January 15, 2025

- US CPI cools in December

- Canada Manufacturing and Wholesale Sales weaker than in November.

- USD consolidates lower following tame PPI data on Tuesday.

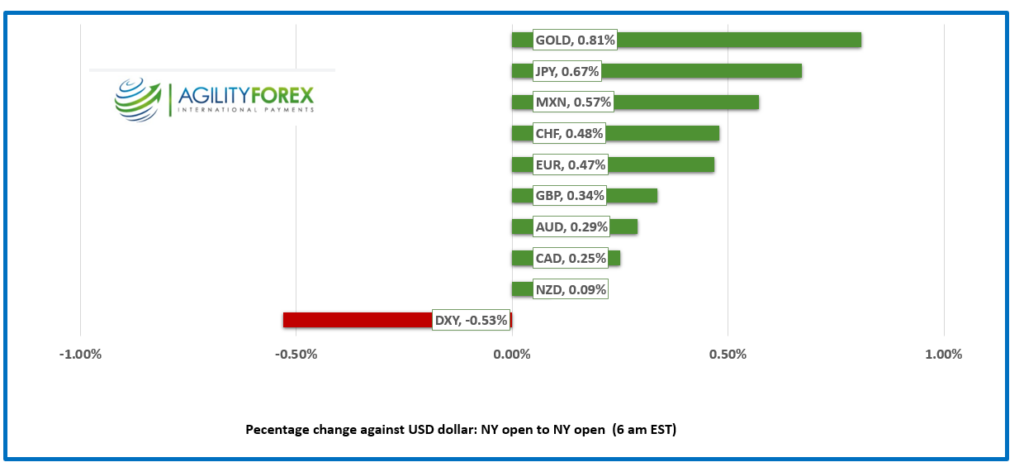

FX at a Glance

USDCAD open 1.4346, overnight range 1.4303-1.4364, close 1.4348

USDCAD dropped on improved risk sentiment following yesterday’s cooler than expected US PPI data, then accelerated lower after the cooler than expected US inflation numbers.

The chances that USDCAD sustains these losses are very slim. That’s because tariffs are likely to be a reality, as Alberta Premier Daniell Smith believes after meeting with Trump on the weekend. A internal Liberal party strife, leading to the proroguing of parliament has handcuffed Canada’s ability to respond.

WTI oil traded defensively in a 76.16-77.19 range overnight but rallied to the top in NY trading. Prices are supported from the 2.6 million barrel drawdown as reported by API but an easing of middle east tensions may limit gains.

Canada Manufacturing and Wholesale Sales data were weaker than they were in November but beat the forecast. The results were overshadowed by US inflation data.

USDCAD Technicals

The intraday USDCAD technicals are bearish with an intraday downtrend intact while prices are below 1.4370 (hourly chart) with a move below 1.4290 targeting 1.4260. A move above 1.4370 will extend gains to 1.4440. The retreat is helping to ease the substantial USDCAD “overbought” condition.

The USDCAD uptrend from the end of October is intact while prices are above 1.4240

For today, USDCAD support is 1.4290 and 1.4260. Resistance is 1.4470 and 1.4490

Today’s Range: 1.4290-1.4390

Chart: USDCAD 4 hour

Ceasefire in Gaza?

Glimmers of hope have emerged for a ceasefire in Gaza, aided by the decimation of Hamas leadership, along with Iran’s diminished influence. Incoming President Trump’s warning of “hell to pay” if hostages were not released further accelerated negotiations. Meanwhile, the polar vortex gripping large parts of Canada and the U.S. has inadvertently put an end to “free Palestine” protests. “Talk about fair-weather friends.”

Show Me the Money

The quarterly “opening of the kimono” kicks off today. JPMorgan Chase got the ball rolling and is up 2.07% in pre-market trading after its Q4 earnings beat expectations. Goldman Sachs also boasted forecast-beating results. Asian equity markets closed on a mixed note. The ASX 200 index fell 0.22%, while the Topix rose 0.31%. European bourses surged in the wake of the US inflation numbers with a 1.56% rise in the German DAX leading markets higher. S&P 500 futures surged from just above flat to up 1.59%. The US 10-year Treasury yield plunged to 4.69% from its pre-CPI level of 4.76%.

“Can I Have CPI for $100, Alex?”

Inflation Jeopardy is a popular pastime for traders. The Fed’s fight to tame the beast leads to sharp spikes in volatility for most asset classes. Today’s data proved the case. December Core-CPI rose 3.3% y/y in December (forecast and previous 3.3%) which is a move in the right direction. However, it is still well above the Feds target which suggests that today’s market reaction on hopes the Fed will be less hawkish, is premature

EURUSD

NY open 1.0307, overnight range 1.0287-1.0317-then 1.0355 post CPI.

EURUSD rallied yesterday, but gains may be facing headwinds from dovish ECB comments. Vice President Luis de Guindos said, “The policy trajectory is clear, and we expect to continue to further reduce the restrictiveness of monetary policy. The latest information suggests that the economy is losing momentum.” His words countered remarks from colleague Robert Holzmann, who yesterday said that stubbornly high inflation should temper the pace of rate cuts. Eurozone Industrial Production fell 1.9% y/y in November. Trading will be messy around the option expiry window (10:00 AM EST) with $3.1 billion of 1.0295-00 strikes maturing and another $2.1 billion of strikes in the 1.0330-50 area.

GBPUSD

NY open 1.2227, overnight range 1.2161-1.2241-1.2306 after USD CPI

Sterling got a boost despite lower-than-expected UK inflation numbers. Core CPI rose 3.2% y/y compared to 3.4% that was expected and 3.5% in November. PPI and Retail prices also fell. The rally was sparked by the rise in Gilt yields due to the UK fiscal situation being in the spotlight. The odds for a February rate cut rose from 62% to 85% in the wake of the data.

USDJPY

NY open 156.78, overnight range 156.71-158.08-156.25 after CPI

USDJPY dived following comments by BoJ Governor Kazuo Ueda, who strongly hinted that the BoJ would raise rates on January 24. Mr. Ueda said, “We are currently analysing data thoroughly and will compile the findings in our quarterly outlook report. Based on that, we will discuss whether to raise interest rates at next week’s policy meeting and would like to reach a decision.”

AUDUSD

NY open 0.6204, overnight range 0.6181-0.6212-0.6247 after US CPI

AUDUSD traded in a similar range to yesterday, with prices underpinned by the hope that US inflation will continue to drift lower.

NZDUSD

NY open 0.5614, overnight range 0.5597-0.5626 -0.5661, post-CPI

NZDUSD moves mirrored those of its antipodean cousin. Traders are waiting for today’s US inflation numbers and still benefiting from optimism that the US might impose graduated tariffs rather than starting at 10%. New Zealand Business Confidence rose 16% q/q in Q4 compared to -1% in Q3.

USDMXN

NY open 20.5117, overnight range 20.4974-20.5634-20.3978, post-CPI

USDMXN retreated due to improved risk sentiment after yesterday’s PPI data and continued to trade at its session low in NY.

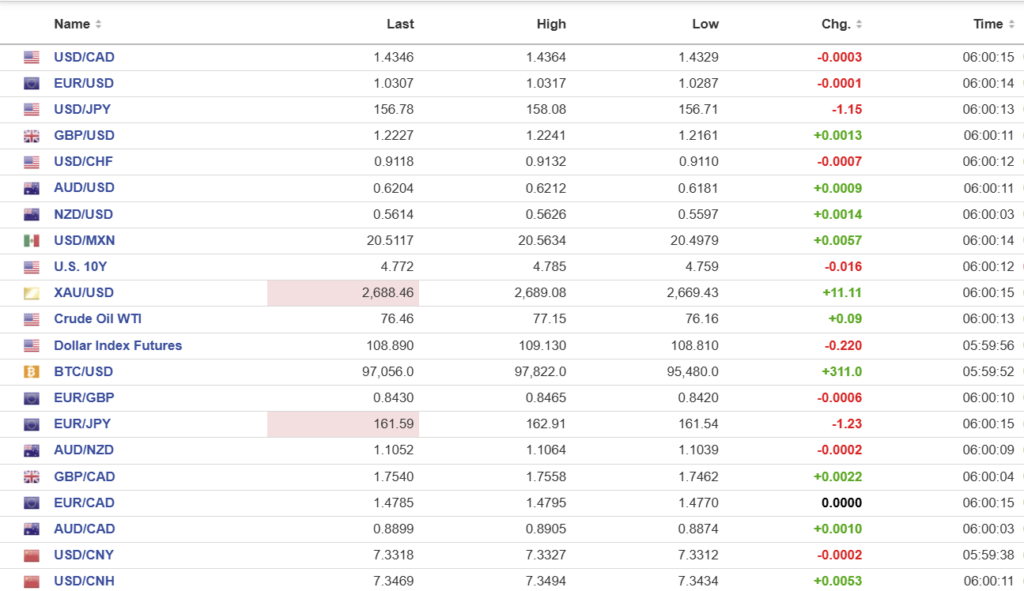

FX high, low, open (as of 6:00 am ET)

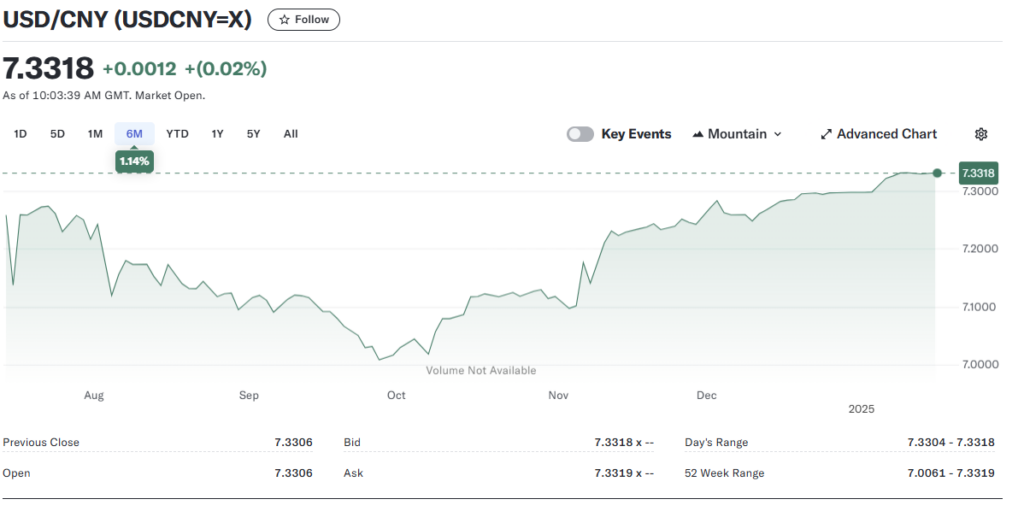

China Snapshot

PBoC Fix: 7.1883 vs exp. 7.3240 (prev. 7.1878)

Shanghai Shenzhen CSI 300 fell 0.64% to 3796.03

The PBoC is pumped about $130.9 billion of liquidity into the system using 7-day repos. The WSJ said it was needed to offset the impact from the expiration of medium-term lending facility loans, plus tax payments due and increased cash demand before the Lunar New Year holiday. The move is also seen as another bit of support for the yuan.

Chart: USDCNY

Sources: Yahoo Finance, Oanda, Investing.com, Google Finance