November 1, 2024

- Nonfarm Payrolls data skewed by hurricanes-NFP rises by 12,000

- Many European and other markets closed for All Saints Day

- US dollar grinds out tiny gains.

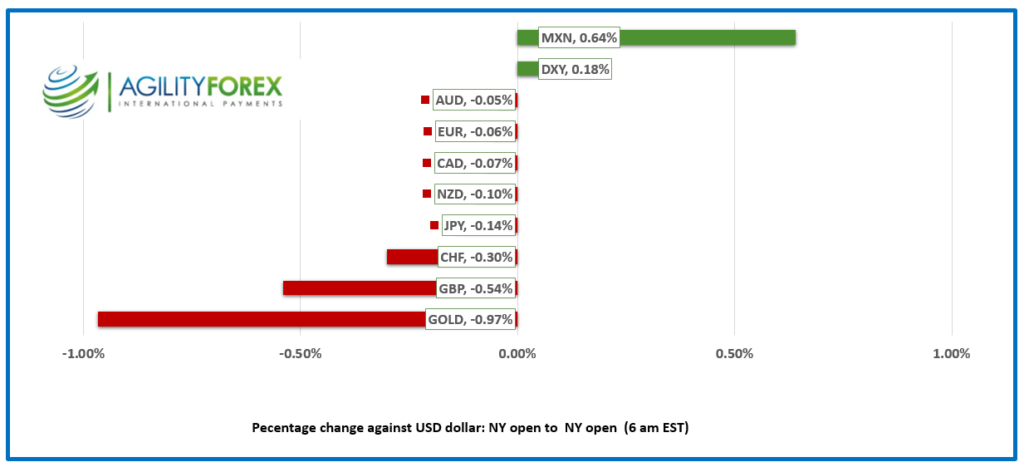

FX at a Glance

Source: IFXA/RP

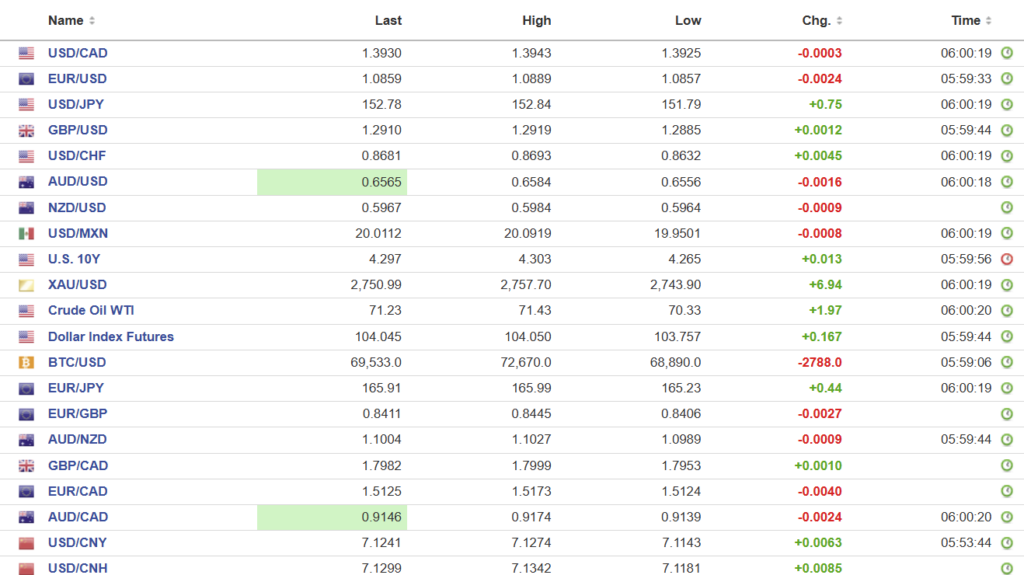

USDCAD open 1.3930, overnight range 1.3908-1.3943, close 1.3935

USDCAD spiked to 1.3945 yesterday following yet another dismal GDP report and has been trading with a bullish bias ever since. The Canadian economy is crawling compared to the robust growth in the U.S., where Q3 saw 2.8% y/y growth, while Canada will be lucky to reach 1.0% in Q3. Weakness in Canadian manufacturing has been a significant contributor. The U.S. economy is running above potential, and the unsettling part is that Canada’s economy might be inching past its limits too.

“Get Over It, Already!”

Iran’s Ayatollah Khamenei, a ruler long past his best-before date, is reportedly planning yet another attack on Israel in retaliation for Israel’s retaliation on Iran, which itself was in retaliation for… and the cycle continues. Apparently, he won’t rest until his entire Iranian Revolutionary Guard Corps is martyred. Israel claims to have intelligence on Iran’s plans for a missile and drone attack from Iraq, and oil traders are taking it seriously—WTI has surged 6.3% since Tuesday.

Today’s US NFP and ISM data may be non-events as the market’s focus remains on the US election.

USDCAD Technicals

The intraday USDCAD technicals are bullish above 1.3910 and looking for a decisive break above 1.39 50 to extend gains to 1.3990, then 1.4040. A break below 1.3910 suggests a drop to 1.3860.

The USDCAD uptrend that began on April 2022 remains intact above 1.3540, a level guarded by support at 1.3600 and 1.3720.

For today, USDCAD support is 1.3910 and 1.3860. Resistance is 1.3950 and 1.3990.

Today’s Range 1.3910-1.3990

Chart: USDCAD daily

US NFP Report – Only One Job Matters

Nonfarm payrolls rose by a mere 12,000 jobs, compared to the forecast of 113,000 and last months 254,000 gain. The data is dodgy due to the impact from two hurricanes and one Boeing strike. The dollar’s reaction was typical of for useless information-It barely reacted at all. Nevertheless, for today, and for the US, only one job matters: the winner of the presidential election. ISM manufacturing data will have minimal impact ahead of Tuesday’s vote.

Winners and Losers

In Europe, today is All Saints Day, a holiday when traders thank the “Patron Saint of Lucky Trades” for financial windfalls. Elsewhere, it’s the Day of the Dead, a lively tribute to the ghosts of losing trades. For the rest of the world, it’s a day of lighter-than-usual liquidity.

Tech Earnings Cause Headaches

The fallout from disappointing Meta and Microsoft outlooks eased somewhat following Amazon and Intel’s quarterly reports but not enough to calm Asian equity traders. Japan’s Topix lost 1.90% while Australia’s ASX 200 dropped 0.50%. Better-than-expected Caixin PMI data for China helped lift Hong Kong’s Hang Seng by 0.90%. European bourses are trading in the green, led by a 0.59% rise in the UK FTSE 100 index. S&P 500 futures are up 0.34%, and the US 10-year Treasury yield is steady at 4.30%.

EURUSD

EURUSD gave back most of Thursday’s gain, trading negatively in a 1.0854-1.0889 range with prices in an uptrend above 1.0810. EURUSD is supported by expectations for a less dovish ECB monetary policy meeting on November 14, following higher inflation readings. Many Eurozone markets are closed for All Saints Day.

GBPUSD

GBPUSD traded in a 1.2885-1.2919 range as it consolidates yesterday’s budget losses. The 10-year Gilt market has calmed down, with yields sitting at 4.473%, off the 4.53% peak but still well above the pre-budget level of 4.21%. The technicals are bearish below 1.3000, with a potential test of the 1.2770 area.

USDJPY

USDJPY drifted higher in a 151.79-152.85 range, supported by higher US 10-year Treasury yields, which overshadowed recent BoJ policy meeting outcomes and Governor Kazuo Ueda’s comments downplaying risks against further tightening.

AUDUSD and NZDUSD

AUDUSD drifted lower in a 0.6556-0.6584 range due to broad US dollar strength and caution ahead of the US election and Monday’s RBA monetary policy decision. Traders largely ignored Q3 PPI data, which ticked lower to 0.9% from 1.0%, and the better-than-expected Chinese PMI report. NZDUSD traded in a 0.5964-0.5984 range with NZ employment data due on Wednesday.

USDMXN

USDMXN is basking in the glow of Thursday’s higher-than-expected Q3 GDP growth (actual 1.0% versus forecast 0.60% q/q and 1.5% y/y), though the optimism is unlikely to last. USDMXN traded in a 19.9501-20.919 range, hovering just above its session low.

BTCUSD (Bitcoin)

Bitcoin is feeling the strain of election jitters. Prices dropped from 72,620 to 68,890, likely due to unwinding of some of the “Trump trade.” BTCUSD previously rallied on hopes of a crypto-friendly Trump win, and some traders may now be booking profits.

FX high, low, open (as of 6:00 am ET)

Source: Investing.com

China Snapshot

PBoC fix: 7.1135 (prev. 7.1390)

Shanghai Shenzhen CSI 300 fell 0.003% to 3890.02

Operating conditions in China’s manufacturing sector improved at the start of the final quarter of the year. The headline seasonally adjusted Purchasing Managers’ Index PMI rose to 50.3 in October, up from 49.3 in September.

Caixin Senior Economist Dr Wang Zhe wrote: In summary, October saw growth in manufacturing supply and demand, increases in prices, proactive inventory replenishment by companies, and logistics delays. Business optimism improved. However, weak external demand and declining employment remained areas of concern.

Chart: USDCNY and USDCNH

Source: Investing.com