took was one ill-advised tweet in January 2017 by Prime Minister saying, “To those fleeing persecution, terror & war, Canadians will welcome you, regardless of your faith,” to transform the once-functional Canadian immigration department into a bureaucratic dogs breakfast. That one tweet sparked a wave of asylum seekers, many crossing the border illegally, which created a host of other problems including a massive strain on public resources and social services, in addition to housing and employment issues.

BoC Ready to Tackle Downside Risks

None of this is news to Tiff Macklem and company. The Bank of Canada has already cut rates three times since June 5, and if weak economic data continues to roll in, they might follow the Fed’s lead with a 50-basis-point cut on October 23. The Summary of Deliberations confirms this outlook. Policymakers acknowledged the labor market’s softening, with employment growth failing to keep pace with labor force expansion—raising serious concerns about a deeper economic downturn. Mr Macklem may have tipped his hand to the Financial Times recently when he said “As you get closer to the inflation target, your risk management calculus changes. You become more concerned about the downside risks. And the labour market is pointing to some down side risks.

Bond traders are buying into that story The CAD/US 10 yield spread and the 2 year yield spread are only marginally changed following the Fed’s 50 bp rate cut. That is keeping USDCAD gains in check, while the risk of a Canadian recession limits USDCAD downside.

The bottom line? Canada’s economy isn’t just feeble it will soon be swapping the walker for a coffin.