October 8, 2024

- Light data calendar and hurricane sap trading enthusiasm.

- WTI oil drops 3.0% despite supply disruption concerns.

- US dollar opens marginally mixed compared to Monday.

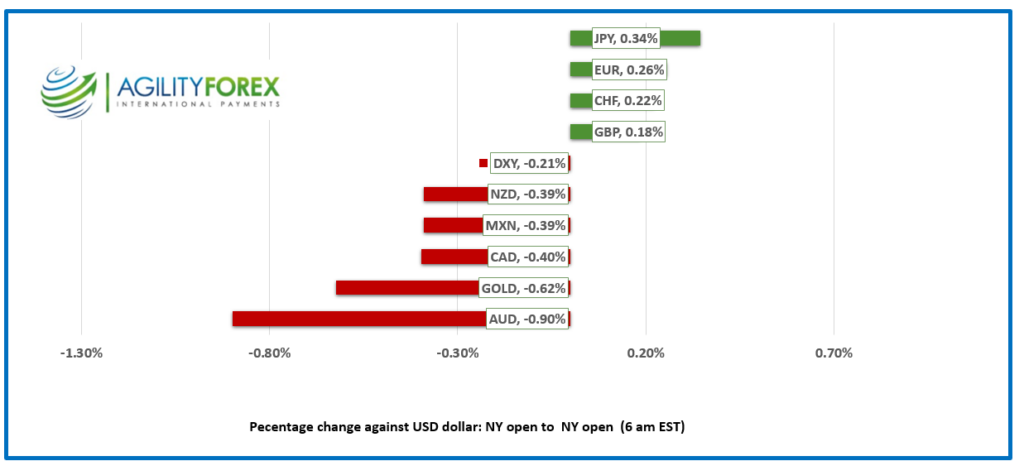

FX at a Glance

Source: IFXA/RP

USDCAD open 1.3645, overnight range 1.3611-1.3648, previous close 1.3620

USDCAD extended yesterday’s gains overnight due higher US Treasury yields. The CAD/US 10-year yield spread narrowed to -76.6 which is down from -80 a week ago. That implies that the risk for owning Canadian dollars vis a vis the US has improved when recent economic data suggests that is not the case. The BoC needs to cut rates by 50 bps on October 23, to help boost a sluggish and slowing economy. The Fed doesn’t have that worry (at the moment) as is expected to cut rates by just 25 bps in November.

Canada’s oil sands business got a boost of confidence following news that Canadian Natural Resources is buying Chevron’s Athabasca Oil Sands and Duvernay Shale formation for $6.5 billion. Does that mean that Canadian Natural Resources Chairman Murray Edwards just flipped the bird at Canada’s environment minister Steven Guilbeault?

USDCAD technicals

The intraday USDCAD are bullish following the break above the 200 day moving average at 1.3602 which extend gains to resistance in the 1.3650 area. The uptrend channel from October 3 is intact while prices are above 1.3610 with the top of the band at 1.3890.

The longer term USDCAD technicals are bullish with the move above 1.3610 reverting to support. However, Bollinger band and RSI studies suggest USDCAD is approaching extreme overbought levels which suggests prices may need to consolidate in a 1.3610-1.3690 range.

For today, USDCAD support is at 1.3610 and 1.3570. Resistance is at 1.3660 and 1.3690.

Today’s Range 1.3610-1.3680

Chart: USDCAD daily

Source: Investing.com

War, Milton, and Cautious Traders

Traders are biding their time today due to a light US economic data calendar and are focused on other distractions. Traders are still waiting to see how Israel will respond to Iran’s attack on October 1, fearing a full-blown war. Meanwhile, Hurricane Milton, a nasty Category 5 storm, hasn’t even made landfall yet but has already caused a few oil platforms to shut down and is heading for the already storm-battered Florida Gulf Coast. Oil prices declined as the supply disruption from the storm is expected to be minimal. Authorities have ordered what may soon be the largest evacuation in the state since 2017.

Fed Speak and Equities

A gaggle of FOMC members reiterated the Fed’s intention to cut interest rates further yesterday, but none of them said anything new. However, NY Fed President John Williams stated that “the 50bp rate cut in September was not the rule of how we will act in the future.”

Asian equity indexes closed in the red, led by a 9.4% plunge in Hong Kong’s Hang Seng. European bourses are all negative, with the UK FTSE100 falling 1.12%. Meanwhile, S&P 500 futures are up 0.30%.

EURUSD

EURUSD drifted modestly higher overnight in a 1.0972-1.0998 range, although prices remain well below Friday’s pre-NFP level of 1.1040. News that German Industrial Production rose 2.9% m/m in August, topping the forecast of 0.8%, may have helped nudge prices higher. However, ING analysts suggest that the results are merely a technical rebound and not an indication of recovery.

GBPUSD

GBPUSD traded in a 1.3064-1.3104 range. The currency continues to suffer from fears that the Bank of England will cut rates faster than the Fed, which Governor Andrew Bailey hinted at last week. UK BRC Retail Sales rose 1.7% in September, compared to 0.8% in August.

USDJPY

USDJPY continued to consolidate Friday’s gains and traded sideways in a 147.34-148.20 range. Prices are underpinned by the US 10-year Treasury yield, which is sitting at 4.03%, with traders laughing at the usual verbal intervention by Japanese officials.

AUDUSD and NZDUSD

AUDUSD slid from 0.6769 to 0.6715 due to falling commodity prices, positive economic data, and inconclusive RBA minutes. The disappointment from China’s National Development and Reform Commission’s failure to announce fresh stimulus weighed on commodity prices, while the RBA minutes were wishy-washy. Policymakers discussed both rate hike and rate cut scenarios. Meanwhile, the NAB Business Confidence survey fell 0.2, which was better than the -0.5 in August.

NZDUSD traded lower in a 0.6108-0.6146 range due to broad-based US dollar strength ahead of the anticipated 50 bps rate cut by the RBNZ tomorrow.

USDMXN

USDMXN drifted in a 19.2706-19.3586 range and is at 19.3200 in early NY. The Citibanamex Survey released yesterday shows a unanimous call for a 25 bp rate cut to 10.5%. Projections for headline and core inflation in September are 4.6% and 3.9%, respectively. Estimates for USDMXN by year-end are 19.67 compared to 19.57 previously. GDP growth is expected at 1.5% in 2024 and 1.2% in 2025.

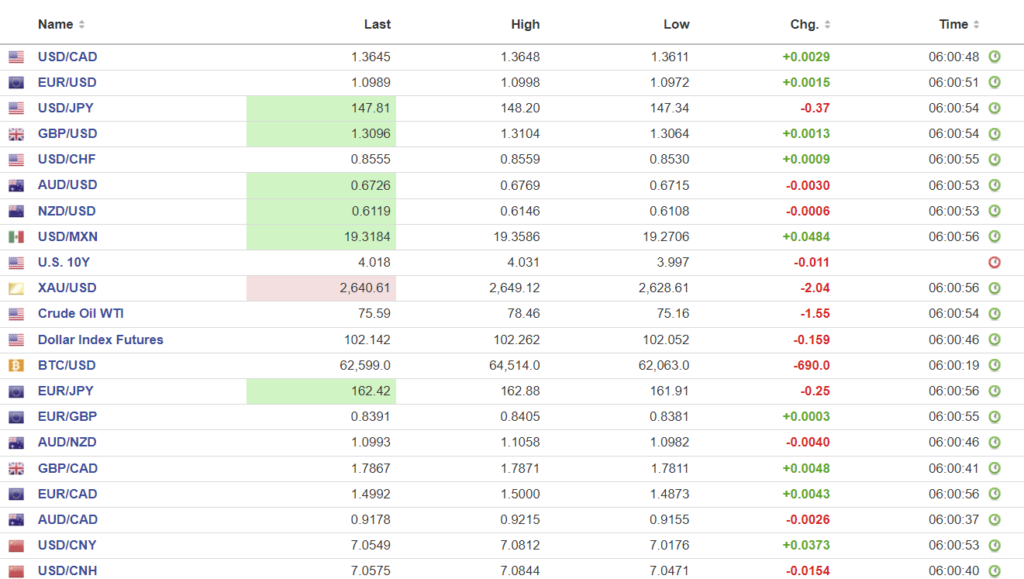

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: unchanged 7.0709 (prev. 7.0074)

Shanghai Shenzhen CS! 300 rises 5.93% to 4256.10: closed at 4017.85 – September 30: Hong Kong Hang Seng falls 9.4% to20926.79,

The CSI rose 11% at the open but gains faded throughout the day. The results are a disappointment to those who expected even further gains after the pre-golden week rally. They were hoping today’s National Development and Reform Commission’s press conference would offer fresh stimulus. It didn’t. However, today’s market sell-off may have just been profit-taking after fantastic gains in the previous 21/2 weeks.

Chart: USDCNY and USDCNH

Source: Investing.com