By Michael O’Neill

President Trump has not been kind to Chief Financial Officers, Treasurers, or businesses of any size. These people spend a lot of time, effort, and resources seeking ways to manage and mitigate the companies’ financial risks. They need to identify and quantify financial exposures, particularly to foreign exchange and interest rates then forecast future cash flows, and understand the financial impacts from unhedged exposures.

Finally, a comprehensive hedging policy is developed, outlining objectives, acceptable instruments, limits, and responsibilities. It’s a tried-and-true strategy that has helped corporations survive the turmoil of the COVID pandemic, the 2008 financial crisis, and the Iraq war.

Sure, there were wobbles and wrinkles, but for the most part it was working, right up until January 20, 2025.

No Playbook for Pandemonium

President Trump first took office on January 20, 2017, where he met and began a relationship with Executive Orders. He was rather shy and awkward and only issued 55 executive orders for the entire year. That changed on January 20, 2025. He fell head-over-heels in love with the ability to sign a piece of paper and wreak havoc across the globe, which he has done 152 times as of today and about 6–7% of them have had significant alterations, suspensions, or reversals. This on-again/off-again approach is extremely problematic for businesses and institutions attempting to manage their financial exposures. The numerous tweaks, amendments, or delays are a catastrophe.

.

Volatility is the First Casualty of a Tariff War

FX traders are no strangers to pain, but 2025 introduced a fresh variety—policy-by-impulse. Back in 2023, DXY volatility was already on the downslope, easing from double-digit levels to around 7% as markets digested Fed hikes and inflation angst gave way to fatigue. By mid-2024, things were downright sleepy—annualized volatility flirted with 5.5%—until a soft patch in the U.S. economy and a couple of well-telegraphed Fed cuts jolted things back toward 7%. Then Trump returned, executive orders in one hand, tariff threats in the other, and just like that, market calm went the way of the VHS tape.

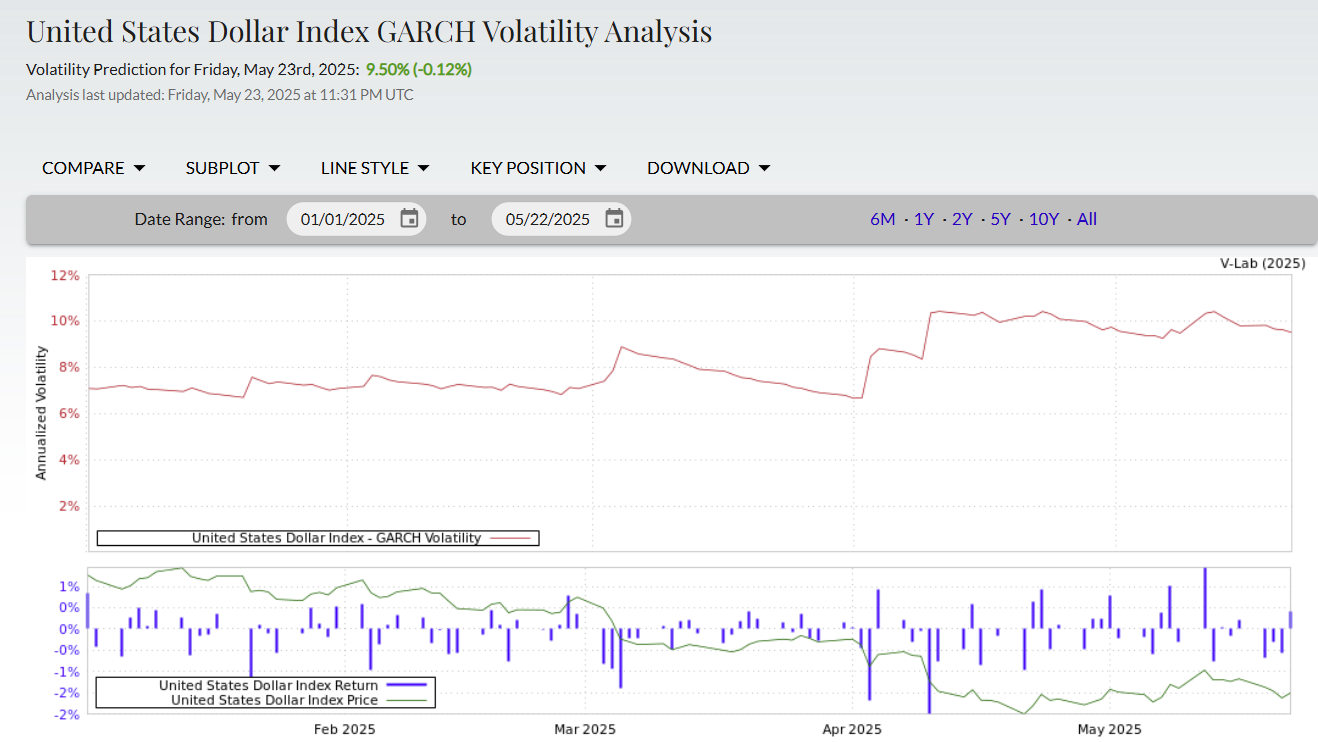

Between January and late May, NYU’s Volatility Lab clocked DXY annualized GARCH volatility at 9.5%—and that may understate it. The real-world price action suggests implied vol likely ran hotter, as traders tried to hedge what can’t be forecasted: a tweet, a pivot, or a policy reversal scribbled on a napkin at dinner. The only constant in 2025 has been uncertainty—and hedging costs are rising.

Source: V-Lab NYU

When Forward Traders Trade Like Spot Traders

In this environment, traditional short-term hedging strategies are beginning to unravel. Normally, forward traders take a measured view—booking hedge rates over 60, 90, or 180 days, absorbing short-term noise in favor of predictable cash flow coverage. But 2025 isn’t normal. When official policy is announced on TruthSocial, forward traders start thinking like spot traders.

The result? That carefully constructed 90-day hedge is suddenly deep out-of-the-money. The forward rate that looked like a no-brainer at execution is now marked to market at a loss before the confirmation email even lands. And when tariffs are announced, delayed, walked back, and slammed back on in the space of two weeks, even the most robust hedging strategies get torpedoed.

Add in ballooning U.S. debt, a Moody’s downgrade, and global markets second-guessing Washington’s every move, and you’ve got the perfect recipe for macro mayhem.

For corporates, this means higher costs as hedging instruments like forwards and options get more expensive and hedge ratios get distorted by market whiplash. Some treasurers are slashing hedge tenors to avoid getting blindsided. Others are skipping the process altogether and becoming active spot traders.

It really doesn’t matter. In the Executive Order era, as long as policy is dictated by impulse, not process, hedging strategies and coin-flipping are one and the same.

One man’s mood ring is another man’s bad mood.