By Michael O’Neill

What’s the hurry? That’s the message Fed Chair Jerome Powell gave to global markets in a speech to the National Association for Business Economics in Nashville earlier this week. Mr Powell said, “We’re in no rush to cut rates,” and then explained why. He said that September’s 50 bp cut was just a “recalibration”—not a signal that similarly sized cuts are coming down the pipeline. The Fed’s game plan, Powell emphasized, is to go meeting by meeting, carefully weighing the data before making any moves.

Bond traders were unhappy. Many were positioned for a 50 bp drop at the November 7 meeting. That changed quickly with the odds of that happening falling from a pre-Powell speech level of 69% to 36.3% by October 2. Stronger-than-expected employment reports, including higher-than-expected Job Openings, ADP employment and weekly jobless claims, are justifying Mr Powell’s caution.

The Only Constant is Change

There will be plenty of Fed officials offering up their expertise and monetary policy analysis until the FOMC blackout period begins on October 26. Any one of them could offer up an opinion that roils bond, currency, and equity markets. Mr. Powell was adamant that the FOMC would carefully assess incoming data, the evolving outlook, and the balance of risks. And there is a ton of top-tier incoming data coming down the pipeline before the next FOMC meeting. The October 4 nonfarm payrolls report will be forgotten before policymakers nibble on their first pastry on November 7, due to an abundance of fresher employment data, including the November 1 NFP release followed by another JOLTS and ADP report. The times they are a-changing.

Squid Game-American Style.

In South Korea’s dystopian survival series Squid Game, 456 financially strapped players battle in brutal children’s games where the loser dies. The American version? Far less dramatic—there are just two contestants. The prize? Becoming the 47th President of the United States.

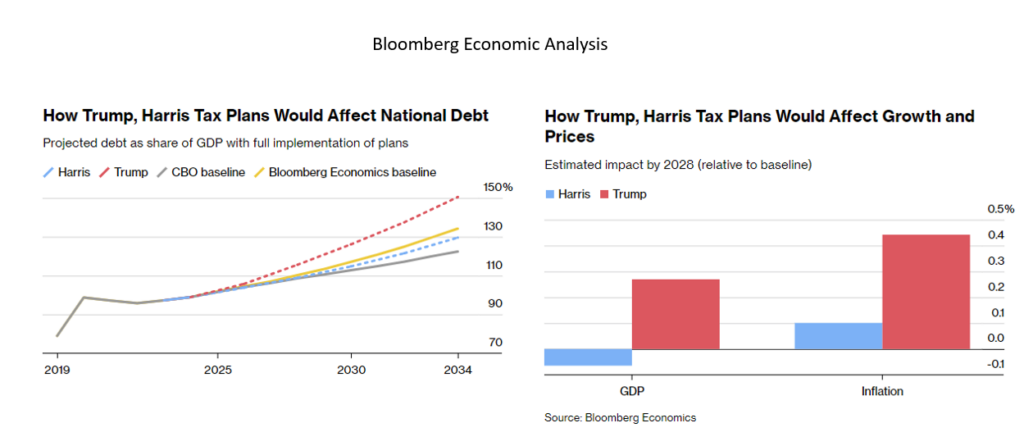

Regardless of who wins, US debt will balloon. Bloomberg estimates that Donald Trump’s platform of tax cuts will raise the debt-to-GDP ratio from about 99% in 2024 to 116%. Kamal Harris’s platform will only lift the debt-to-GDP to 109%. Statista.com estimates that the public debt of the US in August 2024 is $35.3 trillion, so with a number that big, the $1.4 trillion difference between candidates is merely a rounding error. In fact it is less than the $2.3 trillion the US government spent attempting to eradicate al-Qaeda in Afghanistan only to leave 20 years later with anti-US Taliban in charge. The following chart is how Bloomberg economists see the economic impact between Harris and Trump platforms. (Bloomberg owner Michael Bloomberg is a Democrat)

Source: Bloomberg.com

Read This and Weep

US debt may soon surpass 100% of GDP, and as crazy as it sounds, the country can afford it. The US dollar is the world’s reserve currency, which generates constant demand for US debt. Plus, the US economy is vast, diverse, and one of the most productive and innovative on the planet. When problems arise, America can either work or invent its way out.

Canadians may feel smug. Canada’s debt-to-GDP ratio is a mere 69.8%, which looks pretty good. The Prime Minister and Finance Minister proudly trumpet that its debt-to-GDP ratio is the lowest of the G7 and is ranked number 5 of 32 nations. However, the performance is from fudging the books. The government is calculating its net debt and including the assets of the Canada and Quebec Pension funds. The results are also misleading. 27 of 32 major countries calculate debt-to-GDP ratios using gross debt, and if Canada did the same, it would rank #26.

Rate Cut Express

The Fed may not be in a hurry to cut interest rates, but if economists at CIBC are correct, the Bank of Canada is likely in a mad rush. They are predicting a 50 bp rate cut at the October 23 and December 11 monetary policy meetings and then another 75 bps of cuts by the June 4, 2025. The biggest reason for the aggressive rate moves is because of the rising risk of deflation. Canada’s economy is already sluggish. Canada’s productivity is the worst performing of all advanced economies since 2019 and deflation will exacerbate the problem. If prices are dropping, consumers will delay purchases, and productivity will continue to fall.

Canadian and US interest rates may be eventually landing on 2.5% but for the Canadian dollar, the speed of the journey to that level is most important. If the Bank of Canada has booked a seat on the “Rate Cut Express” while the FOMC is content with a milk run to 2.5%, USDCAD has very limited downside.