May 1, 2025

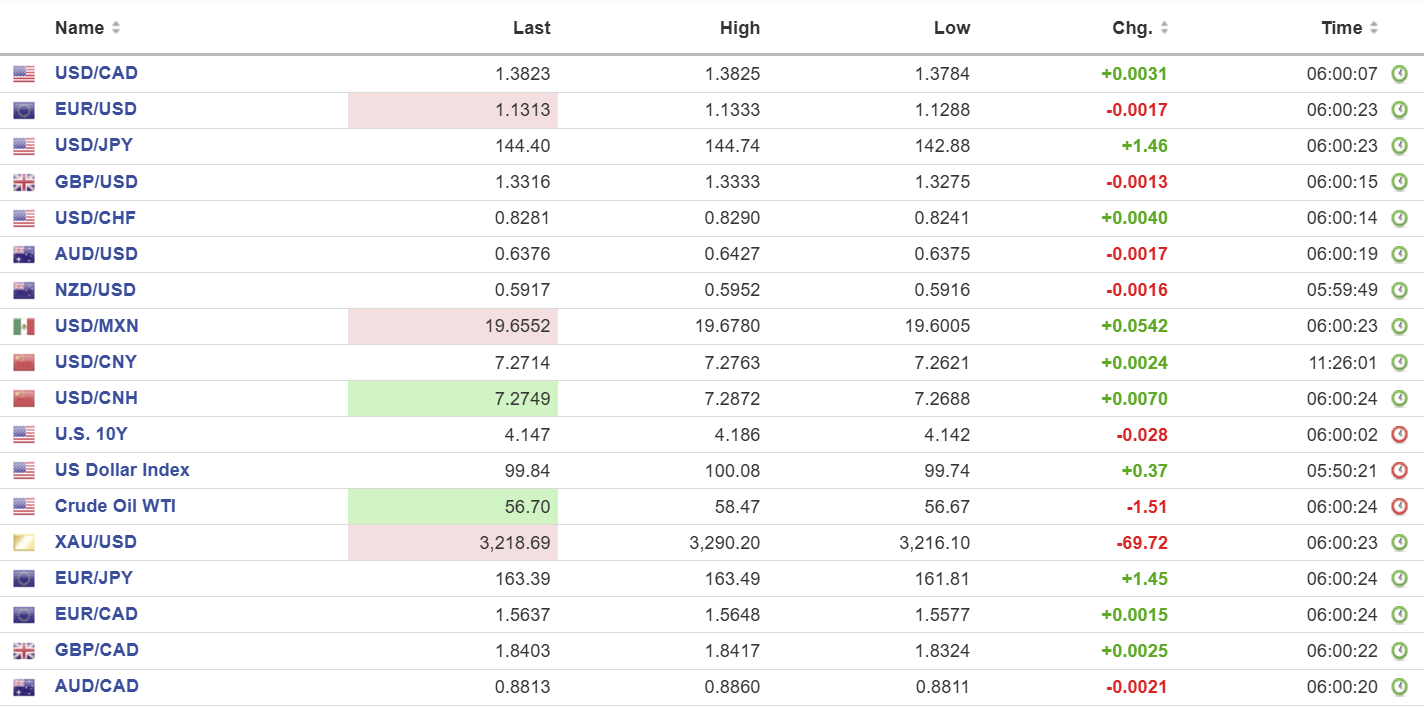

USDCAD: open .3823, overnight range 1.3784-1.3825, close 1.3801

USDCAD ignored yesterdays disappointing March GDP result (actual -0.2% m/m, forecast 0%, previous 0.4%) partly because the Stats Canada estimate is for GDP to rebound to 0.1% in March. That result is questionable as the impact of Trump tariffs has yet to be seen.

USDCAD will continue to be whip-sawed by the ever-shifting US economic sentiment. Traders are still reacting to Trump tweets about how wonderful he is doing despite a pile of evidence to the contrary. He claims to be having trade talks with China but officials in Beijing say if he is, it is news to them.

WTI oil prices fell from 58.47 to 56.83 due to the impact of Trump tariffs and increased production from Iran and Kazah. In addition, Saudi Arabia is rumoured to be planning to demand another increase in production at Opec’s May 5 meeting. Traders ignored yesterdays EIA report that US crude inventories fell by 2.69 million barrels last week.

USDCAD Technicals

The intraday USDCAD technicals are mildly bullish following the failure to break below key support in the 1.3770 area (#rd Std Deviation Bollinger band) which is guarding the 78.6 Fibonacci retracement level at 1.3722. Both RSI and MACD indicators are suggesting an upside bounce targeting the 1.3950 area.

Longer term, the USDCAD downtrend remains intact supported by the prices below the 100- and 200-day moving averages.

For today, USDCAD support is at 1.3770 and 1.3740. Resistance is at 1.3860 and 1.3910

Today’s Range: 1.3770-1.3970

Chart: USDCAD daily.

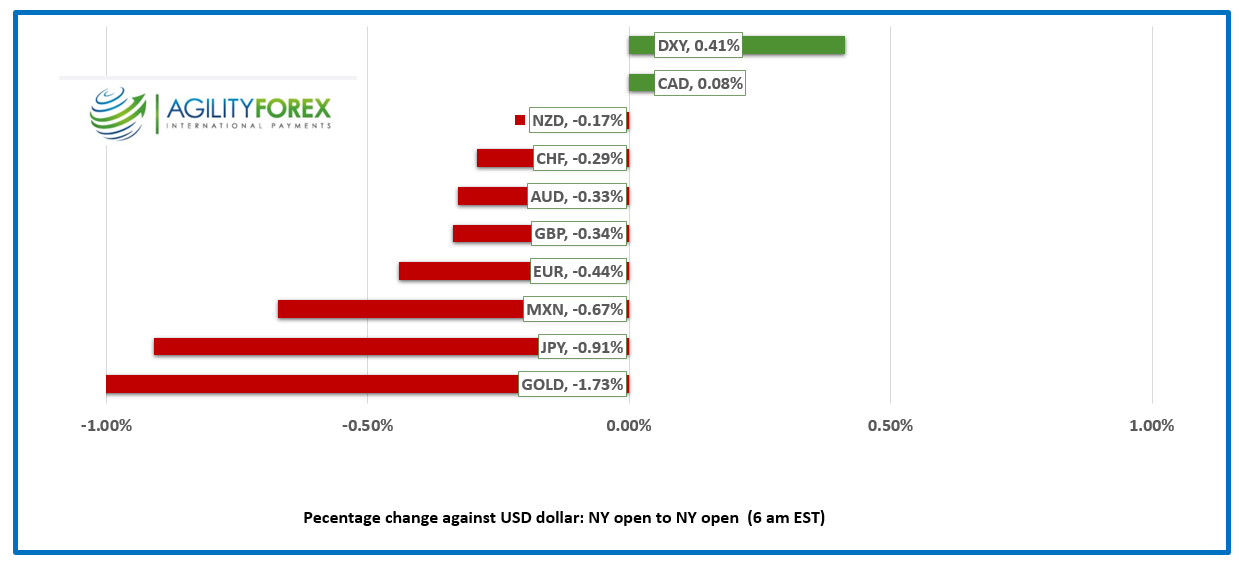

FX at a Glance

Taking a Break

Workers in over 160 countries are not working today to celebrate May Day. In medieval times May 1st was a day to celebrate a Spring Festival which included bonfires, floral garlands and dancing around a Maypole. That date was usurped by trade unions in 1889. The Second International, a federation of socialist and labour parties, officially declared May 1 as Labour Day. It was done to commemorate the Haymarket Affair and honour the deaths of labour activists when a Chicago demonstration turned violent. May 1st is not a statutory holiday in Canada, the US and the UK.

Microsoft Results Lift S&P 500 futures

Wall Street flipped from early losses to close with modest gains yesterday and then analyst-beating earnings from Microsoft and Meta helped propel stocks higher in after-hours trading. Australia’s ASX 200 rose 0.24% and the BoJ rate decision helped lift Japan’s Topix by 0.46%. Hong Kong was closed. The UK FTSE 100 is the only European bourse that is open, and it is flat as of 6:00 am EDT. S&P 500 futures are soaring and are up 1.32%. The US 10-year Treasury yield is 4.147%. Gold XAUUSD broke below support at 3270.00 and is trading at 3215.06 in early NY.

Recent Data Raises Recession Risks

Trump has led the US economy into its first contraction since 2022 while his actions drove consumer confidence to a five-year low. Today, Challenger job cuts fell 62% to 105, 441 compared to last month but they are 63% higher from the same month last year.

Challenger SVP Andrew Challenger wrote: “Though the Government cuts are front and center, we saw job cuts across sectors last month. Generally, companies are citing the economy and new technology. Employers are slow to hire and limiting hiring plans as they wait and see what will happen with trade, supply chain, and consumer spending.”

Initial jobless claims rose 18,000 to 241,000 last week. ISM PMI data is due at 7:00 am PDT.

EURUSD

NY Open: 1.1313 Overnight Range: 1.1288-1.1333

Most of Europe are running around Maypoles or marching in parades due to the Labour Day holiday. The single currency has clawed back some of yesterday’s losses but while prices are below 1.1370, the risk is for a test of support at 1.1250.

GBPUSD

NY Open: 1.3329, Overnight Range: 1.3275-1.3333

GBPUSD rebounded from yesterday’s lows and is trading in NY at its session peak. Prices are supported by US claims that making a trade deal with the UK is a priority. The UK may see it that way as well. UK Manufacturing PMI ticked up to 45.4 in April from 44.0 but according to S&P Global economist “new export business fell at the quickest pace for nearly five years, with demand from clients in the US, Europe and mainland China all declining.”

USDJPY

NY Open: 144.40, Overnight Range: 142.88-144.74

The Bank of Japan did as expected and left interest rates unchanged at 0.5%. However, it was the downgrade of its 2025 GDP forecast to 0.5% from 1.1% and its 2026 GDP estimate to 0.7% from 1.0% that boosted prices. The downgrades were due to uncertainty around Trump’s tariffs. At the same time, policymakers expect core inflation to reach 2.2% in 2025 and 1.7% in 2026.

AUDUSD

NY Open: 0.6376 Overnight Range: 0.6375-0.6427

AUDUSD traded with a negative bias overnight due to broad US dollar strength and is trading just above its session low. Australia’s trade surplus widened to $6.9 billion from 2.85 billion in March, partly due to higher exports to China.

NZDUSD

NY Open: 0.5917, Overnight Range: 0.5916-0.5252

Kiwi is at its overnight low ahead of today’s US data which includes ISM Manufacturing PMI and due to increased odds that the RBNZ cuts rates by 0.25 bp on May 28.

USDMXN

NY Open: 19.6552, Overnight Range: 19.6005-19.6780

USDMXN is trading with a bullish bias while prices are above 19.6230 and looking for a break above 19.7000 to extend gains to 19.7800. The USDMXN gains occurred despite Mexico Q1 GDP rising 0.2% q/q.

China Snapshot`

Markets Closed

PBoC fix: 7.2014 vs exp. 7.2670 (Prev. 7.2029).

Shanghai Shenzhen 300 fell 0.12% to 3770.57

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.