October 3, 2024

- Risk aversion rising on escalating Middle East tensions.

- Yen slides on dovish comments from new Prime Minister.

- US dollar rises on renewed risk aversion.

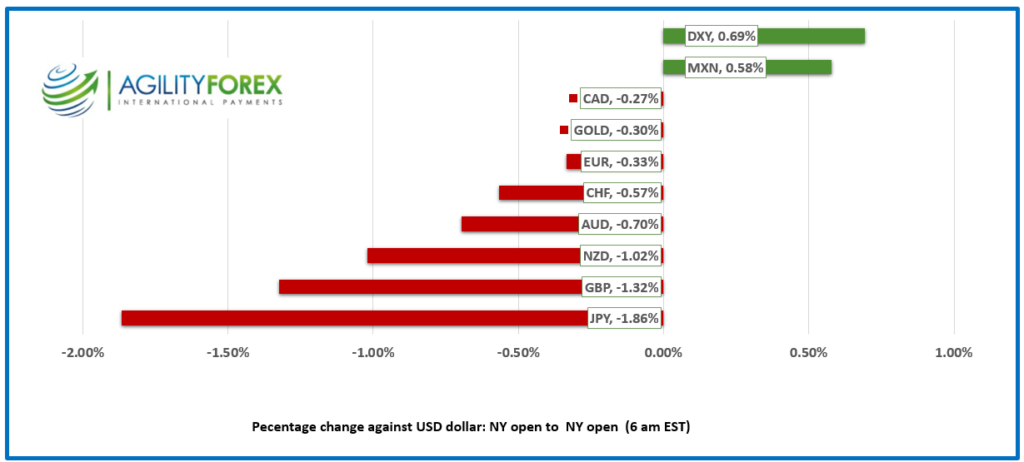

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3535, overnight range 1.3496-1.3542, previous close 1.3503

USDCAD rallied due to risk aversion demand for US dollars, but it remained comfortably ensconced in its well-defined 1.3450-1.3550 range.

USDCAD may garner some additional support after economists at CIBC predicted that the BoC will need to ramp up the pace of interest rate cuts due to weak economic data and the risk of deflation. CIBC believes Tif Macklem, and company will need to cut rates by 50 bps at each of the next two meetings enroute to a 2.25% benchmark rate by June 2025.

Oil prices are steady in a 70.55-71.81 range but supported by expectations of supply disruptions it Israel attacks Iran’s oil infrastructure. Elsewhere, Saudi Arabia said that the WSJ report suggesting that the Saudi Oil Minister warned of 50.00 oil if Opec didn’t comply with quotas was “wholly inaccurate and misleading”.

USDCAD technicals

The intraday USDCAD are bearish inside a 1.3420-1.3540 range supported by the downtrend line from September 19. A break above 1.3540 targets 1.3600.

Longer term, the daily chart shows USDCAD in a downtrend from the beginning of August that remains intact while prices are below 1.3560. A topside break targets 1.3660.

For today, USDCAD support is at 1.3520 and 1.3490. Resistance is at 1.3550 and 1.3590.

Today’s Range 1.3510-1.3580

Chart: USDCAD 4 hour

Source: Oanda.

Ayatollah’s Airball

Global markets are trading with a degree of caution after Iran’s “forceful retaliation” against Israel failed spectacularly, and Israel didn’t even use its most modern and effective missile defense strategy. Traders are awaiting Israel’s response to the 180-ish missile barrage fired by Iran at Israeli targets, including Tel Aviv. Israel’s response could range from a precision, tactical strike to regime-changing devastation.

US Data Feast

The Fed’s focus is the labor market, and policymakers have indicated that rate cuts can only occur if the employment market eases. Yesterday’s ADP data suggested the job market was resilient, and this mornings Challenger Job cuts report supports that view. Challenger reported 70,000 viewer layoffs in September. However, weekly jobless claims data suggests otherwise. Claims rose by 6,000 to 225,000 which is in line with the weekly average of 224,250000. ISM Services and factory orders reports are coming up.

Kansas City Fed President Jeffery Schmid, Atlanta Fed’s insider trading President Raphael Bostic, and Cleveland Fed President Neel Kashkari are talking, and they may provide further insight into the interest rate outlook.

Equities are Resilient

Asian equity indexes closed with gains. The sharply falling yen boosted Japan’s Topix index to a 1.20% gain, while Australia’s ASX 200 closed virtually unchanged. European bourses are lower, except for a 0.20% gain in the UK FTSE 100 index. S&P 500 futures are down 0.13%.

EURUSD

EURUSD traded in a 1.1025-1.1050 band with prices weighed down by broad US dollar demand. Traders ignored composite and services PMI reports, which were a tad better than expected, mainly because the odds are that the ECB cuts rates by 25 bp on October 17.

GBPUSD

GBPUSD got hammered, falling to 1.3106 in NY from an overnight peak of 1.3274, thanks to broad US dollar weakness and surprisingly dovish comments from Bank of England Governor Andrew Bailey. Mr. Bailey did the most damage when he suggested that policymakers could become “a bit more aggressive” in trimming interest rates if the inflation news continued to be good. The UK Services PMI data supported his comments, noting “PMI surveys suggest that the UK economy is still on a positive trajectory, with improving order books accompanied by cooling inflationary pressures.”

USDJPY

USDJPY surged, rising from 146.28 to 147.24 after comments from the new Prime Minister offset safe-haven demand for yen. Shigeru Ishiba kicked off the rally on Wednesday when he claimed that the economy was not ready for another rate hike. His comments were echoed by BoJ Governor Kazuo Ueda, who also expressed caution about raising rates, suggesting the focus should be on bolstering the economic recovery. Prices were also underpinned by the tick-up in the US 10-year yield to 3.815% today from 3.78% yesterday.

AUDUSD and NZDUSD

AUDUSD suffered from a bout of risk aversion and mixed economic data, and it is sitting at the bottom of its 0.6845-0.6889 overnight range. Australia’s Services sector PMI eased at the end of Q3 while new business growth slowed due to a downturn in export business. It wasn’t all bad news—Australia’s trade surplus rose from AUD$5.636 billion to AUD$5.644 billion.

NZDUSD traded in a 0.6216-0.6273 range due to broad US dollar strength and the prospect of RBNZ interest cuts on October 8.

USDMXN

USDMXN is consolidating yesterday’s losses in a 19.3944-19.4875 range. The decline occurred despite yesterday’s US ADP data supporting calls to defer 50 bp Fed rate cuts, in part because Banxico Deputy Governor Jonathan Heath said domestic rates should remain unchanged for longer.

BTCUSD (Bitcoin)

Bitcoin traded sideways in a 60,139-62,480 band. Rising geopolitical tensions are weighing on risky assets, and BTCUSD is suffering. Traders fear that a decisive break below 60,000 will lead to a test of 55,000.

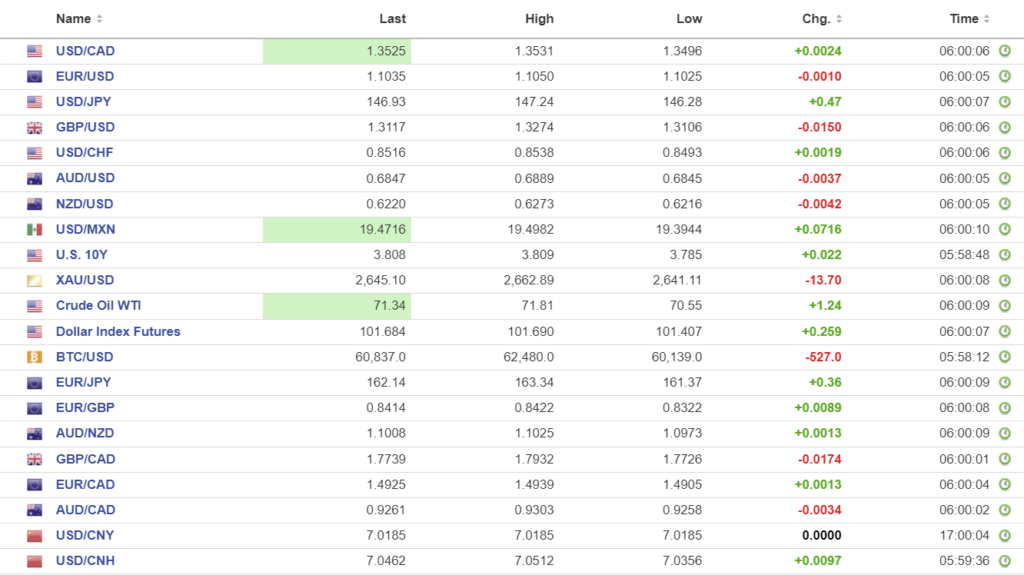

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: unchanged 7.0074 (prev. 7.0101)

Shanghai Shenzhen CS! 300 closed at 4017.85 (as of September 30)

Chinese markets closed for Golden Week.

Chart: USDCNY and USDCNH

Source: Investing.com