June 2, 2025

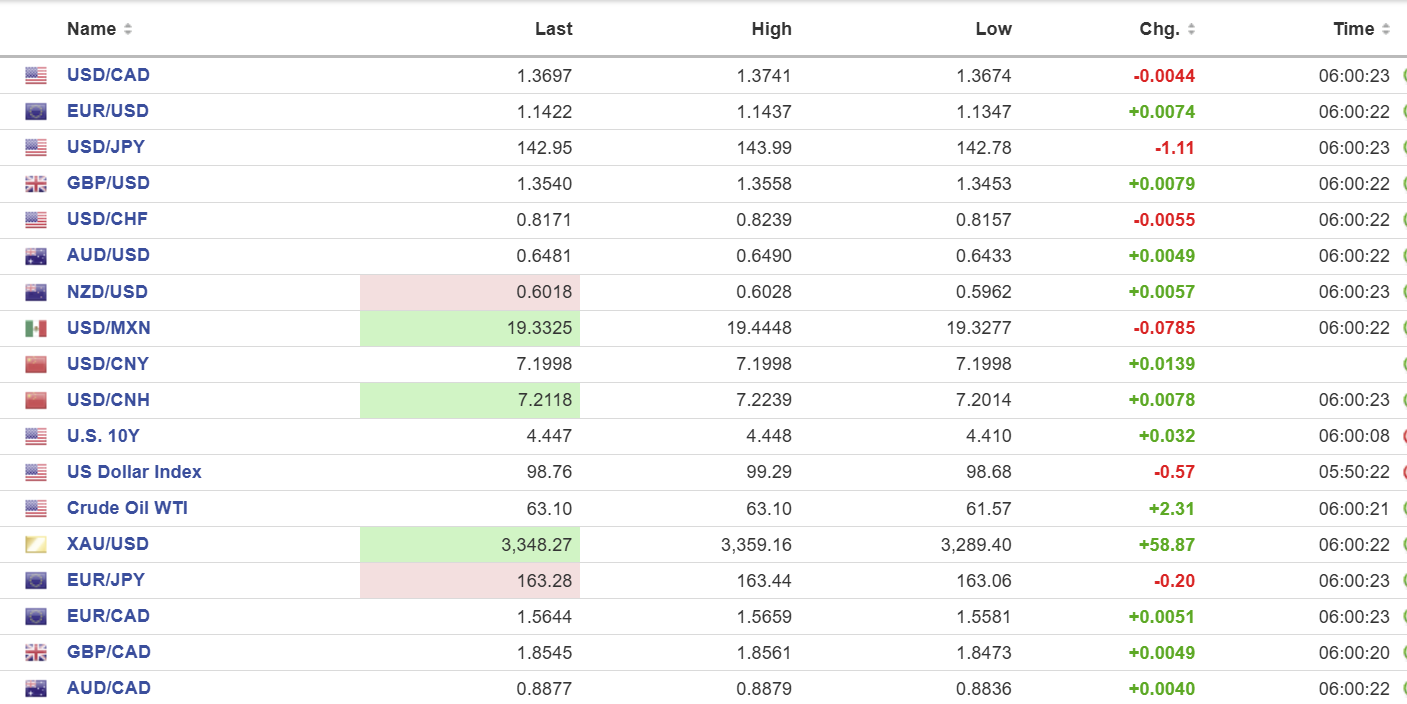

USDCAD: open 1.3697, overnight range 1.3674-1.3741, close 1.3740

Trump is at it again. His Liberation Day tariffs were ruled illegal, but the decision is being appealed so he reverted to his “National Security” tariff playbook. Canada and Mexico suffered his wrath and were hit by a 25% bump to 50% for steel and aluminum tariffs imported into the US. It’s bad news for Canada because it produces nearly twice as much steel as it needs for domestic consumption. The US has more sources for steel than Canada has outlets.

The news should have boosted USDCAD, but it didn’t. Instead, the combination of month-end portfolio rebalancing flows, escalating trade tensions, and dovish comments from Fed Governor Waller fueled US dollar selling and the Canadian dollar got a lift.

Canada’s headline GDP number suggests that the economy is not doing as badly as the Trump tariff war suggests it should, while the details say otherwise. Nevertheless, the headline number, the odds that the Carney government unleashes new fiscal stimulus, and elevated inflation readings point to the Bank of Canada leaving rates unchanged at Wednesday’s meeting.

WTI oil prices are at the top of its overnight 61.07–63.03 range. Opec announced another production increase of 411,000 barrels/day beginning in July, which was better than some earlier predictions of a sharply higher increase. The price rally was underpinned by low levels of US fuel supplies ahead of the summer driving season.

US ISM Manufacturing PMI is expected to have risen to 49.5 from 48.7 in April

USDCAD Technicals

The intraday USDCAD technicals are bearish following the decisive breach of support at 1.3725 and is looking for a break of support at 1.3670 to extend losses to the 1.3630-50 area. Only a move above 1.3750 will negate the selling pressure.

The medium term technicals are bearish. The topside is capped by the 200 day moving average at 1.4023. The momentum and trend indicators confirm bearish pressure as long as prices are below 1.3850.

For today, USDCAD support is at 1.3670 and 1.3640. Resistance is at 1.3740 and 1.3780

Today’s Range: 1.3670-1.3870

Chart: USDCAD daily

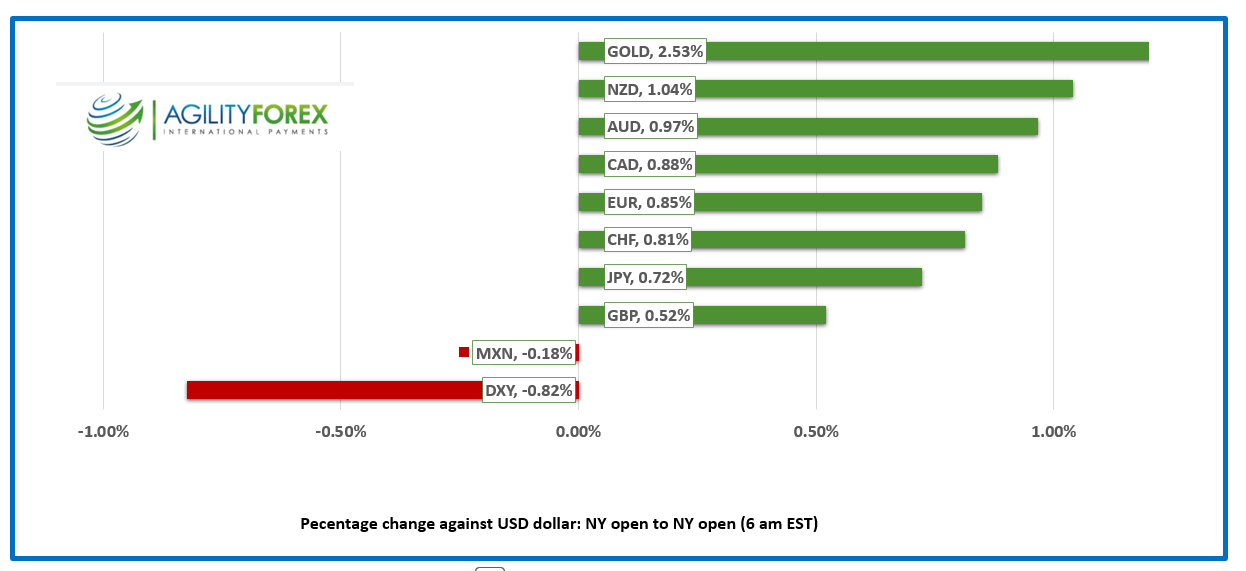

FX at a Glance

Trade Tensions Rekindled

President Trump is not one to be dissuaded from a course of action by pesky legalities. His Liberation Tariffs were found to be illegal because he got bad advice and selected judges who would not bow to his whims. He is appealing the ruling, but just to show he is in charge, he increased tariffs on steel and aluminum by 25% to 50%.

China accused the US of bargaining in bad faith and said the Americans are seriously violating the Geneva trade truce. US Treasury Secretary accused China of the same thing, saying Beijing is withholding critical minerals. The Americans are extremely perturbed that Chinese leaders are not prostrating themselves before Trump.

Fed Official Chirps Dovishly

Fed Governor Christopher Waller said he is open to cutting rates this year because he doesn’t believe that inflation increases from Trump’s tariffs are likely to be persistent, saying “I support looking through any tariff effects on near-term inflation when setting the policy rate.” Those comments will be weighed against this week’s employment data, which starts with JOLTS job openings on Tuesday and finishes with nonfarm payrolls on Friday.

Global Equity Indexes Start June Defensively

Fresh off a profitable May, Trump’s latest tariff salvo put traders on the defensive and Asian indexes started June with losses. Japan’s Topix lost 0.87%, Hong Kong’s Hang Seng fell 0.57%, and Australia’s ASX 200 dropped 0.24%.

European bourses followed suit, and a 0.45% decline in the French CAC 40 index is leading the others lower. The German Dax has fallen by 0.32% while the UK FTSE 100 is up 0.11%. S&P 500 futures are down 0.30% while renewed risk aversion boosted gold (XAUUSD) by $73.16 to 3362.53. The US 10-year Treasury yield is 4.43%. All of the above levels are as of 5:15 am PT.

EURUSD

NY Open: 1.1422, Overnight Range: 1.1347-1.1437

EURUSD rallied on risk aversion and lingering month-end demand as Trump’s latest tariff actions renewed “get me out of US dollars” sentiment. EURUSD was also underpinned by Eurozone Manufacturing PMI, which rose to 49.4 from 49.0 in April. The statement said, “The upward trend in the headline PMI is still continuing, pointing towards a recovery that is progressing. That is backed up by the rise in production we have seen since March.” The ECB is expected to announce another 25 bp rate cut on Thursday.

GBPUSD

NY Open: 1.3540, Overnight Range: 1.3453-1.3558

GBPUSD accelerated to the overnight peak on the back of a higher-than-expected UK PMI reading (actual 46.4 vs 45.4 in April) and because of widespread US dollar selling pressure from Trump’s tariffs. S&P Global Director wrote this about the PMI results: “May PMI data indicate that UK manufacturing faces major challenges, including turbulent market conditions, trade uncertainties, low client confidence, and rising tax-related wage costs.”

USDJPY

NY Open: 142.95, Overnight Range: 142.78-143.99

USDJPY tumbled on the heels of rising risk aversion, driving safe-haven demand for yen due to escalating US/China trade tensions. USDJPY is also on the defensive due to Bank of Japan rate hike expectations. Japan Manufacturing PMI rose to 49.4 from 48.7 in April.

AUDUSD

NY Open: 0.6481, Overnight Range: 0.6433-0.6490

AUDUSD posted small gains due to general US dollar weakness, but the gains were capped due to ongoing US/China trade tensions.

NZDUSD

NY Open: 0.6018, Overnight Range: 0.5962-0.6028

NZDUSD posted gains due to broad US dollar selling pressures, with further direction to be determined by tariff news and US jobs data.

USDMXN

NY Open: 19.3325, Overnight Range: 19.3277-19.4448

USDMXN rallied on Friday, and it is in the process of reversing the gains today. Renewed US economic growth concerns have offset the latest increase in steel and aluminum tariffs on Mexican exports to the US.

China Snapshot`

MARKETS CLOSED- Friday PBoC fix: 7.1848 vs exp. 7.1859 (Prev. 7.1907)

Shanghai Shenzhen 300 fell 0.48% to 3840.23

NBS Manufacturing PMI 49.5 (forecast 49.5, previous 49), Non-manufacturing PMI 50.3, forecast 50.6. previous 50.4)

FX high, low, open (as of 6:00 am ET)

Sources: Yahoo Finance, Oanda, Investing.com, Bloomberg.

–