March 24, 2025

- Equities rebound, while currencies shrug of tariff dilution talk.

- Eurozone and German PMI data shows cautious optimism.

- USD opens close to flat on tariff uncertainty,

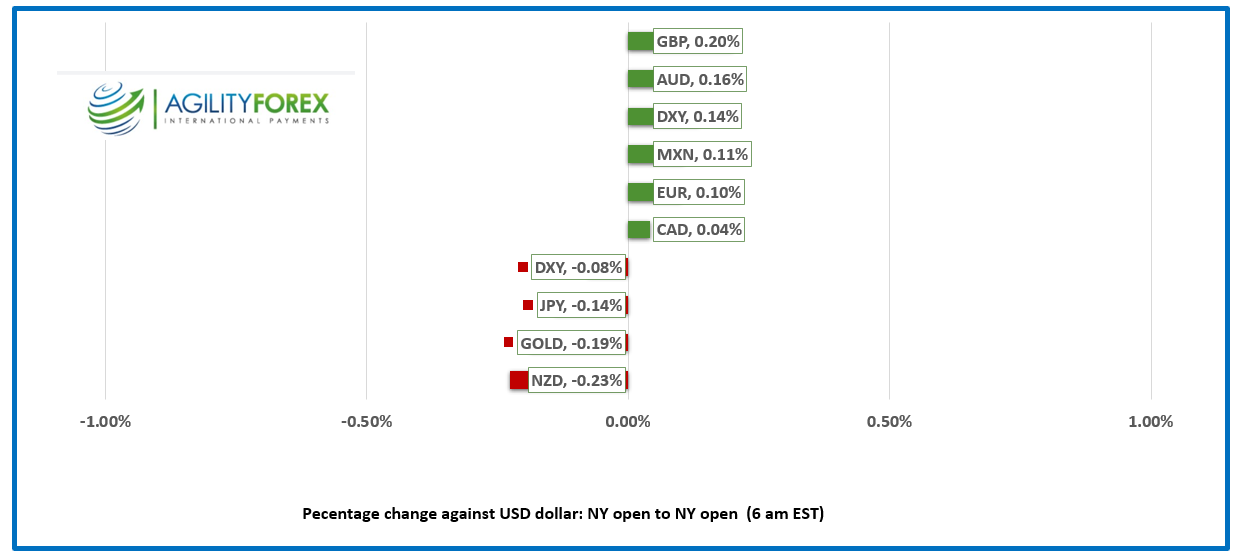

FX at a Glance

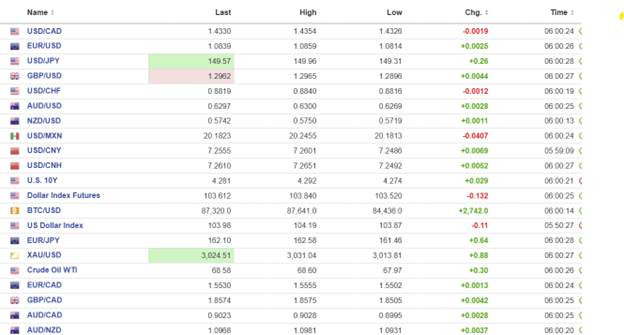

USDCAD: open 1.4337, overnight range 1.4314-1.4354, close 1.4325

USDCAD drifted lower on talk of Liberation Day tariffs being diluted, particularly those affecting autos.

The long-awaited Canadian Federal elections is April 28. Unbelievably, the Liberals and PC’s are neck and neck in the polls and it is all because voters believe Mark Carney is the man to deliver economic growth, and deal with Trump.

That isa real head-shaker. Carney, the UN Special Envoy on Climate Action and Finance (until January 25, 2025) said he firmly believes that “Climate change is an existential threat.” Now he is promising to scrap the carbon tax and focus investing in green tech. He told an audience in Western Canada that he was “pro-pipeline” and then said he was “anti-pipeline to a Quebec audience. Larry Elliot of the UK Guardian, a left wing newspaper wrote an interesting article on Carney. The man is not impressed. Do Canadian’s really think he has changed?

Trump’s tariff agenda is what is driving USDCAD direction and that will ensure the downside is limited.

USDCAD

The intraday USDCAD technicals are bearish below 1.4370 and looking for a break below 1.4300 to extend losses to 1.4270, then 1.4240. A move above 1.4370 targets 1.4420.

The medium-term outlook remains bullish while prices are above 1.4270 which is the 38.2% Fibonacci retracement of the September-February, 1.34201.4785 range. A decisive move below 1.4270 suggests further losses to the 50% Fibonacci level of 1.4212.

For today, USDCAD support is 1.4300 and 1.4270. Resistance is at 1.4370 and 1.4420.

Today’s Range: 1.4310-1.4380.

Chart: USDCAD 1 day

Diluting Tariffs

Someone must have convinced Trump that his planned imposition of tariffs on what Trump is calling “Liberation Day” needed to be tweaked. The risk of shuttered auto plants, higher inflation and increased unemployment rates, combined with a free-falling stock market, is tarnishing his brand and angering his core base of supporters. Bloomberg reported that Trump is still planning to announce “reciprocal tariffs” but will exclude some nations and he will not announce sectoral-specific tariffs.

Geopolitical Tensions Swirling

The US spearheaded Russia/Ukraine ceasefire talks in Saudi Arabia while another Trump delegation is attempting to get a ceasefire in the Black Sea. Meanwhile, the ceasefire in Gaza appears to have ended with Israel conducting airstrikes in Gaza and Syria in response to missile attacks. And now, Turkey’s President Recep Erdogan arrested his closest rival, Istanbul Mayor Imamoglu, on terrorism charges, as Erdogan is terrified of losing the next election. If you can’t beat ’em—lock ’em up.

Asian equity indexes closed with Japan’s Topix falling 0.47%, Hong Kong’s Hang Seng rising 0.51%, and Australia’s ASX 200 unchanged (+0.07%). European bourses are perky. The UK FTSE 100 and French CAC 40 are flat while the German Dax is up 0.16%. S&P 500 futures are up 0.97% but off its best level. The US 10-year Treasury yield has risen 4 ticks to 4.297%, while gold prices are up $8.00.

EURUSD

NY Open: 1.0839, Overnight Range: 1.08214-1.0859

EURUSD eked out small gains in an uneventful session despite positive results from German and Eurozone PMI reports. March Manufacturing PMI rose to 48.3 (forecast 47.2) in Germany and 48.7 (forecast 48) in the Eurozone. Hamburg Bank Chief Economist Cyrus de la Rubio wrote, “While we should not be carried away by a single data point, it is noteworthy that manufacturers expanded their output for the first time since March 2023. It’s also encouraging that the index output has risen for three months straight.”

GBPUSD

NY Open: 1.2962, Overnight Range: 1.2896-1.2965

GBPUSD has popped above the top of its overnight range in the wake of a stronger-than-expected Services PMI report (actual 53.2, forecast 51.2, previous 51) and the reports that Trump will dilute his April 2 tariffs. Traders are still focused on the Chancellor’s Spring Statement, which is due on Wednesday.

USDJPY

NY Open: 149.57, Overnight Range: 149.31-149.96

USDJPY traders were unimpressed with the contraction in Jibun Manufacturing PMI in March (actual 48.3 vs forecast 49.2) and prices rose steadily. Improved risk sentiment due to hopes of a downgraded tariff threat, combined with the higher US 10-year Treasury yield, helped to underpin prices.

AUDUSD

NY Open: 0.6297, Overnight Range: 0.6269-0.6300

AUDUSD is getting a bit of a boost from improved risk sentiment due to hopes that Trump’s April 2 tariffs are watered down. In addition, Judo Bank’s March PMI index rose to 51.3 from 50.6.

NZDUSD

NY Open: 0.57542, Overnight Range: 0.5719-0.5750

NZDUSD lagged AUDUSD gains despite improved risk sentiment due to ongoing expectations for at least two more RBNZ rate cuts before year-end.

USDMXN

NY Open: 20.1823, Overnight Range: 20.1567-20.2455

USDMXN fell to its session low on hopes for some tariff relief. March inflation numbers showed Core CPI rising 0.24% as expected while headline inflation rises 0.24% as expected and down from the 0.27% previously.

FX high, low, open (as of 6:00 am ET)

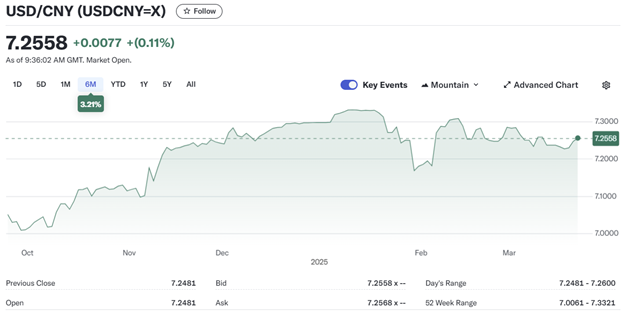

China Snapshot`

PBoC fix: 7.1780 vs exp. 7.2496 (Prev. 7.1760)

Shanghai Shenzhen CSI 300 rose 0.51% to 3934.85

Sources: Yahoo Finance, Oanda, Investing.com,